John M. Lund Photography/DigitalVision via Getty Images

We have initiated coverage of the Matthews Pacific Tiger Active ETF (NYSEARCA: Asia) with a sell rating.

ASIA is an actively managed ETF focused on companies based in Asia excluding Japan, including emerging and Frontier markets. The fund aims to invest in companies with strong growth, sound balance sheets, sustainable cash flow, and capable management teams. The fund can invest across all market caps but mainly focuses on mid- and large-cap companies.

Our sell recommendation is driven by several key concerns, including high turnover among the fund’s management team, significant exposure to China in light of elevated geopolitical risks, and weak absolute and relative performance over the long term.

A team in turmoil

In December 2023, three portfolio managers, including former co-lead manager Sharat Shroff, who had been with the firm since 2008, left Matthews International Capital Management, The company that also launched and manages the Matthews Pacific Tiger Active ETF (ASIA). Even absent our other concerns about the strategy, this level of turnover at the senior investment team level is significant enough to seriously consider, if not justify, a sell rating for the fund.

While we believe current co-lead manager Inbuk Song and the four co-managers have strong credentials, the turnover in Matthews’ senior investment team calls into question whether the current team can successfully execute the firm’s investment process and deliver better results for investors. Sean Taylor, IT director at Matthews and co-lead director of ASIA along with Song, emphasized efforts to optimize position sizing, portfolio construction and risk management across the firm’s investment strategies. However, it remains to be seen whether these initiatives can turn around the Fund’s disappointing results. In our view, the exodus of investment talent from Asia is worrying and disruptive. In addition to Shroff’s recent departure, emerging markets director John-Paul Lech and Japan specialist Taizo Ishida also left the company last December. Since the end of 2019, investors have withdrawn approximately $19 billion from Matthews’ funds, with assets under management falling from $27 billion to $8.0 billion as of May 31, 2024. Given the -70% decline in the firm’s assets under management over a relatively short period, We have serious concerns about the company’s long-term viability. Barring a material and sustained improvement in performance, we believe this trend is likely to continue.

Asia: A closer look at the portfolio

While ASIA was just launched in September last year, its mutual fund counterpart (MAPTX) has a much longer history dating back to 1994. To gain long-term insights into the portfolio and strategy performance under which ASIA is managed we review And discuss the historical portfolio and performance of MAPTX which implements the same strategy and is managed by the same team.

Given the strategy’s growth orientation, the fund has historically overweight consumer discretionary stocks and high-growth technology stocks. From a geographical perspective, the fund’s exposure is very similar to its benchmark index – the vast majority of the fund is concentrated in China, Hong Kong, India, Taiwan and South Korea.

As of March 31, 2024, more than 30% of the fund was invested in China/Hong Kong. Given the growing tension between the United States and China, global efforts to reduce supply chain dependence on China, periodic government crackdowns on various sectors, and the ongoing crisis in the real estate market, we have difficulty feeling comfortable maintaining significant exposure to China today. Importantly, Asia does not have to maintain this level of exposure to China and Hong Kong – its mandate is broader and includes all developed, emerging and frontier markets in Asia (except Japan). As such, we would have preferred the team to reduce focus on China in light of these risks.

From a sector perspective, we generally believe that the fund’s main fishing ponds, which are the consumer and technology fishponds, are typically fertile ground from a business quality perspective. However, while some of the fund’s most important holdings, shown in the table below, are trading at material discounts to their developed market peers, many of these stocks do not look very cheap compared to history.

Collectibles and Valuation

Asia: Top 10 Properties (Matthews Asia)

For example, even though Taiwan Semiconductor Manufacturing (TSM) is at about 11 times EBITDA and is trading at a significant discount to Advanced Micro Devices (AMD) at nearly 50 times EBITDA EBITDA, the fund has seen meaningful multiple expansion – with NTM EBITDA nearly doubling since then. October 2022. So despite what may look like an attractive discount compared to developed markets, we would not be surprised to see multiple compression across the portfolio geared toward large-cap growth in Asia, particularly in stocks more exposed to China and the associated geopolitical risks.

On an overall portfolio basis, as of March 31, 2024, the Asia portfolio traded at 15.3 times 12-month forward earnings and 13.2 times 24-month forward earnings, a premium to its benchmark (MSCI All Asia Ex Japan Index) at 13.2. x and 11.7x, respectively. The fund’s price-to-cash flow of 10.9x also exceeds the benchmark multiple of 8.4x. To be fair, the fund’s total 3-year forward EPS growth is more than double that of the index (26.1% vs. 12.6%), so we expect Asia stocks to trade at a premium to their benchmark index.

However, as we discuss in more detail in our assessment of the fund’s historical performance, Asia has not been rewarded for its drive towards more expensive, higher-growth businesses. We believe that investing in these types of businesses becomes more difficult in a higher interest rate environment for a longer period.

performance

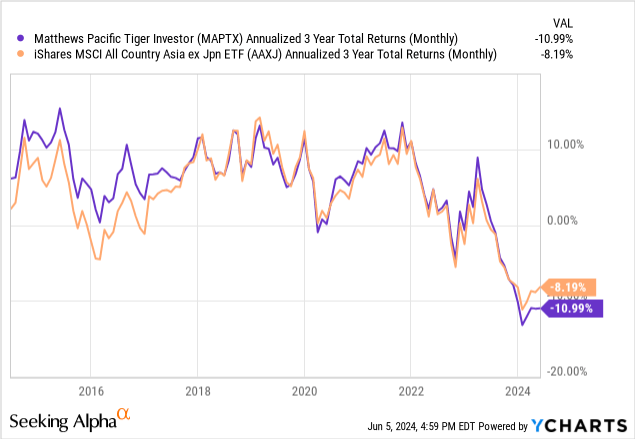

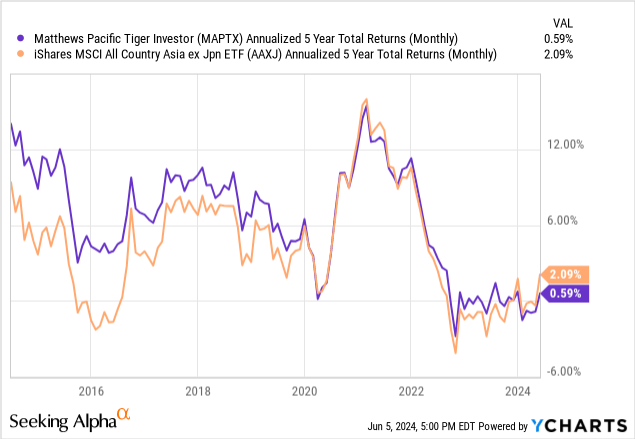

Using MAPTX as a proxy for the long-term performance of ASIA and the strategy, the strategy has underperformed its benchmark over almost all meaningful trailing periods, including over the 1-, 3-, 5-, 10- and 15-year trailing periods. .

As shown in the charts below, the strategy’s 3- and 5-year rolling returns highlight the strategy’s challenging performance, particularly over the past three to five years.

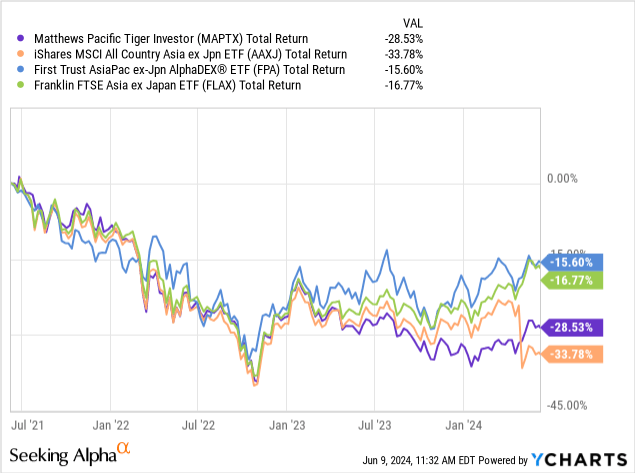

For more context on Asia’s performance, the chart below shows the fund’s total return over the past three years compared to funds with similar exposure, such as the iShares MSCI All Country Asia ex Japan ETF (AAXJ), and First Trust Asia Pacific Ex-Japan AlphaDEX Fund ETF (FPA). , and Franklin FTSE Asia ex Japan ETF (FLAX). To be fair, this has been a difficult area to invest in, as evidenced by the disappointing returns of all these funds. However, Asia (represented by MAPTX) is among the worst performers in this group, only slightly outperforming AAXJ over this period.

Given what we view as several significant headwinds working against the strategy – team turnover, geopolitical risks, valuations – we struggle to find catalysts in favor of Asia’s future performance at this stage.

There is no shortage of risks

As previously noted, beyond the recent change in senior investment team staff, as well as what appears to us to be an insufficient margin of safety, Asia is exposed to macroeconomic and geopolitical risks, particularly in Chinese and emerging market companies which are of great importance. Revenue exposure to China.

Tensions between the United States and China, the global effort to reduce supply chain dependence on China, periodic government crackdowns on various sectors, and the ongoing crisis in the real estate market all pose significant potential risks to Asia. Furthermore, a portfolio orientation towards higher growth stocks and sectors may also underperform if there is a sustained rotation of value into a higher interest rate environment for a longer period.

Summary – Selling Case

In summary, our recommendation to sell in Asia is driven by several key concerns, including high turnover among the fund’s management team, significant exposure to China given elevated geopolitical risks, and weak absolute and relative performance over the long term. The exodus of the Fund’s investment talent is concerning and disturbing, and we have doubts about whether the current team can successfully execute the firm’s investment operation in light of the high staff turnover and material decline in assets.

While some of the fund’s holdings are trading at a discount to developed market peers, we don’t think valuations look too cheap compared to history. We also believe that investing in high-growth companies becomes more difficult in a higher interest rate environment and for a longer period.

As such, we have initiated coverage of ASIA with a Sell rating and will continue to monitor the company and its strategy for improvements related to our key interests.