Gazert

Medicinal Properties Fund (New York Stock Exchange: MPW) is a multinational real estate investment trust specializing in the ownership and leasing of acute care hospitals and other healthcare facilities. The company has been dealing with headwinds centered around increasing interest rates and tenant issues. I have It was more Supportive for investors who hold medical real estate debt In exchange for shares. Following Q1 earnings, I am increasingly concerned about the company’s ability to fund its dividend and downgraded its high-yield debt rating to hold.

FINRA

First Quarter Earnings – Impact of Steward’s Bankruptcy

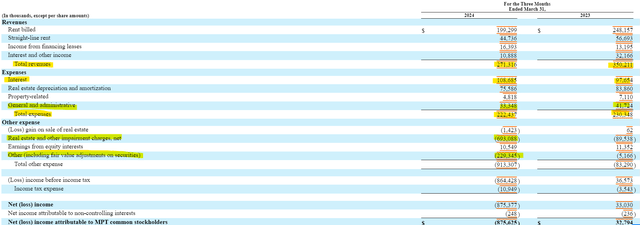

Steward Health, Medical Properties Trust’s largest tenant, recently filed for bankruptcy after the company was unable to turn around its operations. In its income statement, Medical Properties wrote off more than $900 million in real estate impairments and fair market adjustments (non-cash settlements), partly related to Steward’s bankruptcy. Revenues decreased by approximately $80 million, or more than 20% The first quarter of last year. Expenses were down, but nowhere near as revenues were down. The company is profitable without non-cash adjustments, but the downward trend is worrying.

10-h seconds

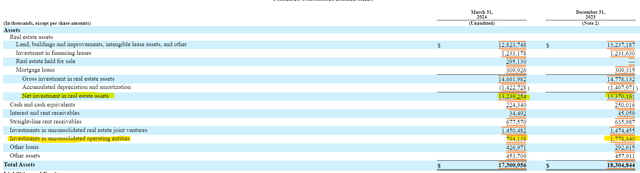

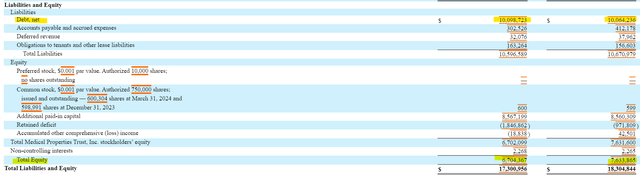

A closer examination of the write-downs shows the impact on the Medical Properties Fund’s balance sheet. The company wrote off its $361.5 million loan to Steward, its $35.6 million equity investment in Steward, its $226 million international joint venture, $120 million in investment with Priory Group, and $200 million in investment with PHP Holdings (also known as Prospect). . The roughly $1 billion investments may not have had a cash value, but they took $1 billion worth of assets off Medical Properties’ balance sheet and were the only contributor to equity, falling from $7.6 billion to $6.7 billion in one quarter. There is also a risk to the potential investment remaining for dilution as management reviews its value on a quarterly basis.

10-h seconds 10-h seconds 10-h seconds 10-h seconds

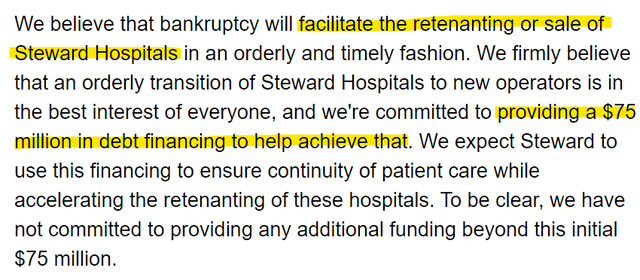

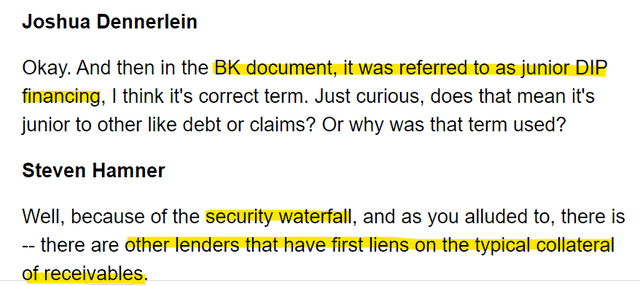

Management is optimistic that Steward’s bankruptcy will have a smooth outcome through the sale or replacement of Steward in its hospitals. Medical Properties Trust has committed an additional $75 million to fund Steward’s restructuring efforts. The DIP financing is small compared to some of Steward’s working capital debt, so it’s important for investors to realize that risks still exist. When it comes to rents, medical properties should see a positive outcome as was the case with Pipeline Health System, although it may take some time for rent collection to take effect.

Earnings call transcript Earnings call transcript 10-h seconds

Dividend anxiety

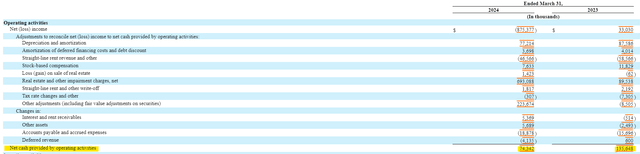

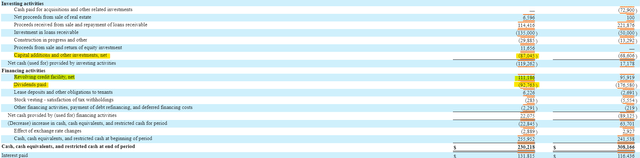

Medical Properties Trust’s cash flow statement highlights my concern about the viability of the dividend. In the first quarter, operating cash flow nearly halved compared to the same quarter last year. When accounting for capital expenditures, free cash flow turned negative in the first quarter compared to $67 million in the first quarter of last year. Because of its free cash flow burn and $92 million dividend obligation, Medical Properties Trust was forced to borrow $111 million from its revolving credit facility. Borrowing money to cover dividends is not sustainable.

10-h seconds 10-h seconds

Liquidity and debt maturities

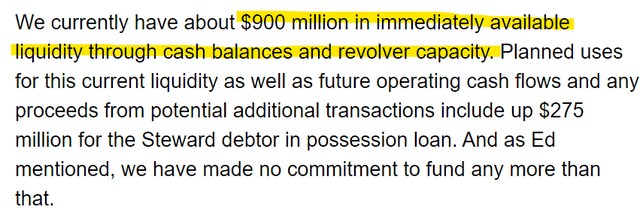

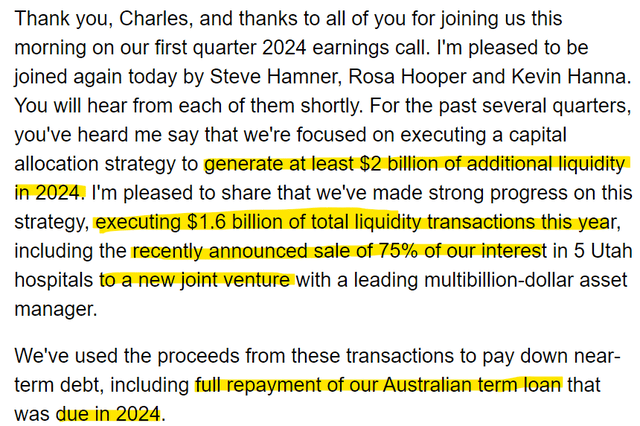

Management noted on the conference call that there is approximately $900 million of liquidity available under the revolving credit facility. In addition, the company is generating additional cash by selling assets and seeking secured financing. Following the end of the first quarter, Medical Properties Trust successfully closed a secured term loan on its UK properties which will fund its sterling loan maturities in 2024 and 2025.

Earnings call transcript Earnings call transcript 10-h seconds

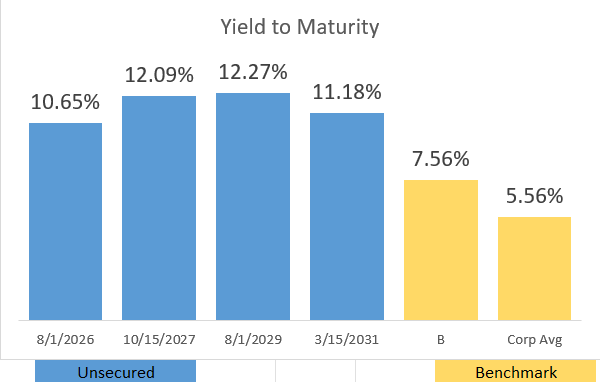

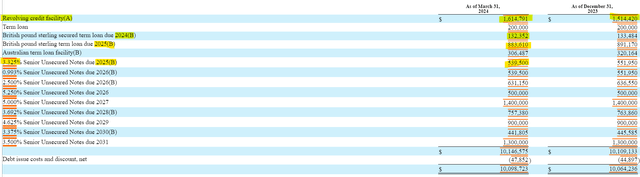

While the company is proactive about handling its 2024 and 2025 debt maturities, investors should be mindful of the more than $3 billion debt wall that will mature in 2026. Additionally, between 2025 and 2026, there is more than $2 billion of unsecured bonds due at below market interest rates. I think Medical Properties Trust will be able to refinance and perhaps pay off some of that debt, but even with the secured terms, it’s looking at an interest rate of about 7%, which puts more pressure on earnings, cash flow, and dividends. Sustainability.

10-h seconds 10-h seconds

Conclusion

While Medical Properties Trust has much higher yielding debt than its peers, I’m downgrading the bond to hold because the coupon (income) yields are lower and I’m not sure how long management will tap into liquidity before addressing the dividend. I don’t see any immediate catalysts that would boost the value of the company’s bonds or stocks. With dividends at risk, and no guidance on when the cash flow situation will rebound, I would advise income investors to avoid the stock.