Don’t go

shares ConocoPhillips (New York Stock Exchange:COP) fell more than 3% on Wednesday after it announced the acquisition of Marathon Oil Company (Marw). Shares are now down more than 10% from their highs, although they are still up 16% from a year ago. since. Last September, I rated Conoco stock as “He buys“But since then, it has become dead money, losing 2% with the market up more than 20%. Given its complementary assets and strong capital returns, I view this deal favorably, and it could be a catalyst for the stock to move higher over time.

Seeking alpha

Under the terms of the transactions, COP will pay 0.255 of its shares for each MRO share, paying a premium of approximately 15%, toward the minimum M&A premium. COP will assume the MRO’s net debt of $5.4 billion, for a purchase price of $22.5 billion. Conoco stock is trading at a P/E of 13.3 times today, based on consensus estimates. Based on consensus Estimates and deal price are ~$29.50, and MRO is bought at a consensus earnings of 10.1x. MRO is smaller and less diversified, and its focus on buybacks over dividends has contributed to a persistent discount multiple, although I’ve looked at its fundamentals. Asset base is positive. COP would be wise to take advantage of this discount.

In other words, even with a premium, MRO is trading at a discount to COP, which is why Conoco expects the deal to be accretive to its shareholders – a view I share. COP also expects about $500 million of cost synergies, given the overlap of its asset base. Accordingly, Conoco expects to repurchase shares worth $7 billion in the first year and $20 billion over three years. It will also raise its dividend by 34% regardless of the deal closing at $0.78 by the end of the year, and expects asset sales of approximately $2 billion while optimizing its portfolio.

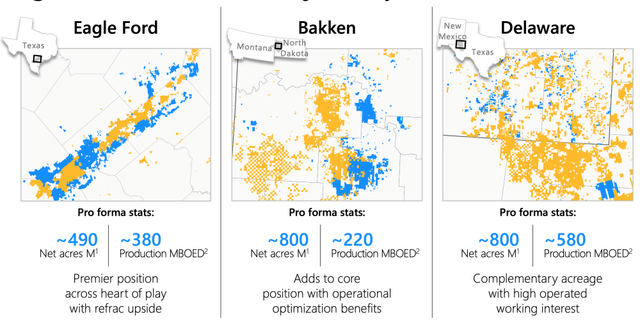

As you can see below, the two companies have overlapping asset bases (COP properties in orange and MRO properties in blue). This overlap is why the company expects to incur so much of the cost: $250 million in general and administrative expenses, $150 million in operating costs, and $100 million in capital. The combined company owns about 2.3 million barrels of oil per day of production. This operating cost reduction is approximately $0.18 per BOE and the additional capital is approximately $0.12 per BOE. These reductions are fairly modest, and each assumes a cost savings of less than 1.5% versus the company’s pro forma spending. I find such a goal credible, if not conservative. Given the extent of overlap that exists, COP & MRO must be able to optimize drilling crews and use greater scale to negotiate better prices with suppliers.

ConocoPhillips

It seems to me that G&A’s goal is a bit more ambitious. COP will spend about $700 million on G&A this year. The MRO must spend about $320 million on G&A, so the goal here is a 25% reduction. Now, Conoco is more than 5 times the size of MRO, so the fact that MRO spends nearly 40% on G&A suggests the potential for significant cost reductions. This is the benefit of scale. Even with increased production, you still only need one CEO, one CFO, one investor relations team, likely a similarly sized accounting department, etc. I expect there will be material expansion opportunities and job cuts due to layoffs. Even running an MRO at COP efficiency and assuming no benefits from additional scale could reduce G&A in the legacy MRO by about $180 million.

As such, although the $250 million target seems large at first glance, it only assumes about $70 million of “ambition” in my view. I consider this possible. However, G&A’s target seems a bit more aggressive than production-related cost reductions. Given how modest this target is, I see some upside in capital savings versus the $100 million target, which could offset a bit of the underperformance on the G&A savings front. Overall, I see roughly $500 million in run rate savings after one year as a very achievable goal, although the mix may be a little different.

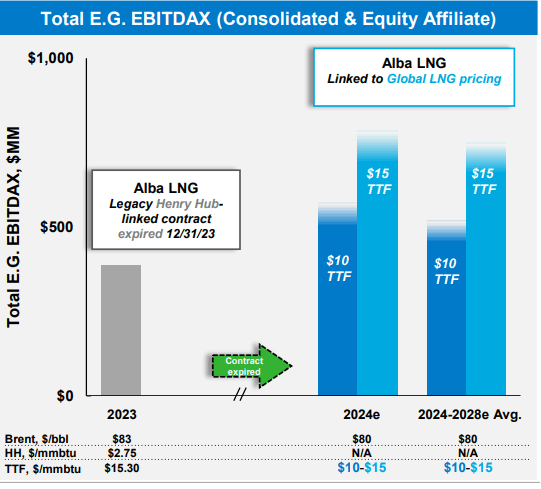

I also view the MRO asset mix favorably. About 53% of its production in the United States is oil. Just under 50% of Conoco’s production is oil, so the MRO will slightly increase the company’s liquids versus natural gas orientation. I see this as a positive, given that oil has wider spreads. OPEC+ provides some floor for oil prices, while natural gas has no cartel supporting prices. Moreover, oil is a global market, while natural gas is a relatively domestic market, due to high transportation costs and limited export capacity. With the abundance of natural gas in the United States, prices have struggled to stay at the $3 level for long periods of time. I assume this is still the case. Now, only a quarter of the MRO’s international operations are oil (representing just 11% of the combined company). However, half of the natural gas is sold as LNG rather than gas, providing oil-like returns, given Europe’s demand for LNG as it shifts away from Russian gas. MRO has a stake in the LNG export hub in Equatorial Guinea, which is now benefiting from the expiration of lower-priced contracts, saving more than $200 million that will benefit COP.

Marathon oil

This asset also fits well with Conoco’s own LNG efforts, and with Russian gas exports to Europe unlikely to resume anytime soon in my view, demand for LNG should remain strong. The Biden administration is also delaying new U.S. LNG export facilities, which could continue to constrain supply and support higher margins. Of course, election results could change this, but since these projects can take years to complete, each delay only prolongs supply constraints, suggesting favorable economics will continue for longer.

At $80 oil and $2.50 natural gas, MRO can generate about $2 billion in free cash flow, and with cost reductions combined, that could get even better. I view $75-85 as the base case for oil, assuming no global recession and current OPEC policy, and $2.50 as a reasonable estimate for US natural gas, recognizing that the weather could swing this materially in the short term. COP pays about 9 times free cash flow, which I find attractive. COP should generate about $10 billion of free cash flow in this environment, and is trading at about 14x. This is a meaningful evaluation gap that is being exploited.

With roughly $12.5 billion in combined free cash flow, it can safely meet its $7 billion buyback target and pay its dividend that would now cost about $5.5 billion, assuming energy prices remain steady. The combined company has a pro forma free cash flow yield of 8%, which I consider attractive, given the potential for modest production growth, an increase in LNG, and the potential for further reductions in capital costs. COP has found an accretive asset to add to its portfolio in MRO, and although the combined company is still smaller than Exxon Mobil (XOM) and Chevron (CVX), I don’t expect major antitrust challenges.

I continue to rate COP as a buy, and while stocks often fall when mergers and acquisitions are announced, this is a pullback to buy. An 8% free cash flow yield for a leading, broad-based oil and gas company is attractive, and I see upside risk to the $20B 3-year repurchase target, assuming oil stays above $75. With production growth of 1% to 2% and cost discipline, even in a stable commodity environment, the new COP is capable of generating sustainable returns of 10% with higher oil prices as a potential additional catalyst. I expect shares to move toward $130 over the next year as buybacks reduce the share count, and we see the benefits of this deal coming into focus.