Thomas Brown/Digital Vision via Getty Images

Investment Thesis: I continue to rate MakeMyTrip as a Buy at this time.

In a previous article in February, I made the argument that MakeMyTrip Limited (Nasdaq: MMIT) could have upside potential To a target price of $77 based on continued sales growth, but I will continue to monitor growth in customer enticement costs across the hotel and packages segment.

ycharts.com

The stock has since surpassed that price target — up more than 35% from my last article and trading at $79.24 at the time of writing.

The purpose of this article is to evaluate whether MakeMyTrip has potential for further upside from here.

performance

When looking at Q4 and FY2024 results, we can see that revenues increased by 36.6% compared to the previous quarter of last year, and by 32% year over year. Annual basis:

MakeMyTrip Limited: Q4 and full-year earnings released

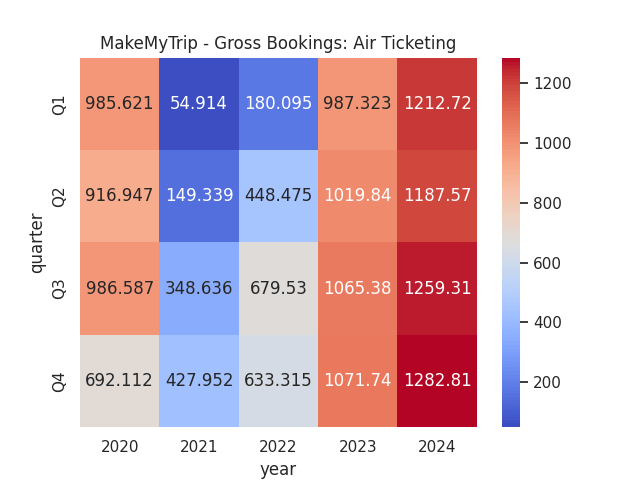

Regarding total airline ticket bookings, we can see that it increased by 19.7% compared to the previous quarter of last year, and 1.9% compared to the third quarter of 2024.

Figures are sourced from MakeMyTrip’s previous earnings releases (Q1 2020 to Q4 2024). Figures presented in millions of US dollars. Heat map created by the author using the marine visualization library in Python.

I mentioned earlier that I would be watching whether MakeMyTrip can ultimately drive revenue growth across the hotel and packages segment while also reducing the growth rate in customer incentive costs. With 28.5% growth in hotel and package revenues QoQ, and 29% YoY – we have seen encouraging growth across the segment.

Regarding customer incentive costs, we can see that on a three-month ended basis, hotel and package costs rose 42% and accounted for 30% of revenue in Q4 2024 compared to Q4 of the previous year.

MakeMyTrip Limited: Q4 and full-year earnings released

Looking from a year-over-year perspective, we see that customer incentive costs rose 36%, with costs now representing 28% of revenue compared to 27% the previous year.

MakeMyTrip Limited: Q4 and full-year earnings released

The initial reason for expressing my concern about customer incentive costs for hotels and packages was that this sector showed lower revenue growth compared to other sectors, at 21.5% for the third quarter of 2024 compared to the third quarter of the previous year.

However, with hotel and package revenues up 29% for Q4 2024 compared to the previous quarter – I see the rise in customer enticement costs as acceptable as we see revenue growth as a result.

Risks and looking to the future

My view on the above results is that the higher growth rate we have seen across hotel and package revenues is encouraging, and despite my prior reservation about higher stimulus costs – the fact that we are seeing higher revenue growth justifies higher costs in the short to medium term.

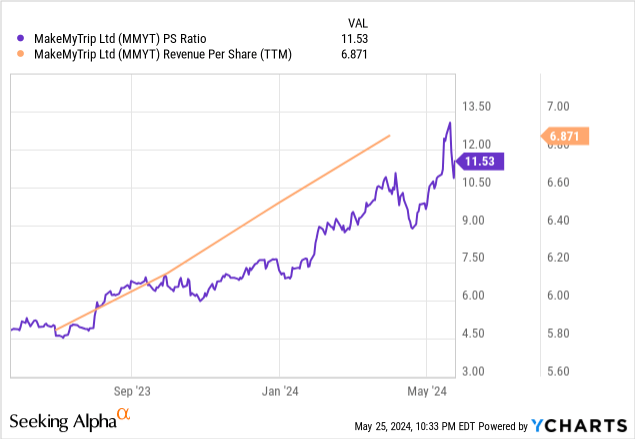

I previously expressed my view that given the stock’s 8.646x price-to-sales ratio back in February, we could see a fair value of $77 per share if revenue per share continues to grow back to its previous highs of $9 ($9 revenue per Share) Share * 8.646x P/E ratio = $77.81. Earnings per share at the time were trading at $6,519.

Since then, we’ve seen PS rise by 33.36%, while EPS is up 5.40%.

Price to sales ratio

ycharts.com

From this, we can see that the growth in price-to-sales ratio significantly outpaces the growth in earnings per share. In this regard, I believe the stock is trading at fair value at the moment.

Going forward, I see MakeMyTrip as having the potential to continue growing revenues across the hotel and packages segment – especially given India’s strong domestic travel market. For example, weekend getaways continue to grow in popularity and popular travel destinations like Jim Corbett saw search growth of 131%. Furthermore, spiritual tourism has also seen growth – with a 97% increase in searches on the platform over the past two years.

Although I have previously expressed concern that MakeMyTrip may see a slowdown in revenue outside of the peak season for international travel to India from October to March, the country as a whole is benefiting from a strong domestic travel market, which is why I expect we will be able to continue to see Strong future revenue growth.

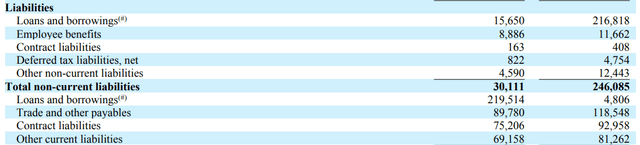

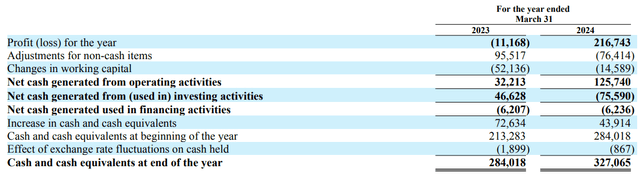

In terms of potential risks, it is noted that short-term loans and advances have increased significantly from US$15.65 million in March 2023 to US$216.818 million in March 2024 – due to the maturation of non-current loans and advances.

MakeMyTrip Limited: Q4 and full-year earnings released

While the revenue growth we’ve seen has been encouraging, investors will be looking more closely to determine if the company has the ability to service its short-term debt while continuing to invest in further revenue growth.

However, we can see that the company has significantly grown its cash and cash equivalents by 15% during this period – indicating that the company is in a good financial position and has the ability to service its current liabilities.

MakeMyTrip Limited: Q4 and full-year earnings released

Conclusion

In conclusion, MakeMyTrip has seen encouraging growth in revenue and the increase in domestic tourism has been encouraging. I see the stock as somewhat overvalued at the moment, but it has the potential to rise over the long term given the strong performance in the hotel and packages sector, as well as continued growth in domestic tourism.