Monty Racusin

Investment summary

My recommendation for microchip technology (Nasdaq:MCHP) is a Buy rating. Management has already seen early signs of recovery, and this aligns well with my view that the bottom is near after two straight quarters of significant declines. declines and demand appears to have outpaced supply for the first time in FY24. If I am right about the timing of this recovery, I expect the market to continue valuing MCHP at this high multiple in the near term.

Business overview

MCHP designs and manufactures microcontrollers, mixed signal products, memory, security products and other analog related products. The existing business was formed through the merger between Microsemi and MCHP, expanding MCHP’s product portfolio and exposure to industries such as automotive, industrial and IoT. In terms of segment, MCHP generates the largest revenue from the sale of microcontrollers (56% of FY24 revenue), and Analog and Interface (ANI) revenue is the The second largest segment at 26.4%. The remainder includes technology and other licenses, MMOs, and FPGAs, which combined account for approximately 17.4% of FY24 revenue. Geographically, MCHP sells to a global customer base, the majority of whom are from Asia (about 47% of FY24 revenue), followed by the Americas by 29% and Europe 24%.

The bottom of the course is close

Redfox Capital Ideas Redfox Capital Ideas

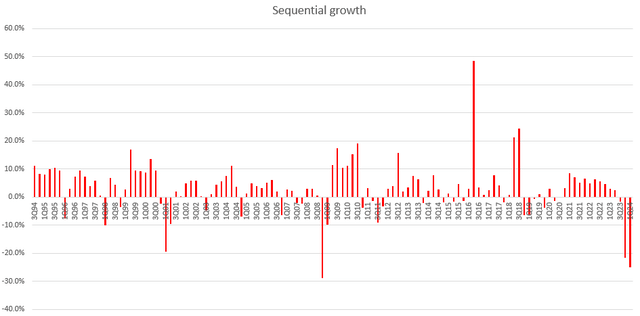

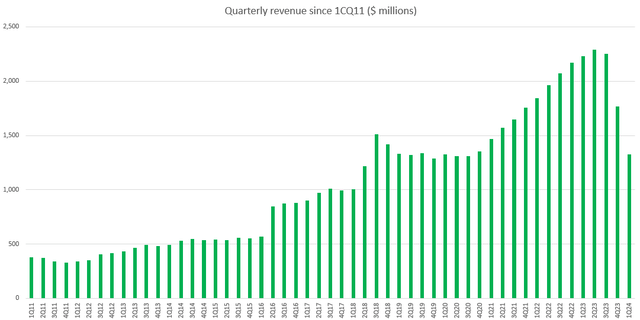

I think MCHP is approaching the bottom of the cycle. In Q4 2024, MCHP reported revenues of $1.33 billion, which represents a 25% sequential decline and a 41% year-over-year decline, and I note that this represents the largest consecutive sequential decline the company has faced since Q3 ’94. The dramatic downward cycle is largely due to the coronavirus situation. Although the coronavirus lockdown has ended, it has lasting impacts on the supply chain through 2023. Customers are worried about not getting the supplies they need in excess, resulting in a massive supply shock to the industry’s supply and demand dynamics . As a result, this led to a significant oversupply of stocks in the channels. Hence, I believe the management took the right decision to reduce deliveries significantly to get rid of excess inventory.

Redfox Capital Ideas

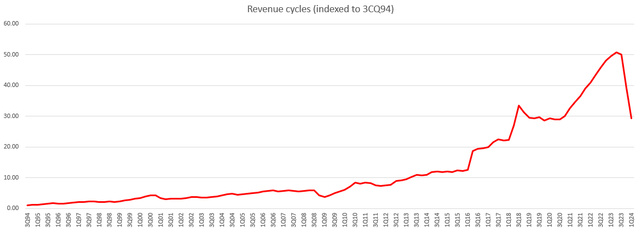

We can estimate the end market consumption level (for MCHP chips) by looking at MCHP’s historical quarterly revenue trend. As we all know, demand for chips has risen over the years due to the trend of digitalization (AI, data centers, IoT, etc.), and this is well reflected in MCHP’s revenue, which has grown from a quarterly trend of ~$500 million in the half The first from 2010 to nearly $1 billion between 2016 and 2018, followed by nearly $1.5 billion between 2019 and early 2021, before entering its most recent bubble moment as quarterly revenue topped $2 billion.

I believe the quarterly end market consumption level is between $1.5B and $2B, based on the flat quarterly revenue trend between 2019 and early 2021 (this was before the coronavirus outbreak, so there was no supply chain issue that impacted supply/supply ). demand dynamics), and the reason it’s over $1.5 billion is because the demand for AI (noted in the Q2 2024 earnings call, MCHP has the tailwind from anything and everything going into the AI space and the AI space year) may get more attention today than in 2019-2021. Assuming the current consumption level is ~$1.75B, this means that MCHP is lagging the market by about 25% (1CQ24 revenue of $1.32B/$1.75B), which means that demand has exceeded supply for the first time in this down cycle, that is A very positive sign.

Management’s comments about the order in progress also align well with my view. Specifically, they are seeing green shoots such as bookings growing for three consecutive months, a lower level of order cancellations and checkouts, an increased number of expeditments and withdrawals of shipments, and new bookings aging within a short period of time. The last point is important because it gives shipping management visibility into 2CH24, which gave me more confidence in management’s view that 2CQ24 could be the bottom and that 3CQ24 could see positive sequential growth.

I have confidence in this management team

The most important thing to learn from this session is that it showed us the quality of this group of management teams on two fronts. First, management is willing to take aggressive measures to protect the business in a downturn, as can be seen from their intention to further reduce chip startups: they will close its three main factories; Reducing capital expenditures by 51% (based on FY2025 guidance of $175 million); and reducing operating expenses, which fell sequentially by 9% in 1Q24 and are expected to decline another 3% in 2Q24. All of this has shown me that in a recession, management will find ways to shore up cash in the budget. Generality. Second, management has kept its capital return policy intact, with MCHP repurchasing a record $387 million worth of stock and paying a record $242 million dividend in the first quarter of 2024. Additionally, management stated that it still intends Increase total capital return compared to adjusted capital flows from the previous quarter by 500 basis points each quarter until it reaches 100% by March 2025. This shows that management does not lose sight of creating value for shareholders, even in a down cycle.

evaluation

Redfox Capital Ideas

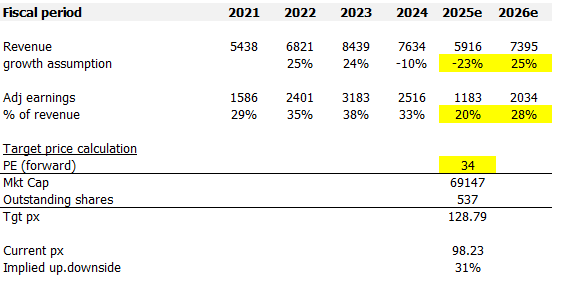

I model the MCHP using the forward PE approach, and using my assumptions, I think the MCHP is worth around $128. My basic assumption is that MCHP will see a recovery soon, most likely in FY26 (CY2025) as it moves through the final leg of this down cycle, which should bottom out in 1FQ25. I arrive at -23% for FY25 assuming that MCHP will see sequential improvements in YoY growth from -46% in 1FY25 to breakeven in 4Q25 before seeing a strong 25% recovery in FY26 (historically a recovery year growth In the general range of the high teens to high 30s ratio, I assumed the middle). Adjusted earnings in FY25 will definitely be affected because revenues are still declining, and I assume they will bottom out at 20%, which is the lowest level MCHP has seen in recent cycles. In FY26, as growth accelerates, margins should at least be able to return to FY21 levels. With a view to recovering soon, I expect the market to continue to support MCHP’s current high multiple of 34x forward PE.

risk

MCHP’s balance sheet inventory remains high as of fiscal Q4 2024, with days of inventory increasing to 224 days from 185 days in the previous quarter. Given that management’s goal is to reduce the duration to 130-150 days, this may put more pressure on margin than I expected. They will likely continue to reduce production by reducing utilization, which has a high margin of decline, to clear excess inventories on the balance sheet.

Conclusion

My view for MCHP is a buy rating as there are early signs of recovery and my analysis suggests a bottom is near. I expect a pickup in growth next year (25 years), and that should see the profit margin rebound accordingly. If so, I think the market would be willing to attach a high multiple to MCHP. Management’s commitment to shareholder returns through buybacks and dividends is another positive for the investment case.