lcva2

introduction

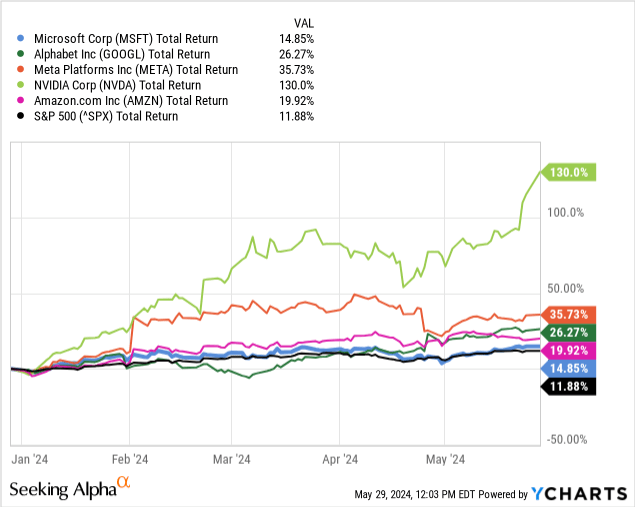

Microsoft Corporation (NASDAQ:MSFT) is locked in a bitter war with big tech rivals Alphabet Inc (GOOG/GOOGL) and Meta Platforms Inc. (META), NVIDIA Corp (NVDA), and Amazon.com Inc (AMZN).) among other things to win the provision of the best artificial intelligence services.

Recent stock gains in all of these names demonstrated the market’s appetite for these companies’ spending on AI R&D and acquisitions.

To this end, MSFT has undertaken a great deal of maneuvering to position itself ahead of others including massive spending on research and development, large acquisitions, and strategic partnerships with outside companies. These moves have given MSFT an advantage over the others mentioned above, and I believe will allow Microsoft to outperform its competitors and deliver its AI services to end users faster and with greater success.

Financial review

I won’t delve too deeply into this section since my primary thesis is about MSFT’s efforts in AI, but it is necessary to provide some overview to understand MSFT’s work.

There are several aspects I want to highlight:

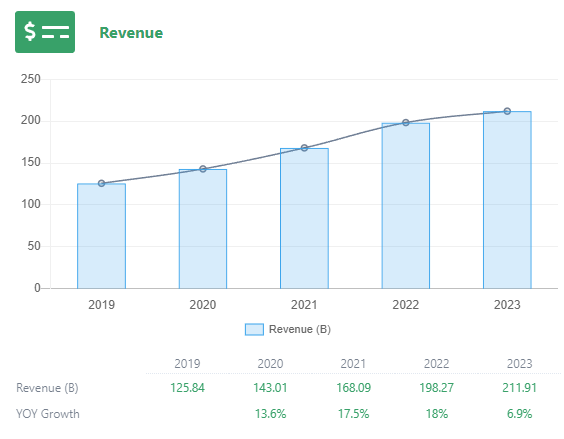

High revenue

Figure A (grasshopper shares)

This is critical to MSFT’s future success, especially as training new AI models and optimizing Azure (the primary delivery method for AI) becomes more expensive and erodes profits without further revenue growth. The mid-teens annual growth in 2020, ’21 and ’22 really showed how much MSFT has grown in the past few years, exceeding previous expectations.

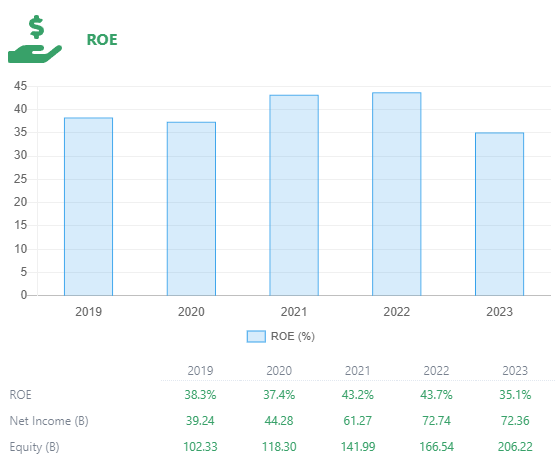

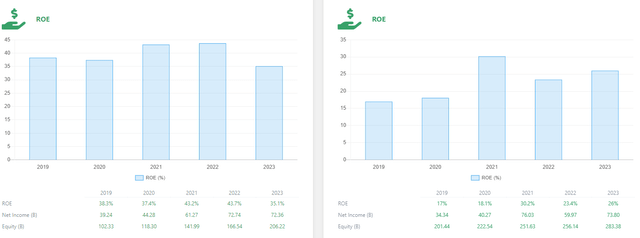

Return on equity is consistently positive

Figure B (grasshopper shares)

Return on equity is an important factor to consider because it tells us how much value shareholders actually gain each year from a company’s net assets. MSFT carries a positive ROE on average. In 2023, there was a whirlwind where income did not grow, but assets did. This has resulted in lower ROE than the last few years, but staying above 35% is still impressive.

Compare Microsoft (left) to Google (right) in this next graphic, where we can see consistently half the same ROE as MSFT.

Figure c (grasshopper shares)

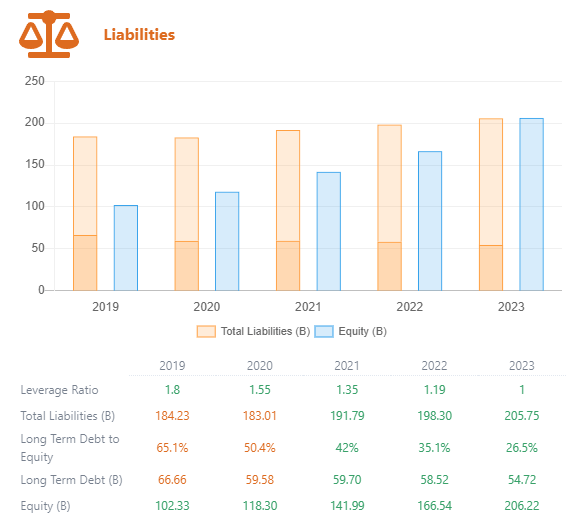

Liability ratio

Figure D (grasshopper shares)

While we can see growth in total liabilities over the past five years, there has been a recent trend of reducing long-term debt and increasing equity, which has resulted in the debt-to-equity ratio falling from 65% in 2019 to 27% in 2019. 2023. This is a very positive sign for MSFT because it shows that its debt is under control and it is reducing it while interest rates are high, so it will have less impact on its bottom line.

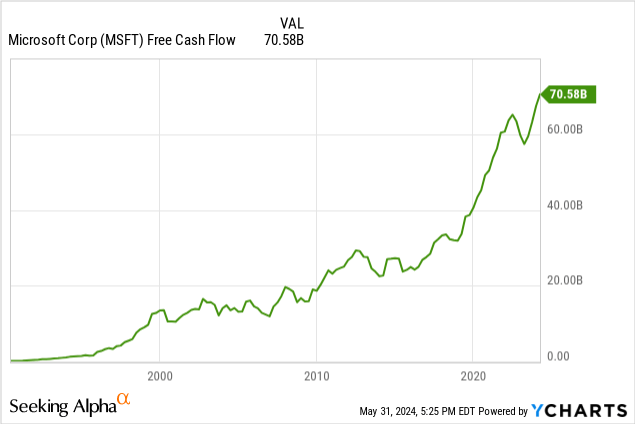

Beyond these big numbers, I also want to highlight MSFT’s free cash flow, which is one of its strongest points financially. MSFT is cash-rich, which has been a boon for the acquisitions and talent hiring it has made in the past few years.

Although we saw a decline last year, this year MSFT is on track to outperform and increase free cash flow. This means they will have more dry powder for future acquisitions, which may be necessary to further develop the new AI division (more on that later too).

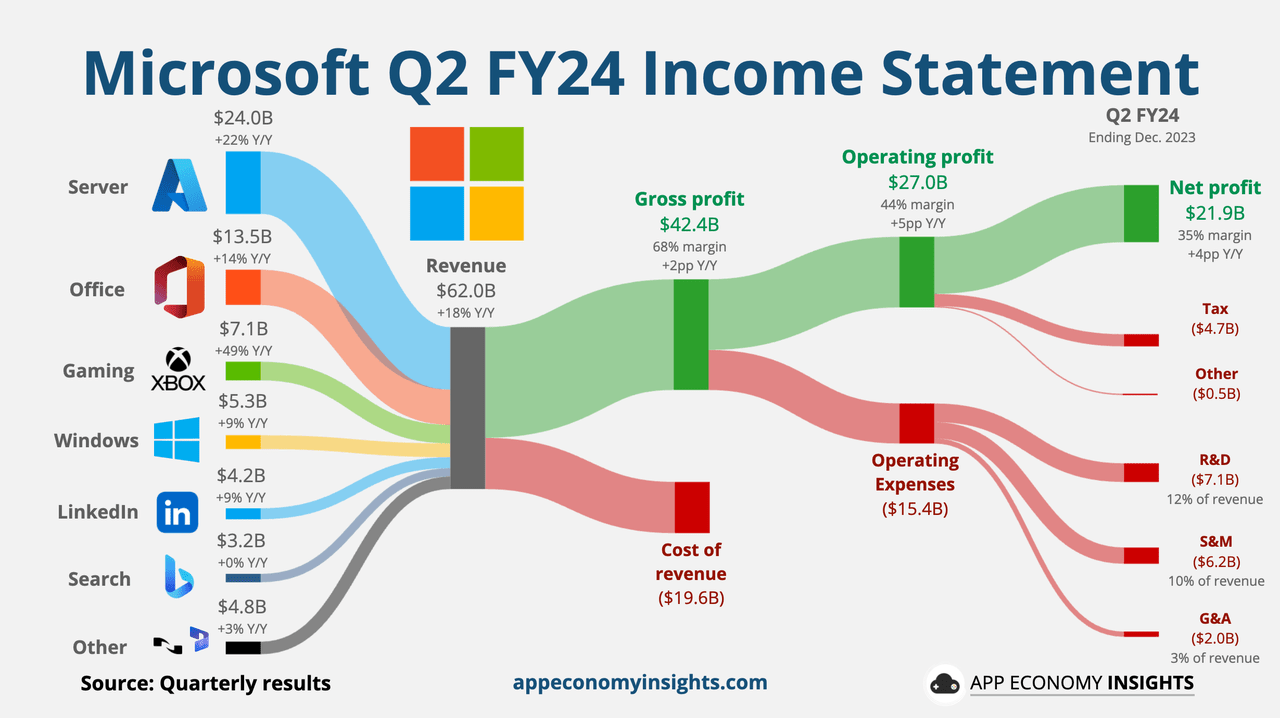

Azure cloud computing

MSFT is already rolling out AI features as a service on its Azure cloud computing platform, which is already one of Microsoft’s biggest revenue generators, dwarfing the next biggest generator, its Office software.

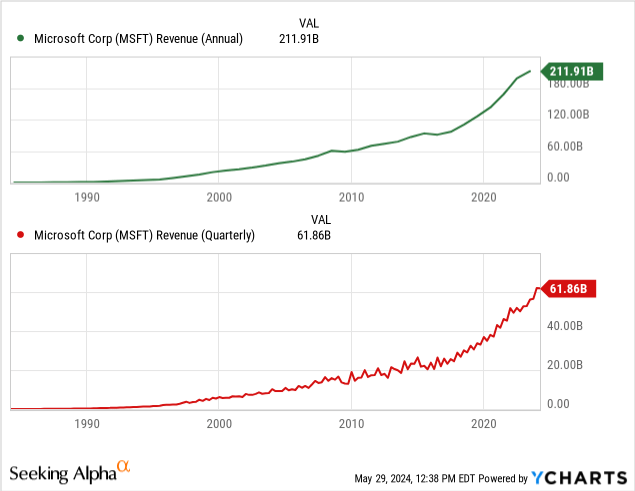

Figure 1 (App Economy Insights)

The introduction of data and cloud services via Azure, which was launched in 2010, changed the revenue trend for MSFT. Look at how the pre-2010 trend was much flatter than the post-2010 trend, both in quarterly and annual revenue numbers.

This jump is not a coincidence. Fueled by Azure, MSFT continues to make money with its cloud computing services.

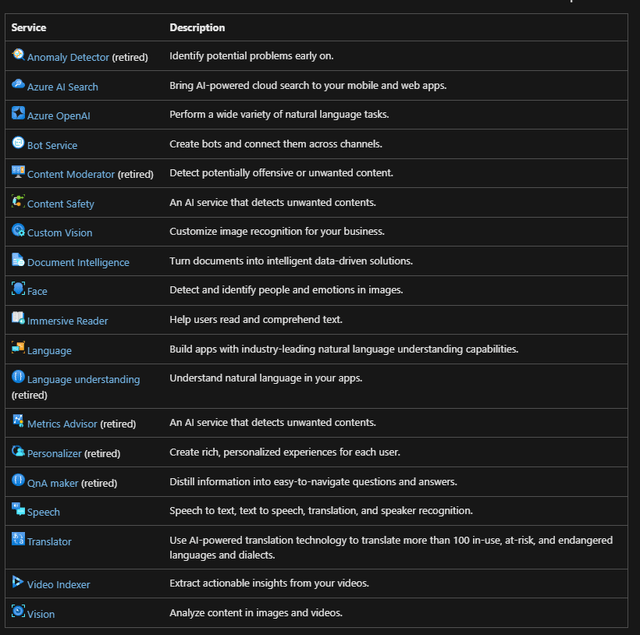

MSFT’s AI offerings are primarily concentrated in its cloud offerings. They offered several AI services that are now defunct, which are marked in the list below as “retired.” These services are intended to attract new customers who see these tools as beneficial to their business or workflow, and to entice Amazon Web Services (“AWS”) and Google Cloud Platform (“GCP”) customers to switch.

Figure 2 (Microsoft Corporation)

Since Azure makes up a significant portion of MSFT’s revenue, it is essential for them to continue bringing in customers to support the growth they expect from the market.

I think MSFT will have no problem bringing in these new clients. They are already making strategic investments all over the world to create new customers for their products.

Strategic investments

Microsoft made big news when it acquired a chunk of OpenAI in 2019, starting for $1 billion. Since then, its investments have increased to more than $13 billion. OpenAI produces the prolific ChatGPT and Dall-E AI platforms, which are the most popular generative AI platforms on the market today.

Hoping to reach developing and emerging markets with Azure, to capture the wave of companies from Asia and the Middle East moving to Web 2.0 as their economies evolve and digitize, MSFT has made several very large investments in cloud computing and artificial intelligence recently. few months.

Geographical investments around the world

All of these newsletters from MSFT itself are from the last couple of months.

- $2.9 billion in Japan to open a research center in Tokyo and train more than 3 million people

- $1.5 billion in the UAE for a stake in artificial intelligence and infrastructure company G42

- $1.7 billion in Indonesia for infrastructure and training of more than 800,000 people

- $2.2 billion in Malaysia for infrastructure and training of more than 200,000 people

- $3.3 billion in Wisconsin, USA to build a manufacturing-focused AI research lab on the University of Wisconsin-Milwaukee campus, build infrastructure, and train more than 100,000 people

MSFT Venture Capital Fund, M12

In addition to these investments, Microsoft is taking positions in several private AI companies via its M12 venture capital fund.

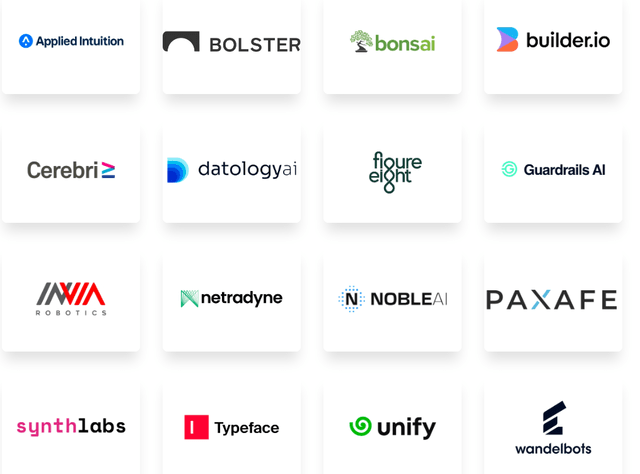

Below is a list of major stakes they have acquired in AI-focused companies, via their website. There you can also find their cloud infrastructure and other investment focus areas on this site. The list is extensive and I encourage you to take a look at the familiar names.

Figure 3 (Microsoft Corporation)

In total, M12 currently has 292 total investments, of which it leads 86. Of these investments, 16 are AI-focused, and this only includes the funding rounds in which M12 participated. MSFT also has its own acquisitions and investments in this area.

Hunting Mustafa Suleiman

There are a few names in the world of artificial intelligence that are widely known. OpenAI’s Sam Altman is probably the only AI developer more famous than Mustafa Suleiman, who was a co-founder of DeepMind Technologies. Google acquired DeepMind in 2014, four years after its launch, and it became the backbone of Google’s AI division.

Solomon left Google in 2022 and created his own company with Linked-In co-founder Reed Hoffman, Inflection AI.

Microsoft did not acquire Inflection AI, likely to avoid further regulatory scrutiny, but instead poached Solomon and a significant portion of the Inflection AI staff. Suleiman is now Head of AI at Microsoft, leading the entire AI division. They also purchased a $650 million stake in Inflection AI through its venture capital wing.

Hiring Suleiman and forming a new division at Microsoft for him and his team, along with the divisions that manage the search and browser programs, shows how important this acquisition is to Microsoft and what a boon they see for themselves.

Artificial intelligence on a large scale

One of the things that struck me most from Microsoft’s last earnings call was when CEO Satya Nadella said this in his prepared remarks:

We have moved from talking about AI to implementing AI at scale.

Microsoft sees itself as a leader in this field, and this note is proof of that. Satya rarely promises what he cannot deliver, and has advocated controlling AI for safety.

Scaling is also one of the most important aspects for Microsoft to achieve success in deploying AI. We know that training and running new models can cost hundreds of millions of dollars, so making a mistake can be a very costly mistake.

Google’s costly mistake is hitting them right now, as its search overview AI technology delivers hallucinatory and misleading results, and produces dangerous information. This caused a public uproar and gave Google a bad look.

Fair value

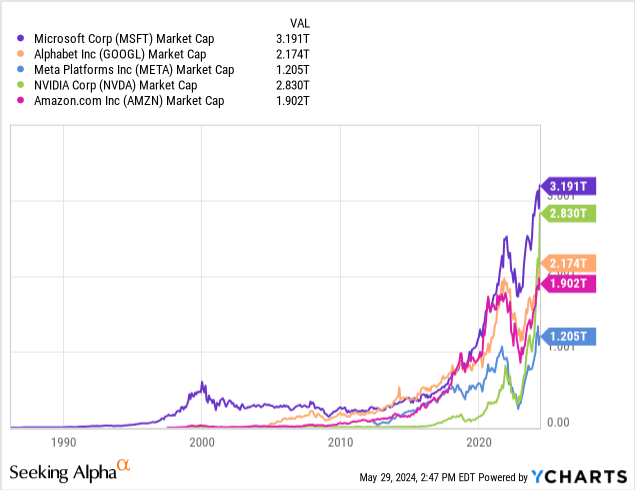

How will artificial intelligence affect Microsoft’s value? MSFT is currently the most valuable company in the world, worth approximately $3.2 trillion. This is a tremendous accomplishment, but I see more in MSFT’s future.

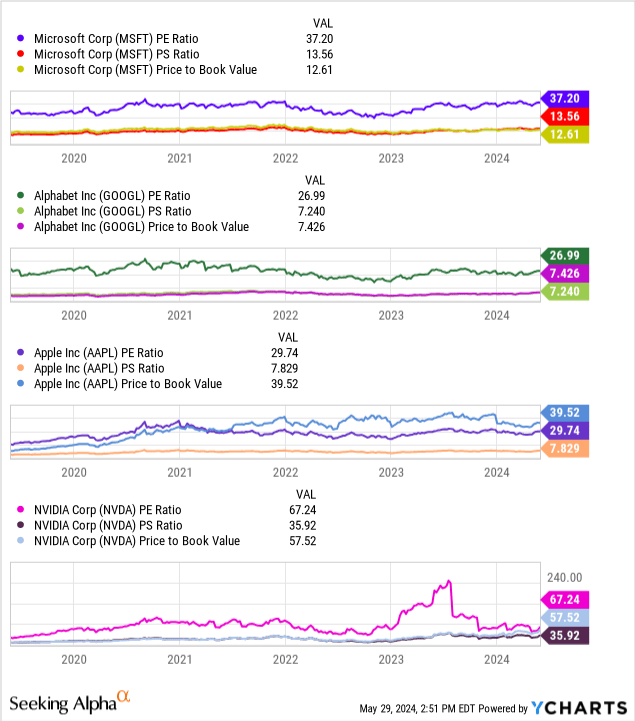

It trades at around 37 P/E, 14/13 P/E, which is higher than Google and Apple (excluding Apple’s P/E), but lower than NVIDIA. Its fundamental ratios are worth more than the S&P 500 average, but that’s because Microsoft’s growth trajectory has become steeper. I believe the integration of AI and new tools into MSFT will achieve these growth goals.

It is unclear how high MSFT could go, as we are now in newly charted territory for valuations. US valuations have never been higher than they are today, and MSFT already has the highest valuation of any company in the world, but that doesn’t mean we’ve reached the ceiling.

Based on the metrics reviewed in the financials section, I believe we are not there yet. There is still room for MSFT to add new sources and build on existing revenue streams in emerging and developing markets, by taking market share from AWS and GCP, and with new technical breakthroughs in AI through the new AI division.

Risks

There are some major risks to this thesis, primarily:

- MSFT’s AI division could fail, despite all the major acquisitions and talent hunting. Good people and companies do not guarantee that they will innovate or accelerate their revenue through these services.

- Google, Apple, Meta, NVDA, or any other large company investing in AI might be able to outperform MSFT, which is not the leader in R&D spending among major companies (in fact, Amazon is).

- Generative AI may have peaked, something I wrote about recently.

- Breakthroughs in AI research, fueled by spending and acquisitions, can lead to very small gains that do not produce enough ROI to make further investment worthwhile.

- Technological progress can be squandered by bad products, like Windows Phone.

- A big market correction could hurt MSFT more than some other big tech, because its valuation is richer than that of some of its peers like Apple and Google, and it is expected to decline before it reaches “value” territory.

Conclusion

Microsoft is set to win the AI war, as its deployment has been generally well-received compared to recent AI mishaps in Google Search. MSFT’s increasing growth is due not only to its poaching of key employees such as its new head of AI, Mustafa Suleiman, but also to its strategic partnerships abroad, and its acquisition and investment in several AI companies around the world.

Winning the AI war (i.e. having the best AI systems) will set up Microsoft for the dominant technology stack associated with its cloud computing service, Azure. MSFT gets a significant portion of its revenue from Azure and the increase in platform customers translates directly into revenue and profits for Microsoft.

I’m issuing a “buy” rating on Microsoft and considering it for a position in my stock portfolio as a standalone stock, but would limit my exposure to no more than 5% of my portfolio to individual stocks.

Thanks for reading.