Georgijevic/E+ via Getty Images

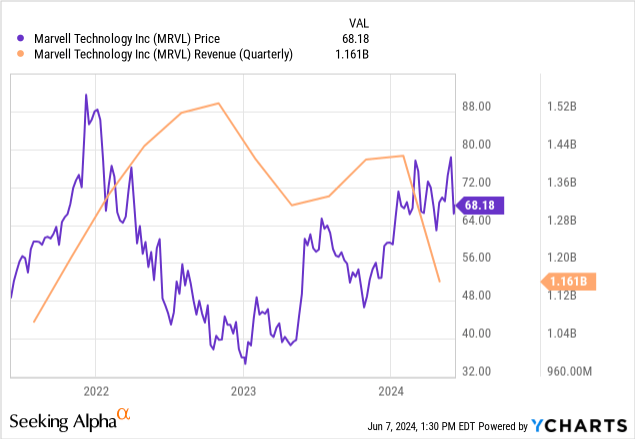

Marvell technology company (Nasdaq: MRVL) The stock price has been on a roller coaster ride over the past three years with shares falling from over $90 to around $35 in 2022 as a result of aggressive Fed policy Tightening monetary policy. Then May 2023 saw a rebound despite declining sales, driven mostly by AI hype.

Now, AI has emerged as a major driver of growth, but overall sales have been hit by cyclical fluctuations, punishing the stock, but that’s very difficult according to this thesis, which aims to show that it’s just a buy even if it’s a small piece of data center AI chip market share. It can make a huge difference to her income.

First, in an area prone to confusion, it is important to clarify how (dedicated cloud) and network connectivity segments are calculated Produced by Marvel is suitable for AI data centers in a market dominated by NVIDIA (NVDA).

Identify opportunities in computing and networking

The field of generative AI has been on the boil since the launch of Open AI’s ChatGPT in November 2022. Through its partnership with OpenAI, software giant Microsoft Corporation (MSFT) has beefed up its cloud and productivity tools, but it’s the company that has benefited the most financially . It is Nvidia whose graphics processing units for accelerated computing are in great demand for artificial intelligence data centers.

However, the semiconductor giant does not have a monopoly position, and it faces competition not only from Advanced Micro Devices, Inc. (AMD), but also from chips dedicated to artificial intelligence being developed by scale-ups like Alphabet Inc. (GOOG). Or (GOOGL) without forgetting Amazon.com, Inc. (AMZN), or Meta Platforms, Inc. (META), or Microsoft. These can represent 10% to 15% of the market share. Now, these AI-specific chips which are also called ASIC or Application Specific Integrated Circuits are mainly designed by two companies: Broadcom Inc. (AVGO) and Marvell, which owes its expertise following the acquisitions of Cavium and Avera in 2018 and 2019, respectively.

Furthermore, compared to Nvidia’s general-purpose GPU chip that is ideal for processing large data blocks due to its parallel architecture, ASICs, while also accelerating AI, are more customizable and optimized for training and inference (usage) of AI models and come integrated with the software development framework. of the cloud provider.

Looking deeper, Marvell’s initial shipment of custom AI chips was made in the first quarter of fiscal 2025 (FQ1-25) as part of its data center end market. However, computer chips are only part of Marvell’s AI story, as there are also networks that have already contributed strongly to its data center business through electro-optics products, used to connect cloud AI applications. This includes 800GB PAM products used in high traffic deployments.

Company presentation (www.marvel.com)

AI Networks revenues increased from approximately $200 million in all of fiscal 2023 to more than $200 million in FY4-24 alone, or a four-fold increase with increased production.

Therefore, the growth of the AI portion of the data center market is being driven first, by dedicated computing chips (ASICs) used to build AI servers and cloud communication (networking) chips to connect both front-end users and back-end storage portion of the data. These cloud-based chips have helped offset declines in enterprise on-premises products.

Evaluating artificial intelligence opportunities

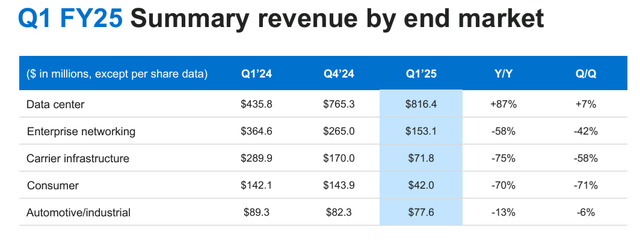

As a result, the data center business grew 87% year over year in the fiscal first quarter of 2025 that ended in April, and 7% sequentially, with AI (ad hoc computing and networking) accounting for about $500 million in sales out of a total of $816 million. dollar. Moreover, with increased production, analysts at JPMorgan Chase & Co. (JPM) expect between $1.6 billion and $1.8 billion in AI chip sales this year. This is possible because Marvell is a spin-off that outsources production to outside foundries, including Taiwan Semiconductor Manufacturing Co., Ltd. (TSM), meaning it can expand quickly.

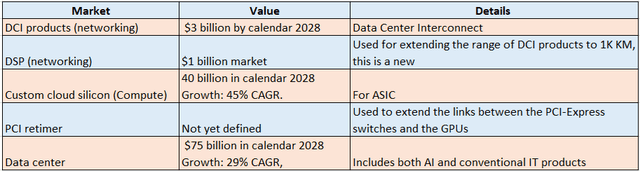

Furthermore, for fiscal year 2026, AI sales are expected to range between $2.8 billion to $3 billion which is roughly half of Marvell’s total revenue for FY24. Additionally, it is poised to benefit from Nvidia’s production of GPUs significantly Accelerated through its dynamic networking product roadmap with some customers qualifying (testing) next generation PAM solutions for 200GB per lane and DCI (Data Center Communications) 800GB products. In a market that is expected to grow to $3 billion by 2028. There are other growth markets as shown below.

The table was prepared using SeekingAlpha.com data.

This table shows that in addition to the networking portion of AI data centers, there are opportunities in computing (custom cloud silicon), where the company boasts some key design wins including Google on a 5-nm Axion ARM CPU chip, and Amazon on a 5-nm chip. Tranium type, without forgetting Microsoft on its Maia chip.

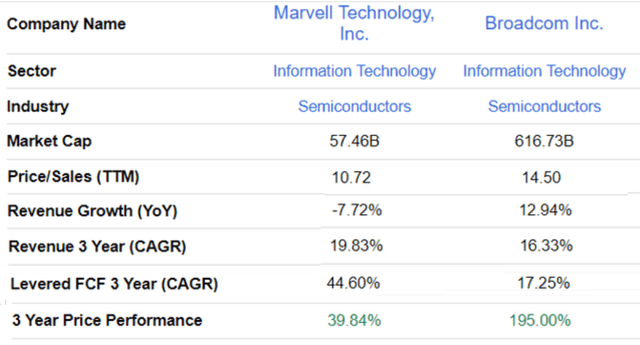

Deserves better based on comparison with Broadcom

So, the company deserves better value but the problem is that its trailing price of 11.27x sales is already overvalued compared to the IT sector by more than 270%. However, comparing it to the broader sector ignores its AI potential which makes a comparison with Broadcom which trades at 14.5x more relevant. Thus, for those looking to diversify into the data center AI chipset space, Marvell is an opportunity and could appreciate in value by 35% ((14.5-11.27)/11.27), based on its undervaluation compared to Broadcom.

SeekingAlpha.com

Applying 15% to the current stock price of about $68, I got $78.3, which is what the stock has reached several times as shown below. Moreover, this was its peak before the Fed aggressively raised interest rates, and was then reached again at the end of May just before the drop.

Justify your target price (SeekingAlpha)

To further justify my bullish stance, the company’s three-year performance remains well below Broadcom’s even though its three-year revenue and FCF growth exceeds the latter as shown in the comparison table.

However, investors will note that this target is well below Wall Street’s average target of $89.41, but is justified given the risks of operating in a cyclical industry.

Cyclicality risk but may outperform the main line based on data center strength

The FQ1-25 revenue breakdown as shown below indicates that Marvell was facing a serious decline due to its exposure to enterprise networking, transportation infrastructure, automotive, and consumer markets. Progress has only been made in the data center sector which includes the AI growth engine.

So, the risk here is that with interest rates still above 5% and inflation still above 3%, economic growth suffers. To that end, GDP growth during May was revised downward from 2% to 1.8% by the Federal Reserve Bank of Atlanta following news of weak manufacturing.

www.marvell.com

However, the economy remains resilient according to the May Nonfarm Payrolls report. However, as an interest rate-sensitive stock, Marvell has been impacted as economic resilience suggests the Fed cannot begin to ease its fight against inflation. So, it’s possible the stock could fall further, but I think it should receive some support during Q2FY2025 financial results based on the strength of the data center.

This is due to the annual labor productivity benefits (up to 0.6%) that it generates, and that AI is being rapidly adopted and becoming a secular trend just like digital transformation, but to make super-intelligent applications widely available, data center infrastructures need to be revamped.

Thus, according to Gartner, spending on data center systems is expected to rise from 4% in 2023 to 10% this year, mostly driven by the AI generation. Now, that’s double the 5% (mid-point numbers) that Marvell expects in its fiscal Q2 2025 financial outlook. So, with strength in its data center business, the company could exceed its $1,250 billion (midpoint) sales guidance ( Pictured below), causing the stock to rise.

SeekingAlpha.com

This performance could be further helped by a recovery in the consumer business where sales are expected to double sequentially, which is in line with industry-wide expectations for an accelerated recovery in the video game market this year compared to last year’s weak growth. For the remaining segments, revenue growth is expected to be flat but resume in the second half. This is supported by the fact that inventory in the first quarter of fiscal 2025 fell by 20% year-on-year and is now approximately the same level as in 2022.

Even a small piece of a data center’s AI chip means a lot

In conclusion, this thesis made a case for investing in Marvell which is gaining market share in AI chips for data centers spanning both computing and networking.

Looking specifically at compute, AI servers are expected to account for roughly 60% of total server spending in 2024. Now, even if Nvidia is expected to dominate this market with a 75% share, this will still be a $200 billion market dollar. By 2027 according to the latest update from BofA Securities. Now, even if Marvell gets 3% market share out of a possible 10% to 15% with Broadcom enjoying the rest, that would imply revenues of $6 billion for FY27. Interestingly, this would be $500 million more than Its total revenue for FY24.

So, even a small piece of the AI chip pie in the data center could make a big difference for Marvell given its small size.

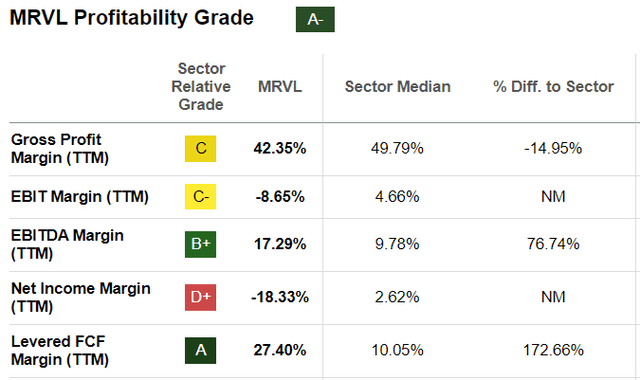

On the other hand, gross margins from hypermarkets are expected to be lower than from enterprise customers for a company already experiencing an operating loss due to higher R&D expenses. However, since it has already made the bulk of investments in 2018-19, capex remains relatively low resulting in free cash flow margins of 27.4% which exceeds the IT sector average by more than 170% as shown below.

SeekingAlpha.com

Moreover, this number is expected to rise in FY25Q2 as cash flow from operations will increase as it will not include the payment of annual employee bonuses. Therefore, it can continue to pay dividends and make stock buybacks, equipped with $848 million in cash against $4.15 billion in debt. However, the debt-to-equity ratio is 30%.