RUNSTUDIO/DigitalVision via Getty Images

Ministry of Foreign Affairs Finance (New York Stock Exchange: Department of State) is a real estate REIT that has some interesting things going on at the moment. The dividend yield is trading at a high of 13%, and this also comes with a discount for booking value.

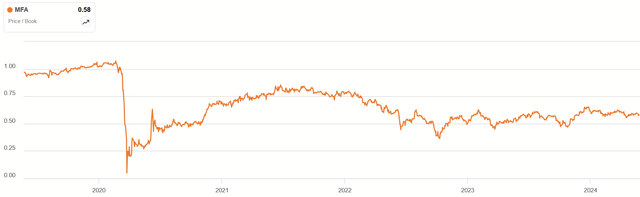

MFA price/book history 5 years (Searching for Alpha)

At 0.58, this seems like a significant discount. Also during this period, the company made some changes to its strategy to avoid some of the risks of the past. After examining where they are in the process, I ultimately concluded that the MFA remains on hold until further progress is made in its transformation.

Financial history

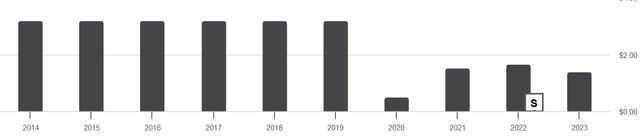

When looking at a REIT’s financial results, one of its biggest tests is how well it maintains its earnings per share. In the past few years, we can see that the Ministry of Foreign Affairs has struggled to maintain it.

Seeking alpha

After 2020 and the emergence of the Corona virus, dividends were reduced and did not return to their previous levels. This is due, in large part, to how the pressures of the pandemic have led to a reduction in the size of its balance sheet.

Author’s presentation of 10K data

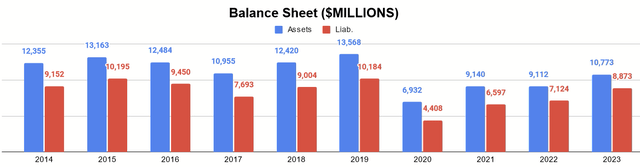

2020 saw the balance sheet cut by more than half. This was not unusual for mREITs at the time, as the coronavirus collapse created liquidity difficulties for many of them that used market-to-market financing and thus faced margin calls. In Q1 2020 earnings, CEO Craig Knutson said:

It was clear to us in late March that our situation was not due to bad assets, but rather fragile financing, and that the way forward would require more sustainable forms of financing. We also recognize that a term financing margin holiday and/or off-market financing will necessarily require higher write-downs and therefore more capital.

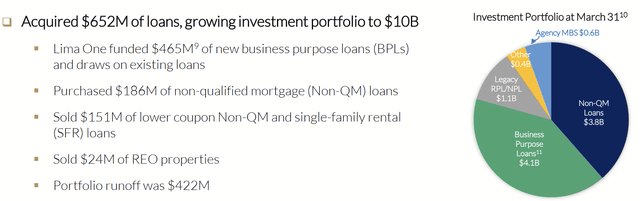

So, while they updated the funding situation, that wasn’t the only change that happened. In 2021, they acquired Lima One, which provides business-to-business loans (“BPLs”) to real estate investors, and these loans make up a growing portion of their investment portfolio. Management continued its strategy to grow its leverage through 2023, noting in its 2023 Form 10K (page 41):

…We believe our commitment to prudent risk management, hedging and prioritization of non-market financing has allowed us to add $3.4 billion to our target assets at increasingly attractive returns. These additions included more than $2.1 billion in funded originations of commercial purpose loans and draws on existing Lima One bridging loans, approximately $880 million in non-QM loans, and approximately $460 million in agency mortgage-backed loans. Reflecting the impact of our strategy, for the year ended December 31, 2023, the yield on our average interest-earning assets increased by approximately 100 basis points, while our effective cost of funds increased by approximately 40 basis points for the year ended December 31, 2022.

So the company is still developing its financing methods, and it is worth considering the type of business it is currently in.

Business model

MFA primarily originates and acquires BPLs (through LIMA) and non-qualified (non-QM) mortgages. The rest of its portfolio contains other types of mortgage assets, largely non-performing whole loans that are purchased at a discount.

Company presentation for the first quarter of 2024

They have been steadily rotating their assets into these concentrations in BPLs and non-QM loans.

Cropping schedule for distributable profits (2023 10K model)

At the same time, Lima’s assets had an increasing contribution to distributable earnings (profits available for distribution as dividends).

Company presentation for the first quarter of 2024

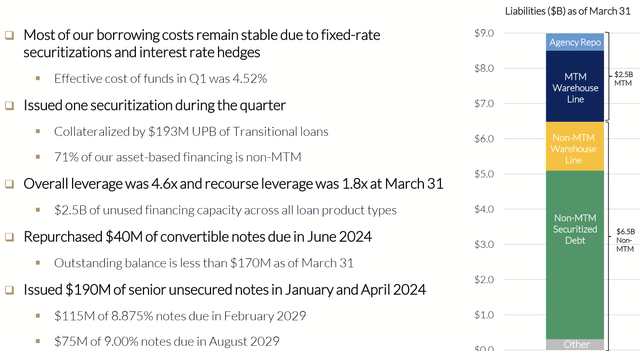

Meanwhile, about 28% of its liabilities are market-to-market financing sources.

Company presentation for the first quarter of 2024

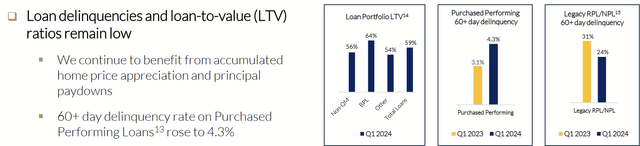

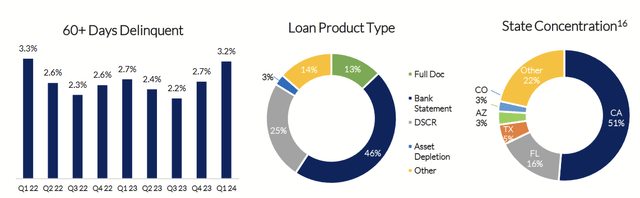

Importantly, although delinquency rates on these loans have risen as of Q1 2023, they remain relatively low at 4.3%.

Company presentation for the first quarter of 2024

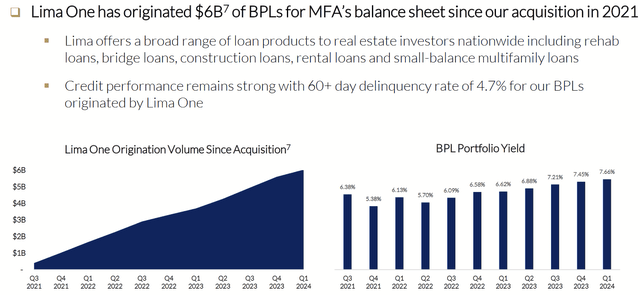

At the same time, Lima One loans enjoyed high yields, low interest rates, and a steady flow of new assets.

Company presentation for the first quarter of 2024

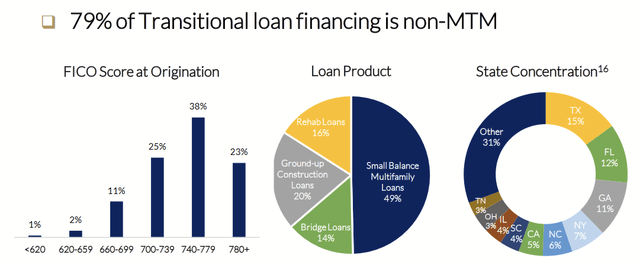

Lima One’s loans are largely multifamily, with approximately half in Texas, Florida, Georgia, New York and North Carolina.

Company presentation for the first quarter of 2024

Meanwhile, non-QM loans are highly concentrated in California and, to a lesser extent, Florida.

a future vision

Overall, I see the situation improving for MFA as they continue to pivot from their legacy strategy and focus on originating the loans themselves through Lima One, which I think comes with some skin in the game that not all mREITs have. However, there are two concerns that I would like to highlight.

Interest differences

While their loan coupons are high, their new financing coupons are also high. In their Q1 2024 earnings, they reported that their most recent bond in April yielded 9%. Regarding the asset purchase, Knutson said:

In some cases, it may make sense to call for a deal and re-leverage the underlying loans in a new securitization. Even if the cost of debt is slightly higher than in an existing deal, buying and re-leveraging can unlock significant additional liquidity, which we can redeploy at attractive returns on equity. These communication rights provide an often underappreciated option that we must improve our responsibility framework in the years ahead.

While he may be right here, this creates additional pressure on distributable profits.

Company presentation for the first quarter of 2024

If interest rates do not fall at a fast enough rate, I fear it will lead to unnecessary losses requiring a cut in quarterly dividends, which now equal DE.

Missing on buybacks

Management also announced that the board has approved a $200 million stock buyback program, which currently represents about one-fifth of market capitalization. Knutson explained:

I will also note that we simultaneously updated our share repurchase authorization, and I would characterize both actions…as administrative in nature.

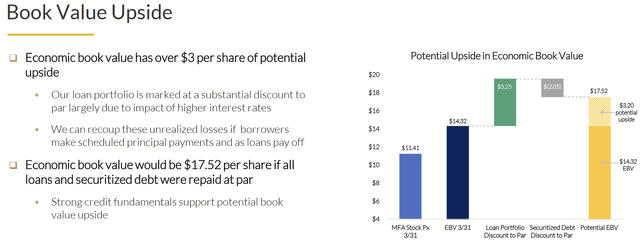

So this doesn’t drive buybacks at a really good price. As of Q1, the tangible book value per share is $17.79. With a 13% dividend, this is a great return on capital if it were bought back.

Company presentation for the first quarter of 2024

In the slide above, it appears that management believes there is some underappreciated value on its balance sheet. However, given DE’s tight cash flow and the ongoing shift in its financing, it seems to me that management is not as comfortable as it should be. There are companies using market pessimism to buy back their shares right now, and I see that as a major indicator of the financial strength of the company as they can create some room for that.

Conclusion

The MFA’s fair value at a reasonably high TBV, is $17.79. Over time, with the company’s active role in origination and re-leveraging opportunities to reduce interest expenses, we can see that and earnings improve.

Meanwhile, the reservation discount and current price under $11 is there for a reason. Stocks are likely to be fairly valued if interest rates do not change favorably for MFA, and if high rates persist and lead to more DQs in the future. While this may not eliminate the dividend, it does mean that the return on cost may not reach the full 13% over the next few years.

I believe that microfinance is close to being an attractive investment but it needs more time to deal with the current situation. Long-term investors would likely benefit from waiting to see them unwind the remains of MTM funding and achieve a lower payout ratio than DE. Meanwhile, microfinance is not the riskiest investment with the reforms made and is at least a favorable contract.