Robert Y

Meituan ( OTCPK:MPNGY ), after starting out as a leading on-demand food delivery platform in China, has branched out into adjacent service offerings such as hotels and in-store travel, as well as several other new business initiatives. While this has allowed Meituan to build one of richest app ecosystem in the country, and it also came at a heavy P&L cost (one of the main concerns I highlighted in my post Previous coverage) and poor stock performance for a long period. It’s no surprise, then, that investors are more optimistic following management’s recent shift from growth to profitability.

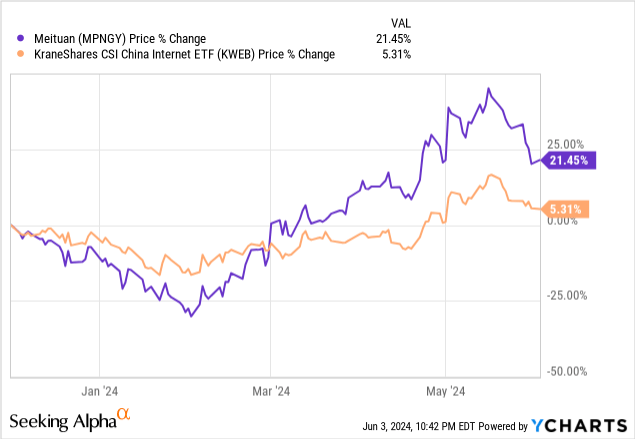

Despite the rally in recent months, the low valuation (forward P/E ratio versus earnings growth of over 70%) suggests the market remains skeptical of a sustainable turnaround. This means there is still plenty of upside ahead of Meituan’s quarterly results, when the restructuring progress is due to be updated. As for the long-term outlook, all eyes will be on management Future expansion approach; Emphasizing a more prudent approach will only add more strength to this rally.

Meanwhile, there is also a capital return story unfolding, with Meituan’s strong net cash position poised to support a much larger buyback once the current $1 billion program expires. Overall, I’m more bullish on the stock at this point.

All eyes on Meituan choose as focus shifts to profits

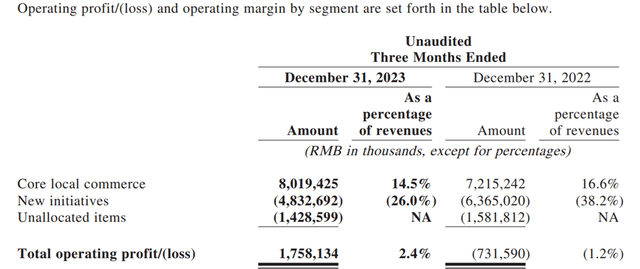

While Meituan has undoubtedly achieved market share gains and growth over the past few years, the company has also destroyed far more shareholder value than it has created. The main reason is management’s inability to translate this growth into profitability (i.e. increased operating leverage) within its many new business ventures. While microfinance and some shared economy initiatives such as Meituan Power Bank (a platform for leasing shared power banks) are suffering a decline, the rest of its new business portfolio, including its international ventures, is making losses.

The biggest P&L returner of all is Meituan Select, its community grocery business, which contributed the vast majority of its new business losses last year. In this context, a comment from a recent earnings call that highlighted steps to not only narrow losses at Meituan Select but also streamline the rest of its new business portfolio came as welcome news.

Meituan

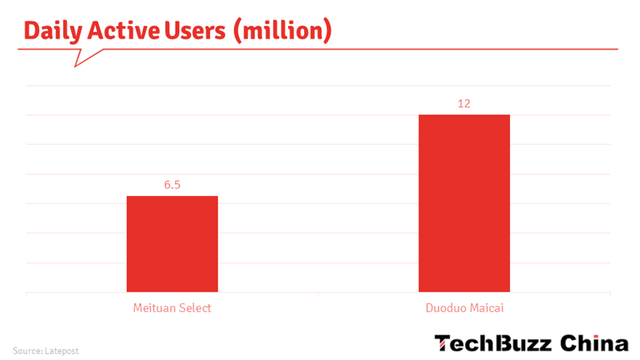

Overall, this seems like the right move – even if it means sacrificing future benefits. First, competition is intense in the Chinese grocery space, and investors simply have no desire to fund a subsidy-led race to the bottom with better-capitalized players like PDD Holdings (PDD) and its Duoduo Grocery arm (the current leading player by daily active users).

TechPaz China

So instead of chasing operating leverage, prioritizing the most profitable areas makes more sense here; This in turn should unlock P&L gains through better overall pricing and reduced subsidies, as well as reduced logistics burden. To be clear, implementation will not be easy, with industry growth slowing in China. However, if the latest quarterly numbers are any indication, I wouldn’t be surprised to see new business losses further narrow next quarter. Moreover, indications of a more prudent approach by management in its new overseas ventures also deserve attention.

Core restructuring efforts to unlock synergies

Outside of the new business portfolio, there may also be a fair amount of P&L that can be unlocked through Meituan’s restructuring of its two core businesses, food delivery and in-store services. To recap, management will consolidate leadership in its No. 1 vertical, food delivery, with its much less dominant in-store business, which currently faces stiff competition from another well-funded tech startup, Douyin. After the integration, both companies will be supervised by former food delivery business head Bozhong Wang.

On paper, at least, the evidence of restructuring seems clear enough. After all, both the food delivery segment and the in-store segment serve an overlapping merchant/customer base, so combining these segments should result in savings. Early details from management confirm this, highlighting the usual cost (think consolidated R&D and administrative functions) and revenue synergies (cross-selling). It may be too early to guarantee full benefit, although given the current outlook, good execution should revalue the stock.

Net cash position sets the stage for a repurchase surprise

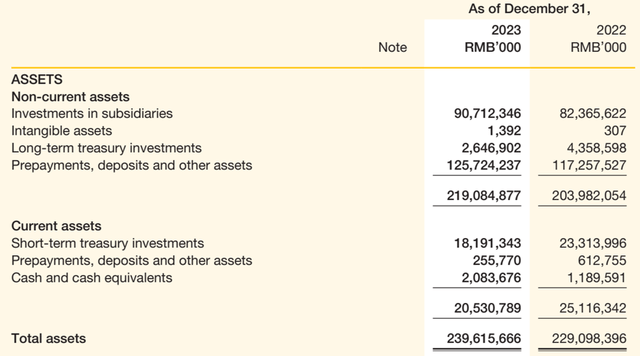

The final leg of the near-term uptrend lies on Meituan’s balance sheet. Recall that the company has a net cash and equivalents position of about US$15 billion (or about RMB 110 billion), which it has already put to work through a US$1 billion share buyback in the first quarter of 2024. Since more than Half of this allocation has already been made. However, the question now is whether Meituan will increase its size once the current buyback process ends.

Meituan

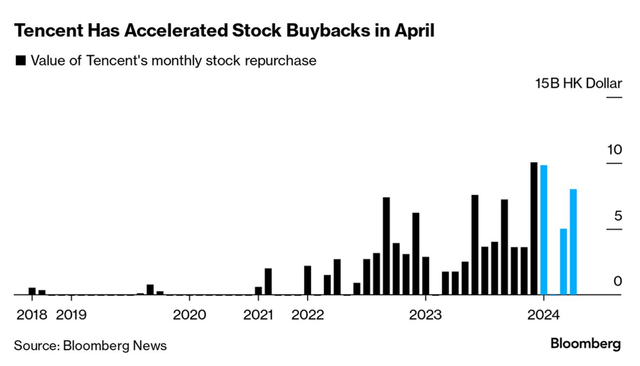

I lean towards the positive – perhaps in the next quarter. First, the company has very manageable debt repayment obligations on its balance sheet. Even if we take into account external investments and capital expenditures, it is very easy to finance this through the company’s core cash-generating businesses. Finally, there has been regulatory pressure to deliver more shareholder returns this year (through China’s “nine-point guidelines”). With well-capitalized tech peers like Tencent ( OTCPK:TCEHY ) and Alibaba ( BABA ) already responding with an enhanced pace of buybacks, it seems inevitable that Meituan will follow suit.

Bloomberg

Cut your way to profit growth

Meituan has been under intense pressure due to its loss-making new business portfolio for some time, but with management now prioritizing profitability, the stock may be worth a second look. Not only is there earnings upside to be unlocked from direct exits and cost-cutting, but restructuring its core business portfolio could yield far greater synergies than many expect. From here, expect more evidence of good execution to continue the stock’s re-rating from its relatively cheap ~17x forward EPS (versus over 70% EPS growth a year ago). Also watch for an increase in the size of the buyback program, especially in light of regulatory incentives and a growing net cash position.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.