com.bibiphoto

Most bond ETFs focus on fixed-rate bonds and therefore involve some price risk. Investment grade bond ETFs tend to have significant price risk, as investment grade companies issued tons of long-term debt in previous years when prices were lower.

iShares interest ETF ratio for hedged corporate bonds (NYSEARCA:LQDH) uses interest rate swaps to reduce interest rate risk, with a minimal duration for the fund. The result is much smaller losses when interest rates rise, much smaller gains when those rates fall, a more stable stock price, and stronger risk-adjusted returns. The fund currently has a healthy yield of 6.6% to maturity. Dividend yields are even higher, at 8.3%, but these appear to include swap gains and so are not necessarily indicative of underlying income generation.

In my opinion, LQDH is a buy, and looks particularly well-suited to risk-averse, long-term investors and retirees.

LQDH – Overview and Analysis

Strategy and holdings

LQDH is an investment grade hedged corporate bond index ETF.

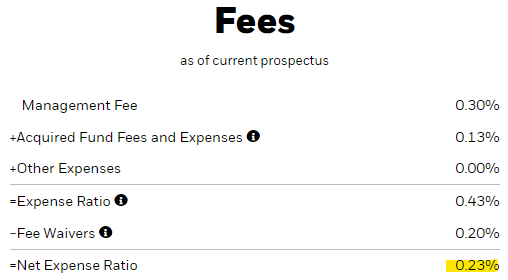

LQDH invests the majority of its assets, currently 97%, in the iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD), the largest ETF on the market. BlackRock manages both funds. It currently waives a significant portion of LQDH’s fees, resulting in an expense ratio of 0.23% for the fund, which is very low for a specialty ETF.

LQDH

LQDH invests the remainder of its assets in interest rate swaps, with the aim of reducing the Fund’s interest rate risk. Let’s explain how these work with a specific example.

LQDH

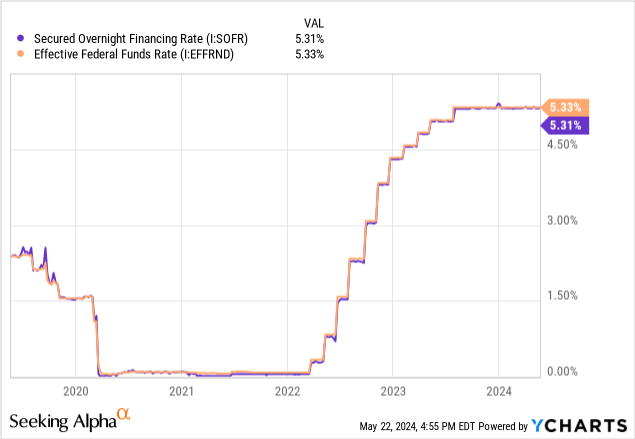

In the above swap, the Fund committed to paying a fixed annual coupon of 5.36% to the counterparty, on a $7 million swap with an expiration date of 05/07/2024. In return, the fund will receive 5.35% interest. Variable rate Voucher from the counterparty on the same date. The coupon in question is indexed to SOFR, which is functionally equivalent to Federal Reserve rates, for our purposes at least.

Data by YCharts

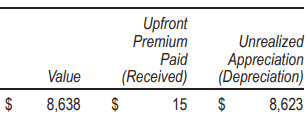

Trade-offs generally have a cost. LQDH had to pay a premium of $15,000 to enter into the above swap.

Currently, the swap has an incredibly marginal impact on LQDH’s performance: the fund pays 5.36%, and receives 5.35%, for a net payment of 0.01%.

An LQDH swap will benefit from higher rates in two ways.

First, higher rates would increase the variable rate coupon the fund receives, resulting in a higher/positive net payment. If the Fed raised interest rates to 6.25% – 6.50%, the SOFR would rise to about 6.35%, and the fund would receive 6.35%, paying 5.36%, for a net positive payment of 0.99%,

Second, in view of the above, higher interest rates would increase demand for and prices for these securities, resulting in capital gains for the Fund. Expectations of higher interest rates would have a similar effect. One can see this happening, as the fund sees $8.6 million of capital gain (appreciation) from this swap.

LQDH

The flip side of the above is that an LQDH swap will negatively impact the fund if interest rates fall.

LQDH swaps are selected to minimize the fund’s overall interest rate or duration risk. So rising interest rates should lead to losses in the fund’s portfolio, and gains in its swaps, and the net effect should be close to zero. Same idea for lower prices.

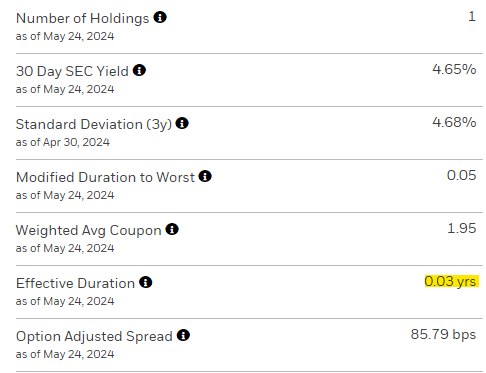

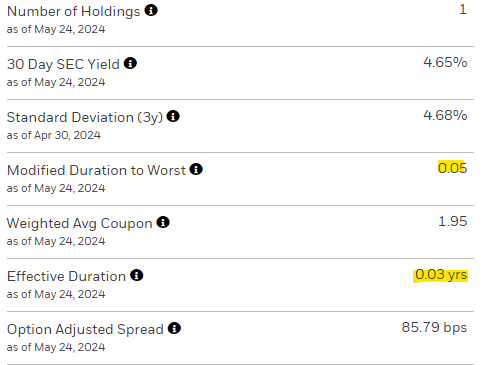

The duration of the LQDH is virtually zero, as expected.

LQDH

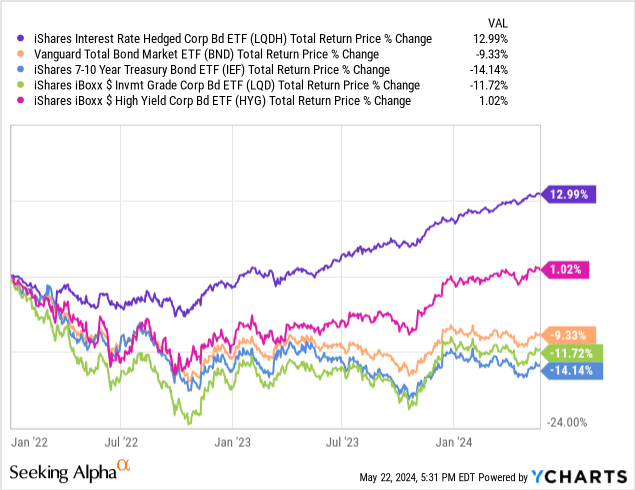

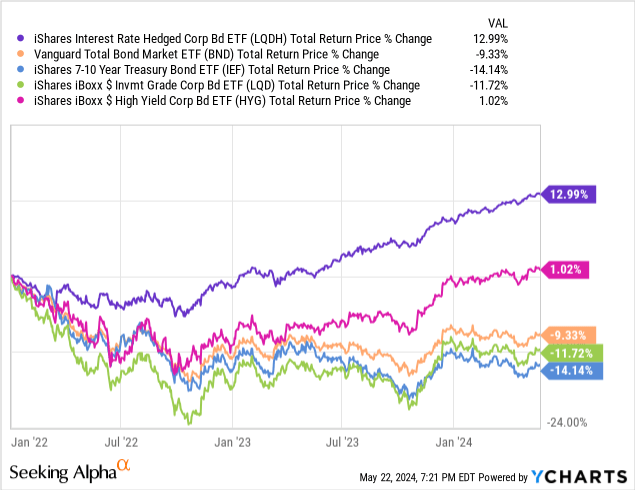

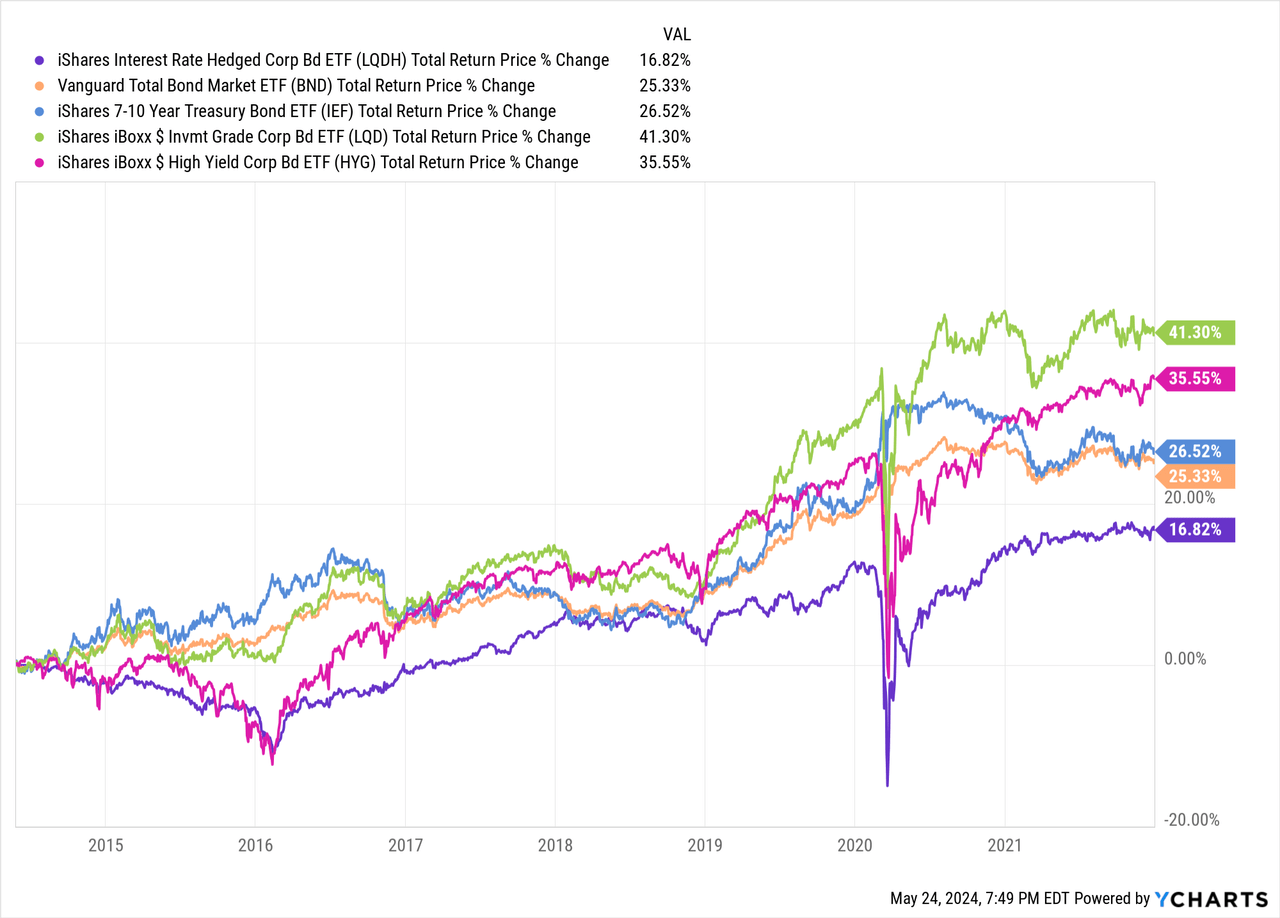

LQDH has effectively hedged most of its interest rate risks over the past few years, as expected. The returns were reasonably good, and a lot Above average.

Data by YCharts

Did not see LQDH some Losses during early 2022, although these were not caused by higher interest rates per se. Since the fund invests in corporate bonds, it faces some credit risk, which should be considered some Losses during recessions, or when spreads widen. Spreads widened during 2022, hence the losses.

Data by YCharts

Now that we know how LQDH swaps work, let’s take a look at some of the broader features and benefits of the fund.

Diversified Holdings

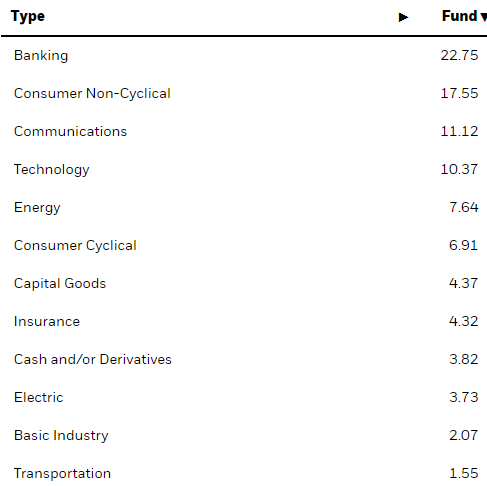

LQDH swaps are their main differentiator, but their investment in LQD is the largest, and should be their main source of income and returns in the long term.

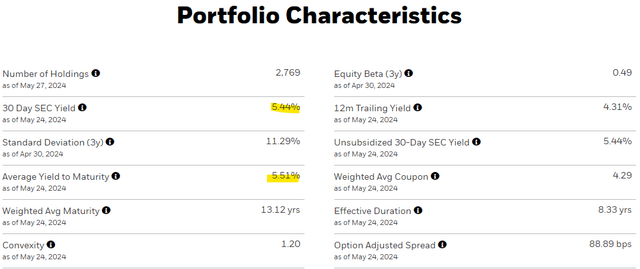

LQD itself is a large, diversified investment-grade ETF. It currently invests in 2,768 different securities from most relevant sectors.

LQD

LQD

Diversification reduces the risk, volatility, and magnitude of losses resulting from default of any individual issuer. LQDH is certainly less diversified than some of the broader bond index ETFs on the market, including the Vanguard Total Bond Market Index Fund ETF (BND), which invests in several bond subasset classes. However, LQDH seems to be sufficiently diverse.

Strong credit quality

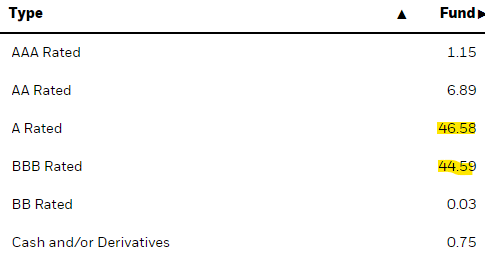

LQDH invests almost exclusively in investment grade corporate bonds. They are issued by relatively safe companies with strong balance sheets and financial statements. Currently, the fund is roughly evenly split between A and BBB-rated bonds, with small investments in AA-rated bonds, and nominal investments in bonds with other credit ratings.

LQDH

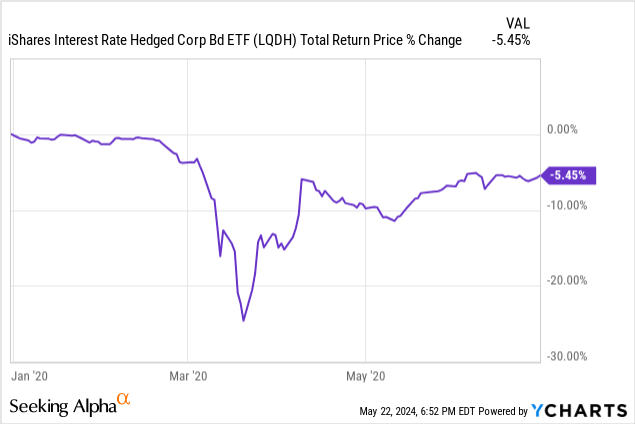

Because of the above, the default rates for these bonds are very low, and do not depend greatly on economic conditions. Expect relatively small losses during downturns and downturns, as was the case (mostly) in 2020, during the beginning of the coronavirus pandemic. The withdrawal rate reached 25%, which is higher than expected, but it only lasted for a few days/weeks.

Data by YCharts

LQDH’s strong credit quality is an important benefit to the Fund and its shareholders, and may be of particular interest to more risk-averse investors.

Good dividend yield

LQDH’s earnings look reasonably good, although the situation is complex.

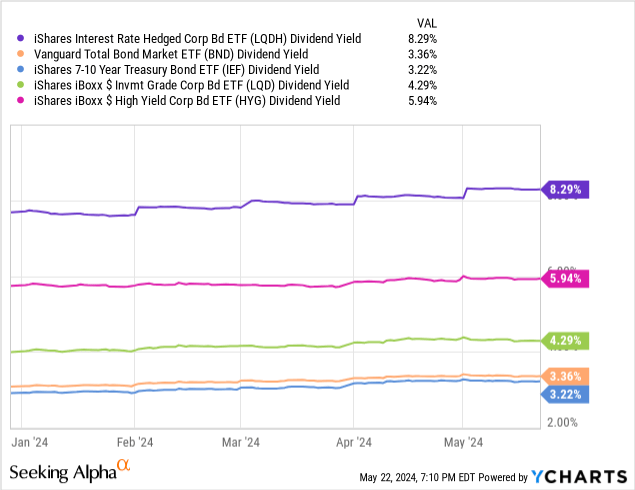

Currently, the fund has a dividend yield of 8.3%, which is very high on an absolute basis, and higher than most bonds and bond sub-asset classes.

Data by YCharts

In some cases, ETFs must distribute gains from futures and options to shareholders. Although I’m not entirely sure if this is the case for fund swaps, it appears to be the case. Basic LQDH cannot reasonably generate that much income. LQD itself has a yield of 5.4% SEC and 5.5% YTM, which is much lower than LQDH.

LQD

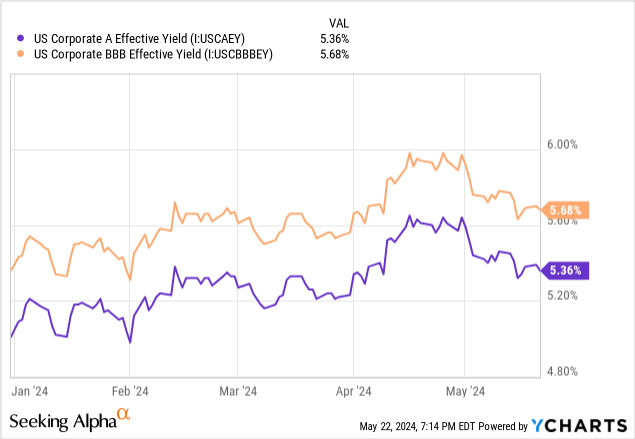

Investment grade bond yields are similar.

Data by YCharts

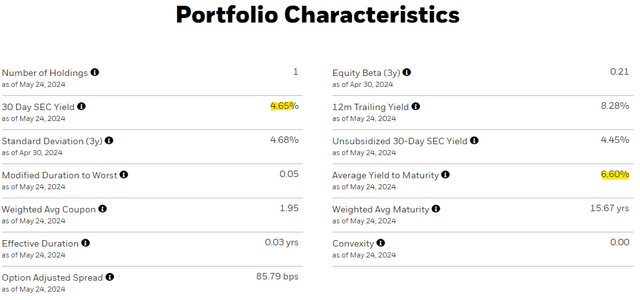

LQDH itself has a yield of 4.7% SEC and 6.6% YTM. I think the latter includes the (expected) payouts from swaps, as well as the more relevant figure.

Data by YCharts

I would summarize the situation this way. LQDH distributes 8.7% to shareholders annually (dividend yield). The underlying LQDH holdings, if held to maturity, should return 6.6% per annum (YTM/yield to maturity). In my opinion, the 6.6% figure is more relevant, and more indicative of the returns investors should expect going forward.

Interest rate risk

LQDH effectively hedges interest rate risks, so this risk is effectively zero.

LQDH

Because of the above, expect small losses well below average when interest rates rise. Since most bonds carry some interest rate risk, LQDH should outperform when rates rise, as has been the case since early 2022.

Data by YCharts

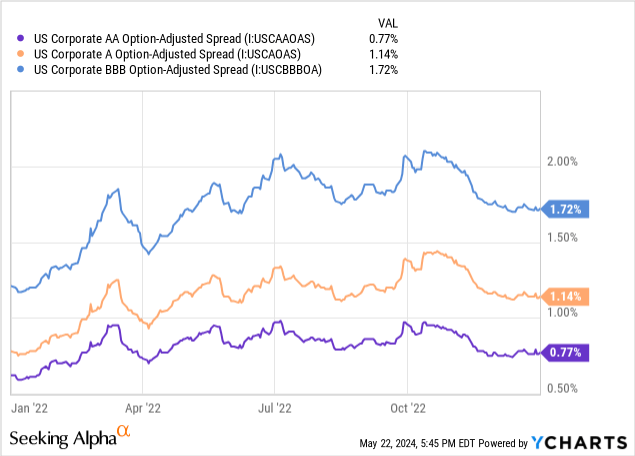

LQDH has some credit risk, so it should see some losses when credit spreads widen, which is… could They coincide with periods of high rates. This was the case during early 2022, which, as we see above, led to some losses. The losses were not that large, and below average.

General volatility

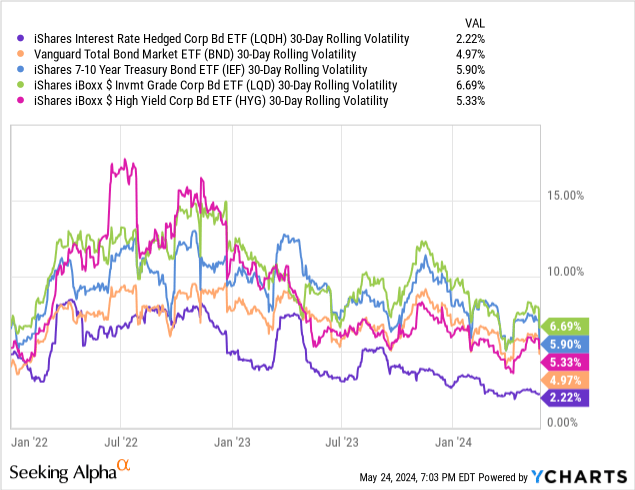

LQDH’s low interest rate and credit risk results in a relatively safe and stable fund with below-average volatility.

Data by YCharts

The above is a significant benefit of the Fund and may be of particular interest to more risk-averse investors.

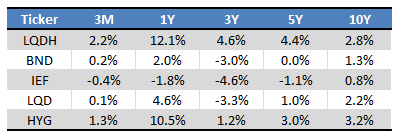

Performance scorecard

LQDH’s performance record is as follows:

Searching for Alpha – table by author

Several things stand out from the above.

LQDH’s long-term returns are very low, as have been the rates especially It was low in the past.

LQDH’s returns over the past three years or so have been reasonably good, due to rising federal interest rates and dividend yields. LQDH has significantly outperformed most of its peers as well, due to its lower risk profile.

LQDH’s recent returns have been very strong, mostly due to tightening credit spreads, but rising interest rates/yields have also played a role.

LQDH has somewhat outperformed its peers since its inception, due to its outperformance over the past few years of rising rates.

Finally, although the results in the table above are accurate, I feel they overestimate the consistency of LQDH’s performance. The fund underperformed significantly before 2022, and most of its returns/outperformance have come since then.

Data by YCharts

Going forward, LQDH returns depend strongly, and predominantly, on federal interest rates. Under current conditions, expect annual returns in the mid-single digits, as has been the case for the past five years. Higher federal interest rates would lead to higher profits and returns, and vice versa.

Conclusion

LQDH’s good 6.6% yield to maturity, and low overall risk and volatility, make the fund a buy.