Da cook

Written by Tracy Chen, CFA, CAIA

The ancient tale of the silly old man who moved the mountains that blocked his doorsteps has become a beloved legend in China. It serves as a reminder that with perseverance, even the most difficult obstacles can prevail can be overcome. China recently announced a real estate rescue package aimed at absorbing unsold inventories. Will China’s perseverance finally succeed in pushing its beleaguered real estate sector towards recovery?

why now?

China’s post-Covid-19 recovery has been plagued by deflationary pressures and short-term expectations. The real estate market remains the main drag, due to years of severe credit tightening on the supply side and purchasing restrictions on the demand side. Since early 2022, we have seen purchasing restrictions gradually eased, but to no avail. Recent economic data highlights an unbalanced two-track economy:

- On the one hand, industrial production, manufacturing capital expenditures, and exports China continues to perform well, thanks to inventory restocking, industrial policy focused on the “new three” of electric cars, solar panels, lithium batteries, and strong external demand.

- On the other hand, consumption and the real estate market continue to deteriorate. The collapses in housing investment, sales and prices have not abated (see Figure 1).

China has chosen to shift credit away from the real estate market to focus on industrial development. The intention was that gains in industrial production and manufacturing would offset property problems. However, this strategy faces multiple problems. The “new three” are already suffering from excess capacity (see Figure 2), low prices, and backlash from export destinations. For example, US President Biden launched targeted tariffs on $18 billion worth of Chinese imports. If eurozone countries follow suit, the damage will be much greater, because the EU accounts for a larger share of China’s exports. Furthermore, these new tariffs and rising geopolitical tensions may lead to more supply chain relocations outside of China.

Meanwhile, the default of Evergrande and Country Garden, along with the dire financial situation of Funke, a strategically important real estate developer, has policymakers worried. Other factors, including moderation in capital expenditures on infrastructure, a sharp slowdown in government bond issuance in the first quarter, and a weak credit impulse, made it necessary for China to focus more on domestic demand and get its internal affairs in order. It is against this background that the new real estate stimulus package was designed. It was a strong announcement, indicating that stabilizing the real estate sector has become an urgent priority.

Package

China’s real estate rescue package focuses more on risk management than on engineering another real estate boom. It aims to achieve multiple goals, including boosting housing demand, reducing housing stock, and supporting developers:

- Land buyback: Local governments may buy back excess land from developers at “affordable” prices. The land could be used to build affordable rental housing. Financing may come from private bond issues, but local governments may have low incentive to purchase land amid difficult financial conditions.

- Stock reduction: Local governments may purchase surplus housing stock from developers at “affordable prices” through local state-owned enterprises. The properties are then converted into affordable rental housing. The bank loan volume reaches CNY 500 billion with a re-lending facility from the People’s Bank of China of CNY 300 billion at an interest rate of 1.75% for a maximum period of 5 years.

- Financing unfinished projects: Banks are encouraged to meet reasonable borrowing needs for whitelisted real estate development projects.

- Requirements for soft housing loans: The minimum down payment is reduced by another 5 percentage points to 15% for first homes and 25% for second homes, a historic low. Minimum mortgage interest rate restrictions were removed, although many cities were not already subject to this restriction. The interest rate on Personal Provident Fund loans for housing has been reduced by 25 basis points.

Challenges and uncertainties

Although this package is welcome, it may not directly boost sales or investment. Housing inventory is at its highest levels in several years. The success of the rescue plan depends on size, financing and implementation:

-

- size: According to Barclays research, to reduce the average number of months of unsold inventory to 18 months of sales, which is considered the normal inventory level, from the current 33 months, the government would need to purchase CNY 14.6 trillion of housing stock, assuming that annual home sales New revenues worth CNY 11.7 trillion in 2023 (see Figure 3). Assuming a 50% discount, this estimate equates to a government purchase of CNY7.3 trillion (US$1 trillion). The planned CNY500 billion financing appears very small, representing only about 3% of the stock.1

- Pricing: The goal of purchasing housing stock is to stop the downward spiral of real estate prices. However, it is difficult to determine the “right” purchase price to ensure fairness. There is a risk of wealth destruction for some parties. If this proposal is priced at a significant discount, it may discourage developers from selling or encourage households to trade it up. The price decline may spread to other properties, resulting in a contagion effect.

- Local government participation: Local governments, already facing financial and debt difficulties, may be reluctant to participate due to low rental yields versus financing costs. In addition, the program is non-binding. Since lenders and borrowers are responsible for future risks and bad debts, risk aversion may limit uptake. According to Rhodium Research, a similar pilot purchasing program launched in early 2023 with a CNY100 billion stake was met with very little interest, with only CNY2 billion taken up.2

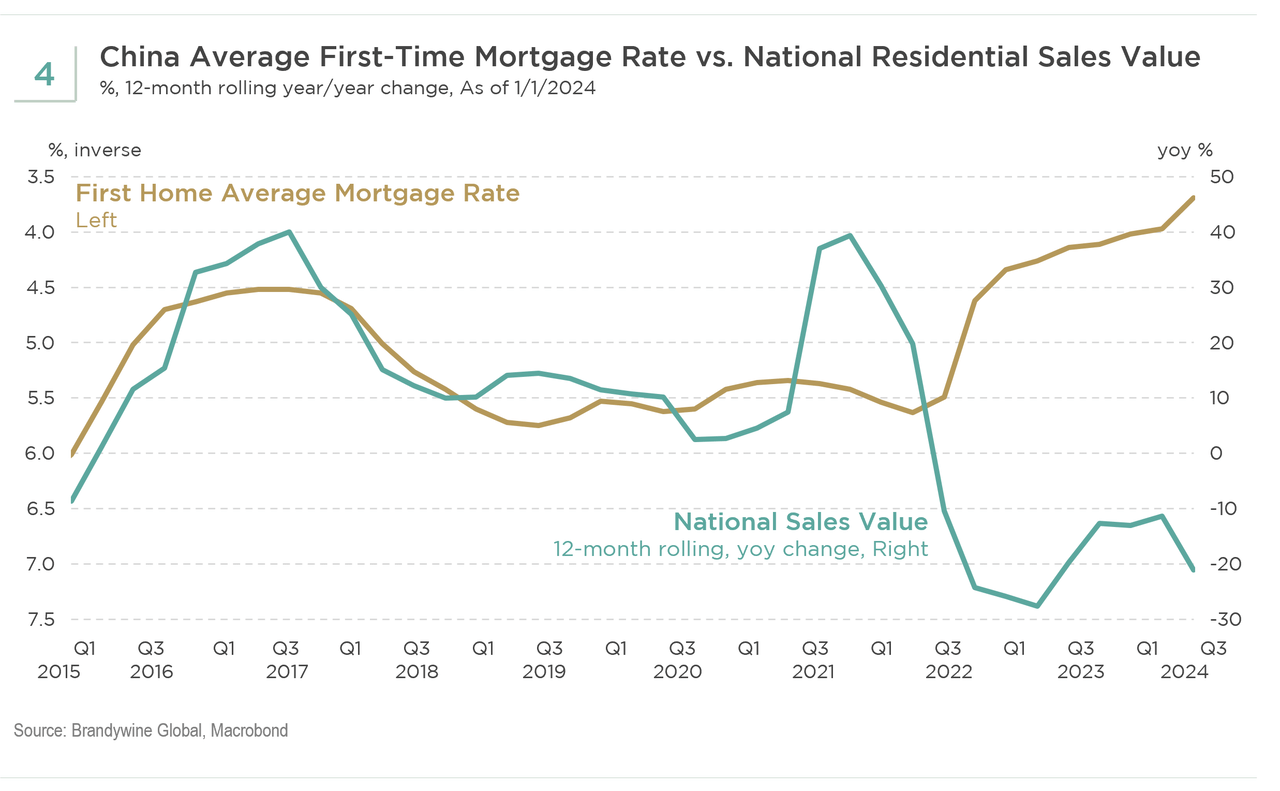

- Buyer Trust: Trust is key, as the success of the program depends on people’s desire to buy homes. Aside from promotions or life event needs, families have mostly lost interest in purchasing homes (see Figure 4). With a large surplus in supply, expectations of rising housing prices are declining, and homes may no longer be viewed as a store of value (see Figure 5).

- Moral hazard: Government interference in real estate purchases raises concerns about moral hazard, corruption, rent-seeking, and unfair competition.

- effectiveness: Previous political stimulus, which has generally produced short-term market head shams, highlights the challenge of addressing long-term structural issues in the market.

Conclusion and investment implications

China’s weak recovery from the pandemic and ongoing issues in the real estate sector have put continued pressure on Chinese assets and the currency:

-

- The yuan (CNY) continues to face downward pressure against the US dollar (USD), due to wide interest rate differentials, rising geopolitical tensions, and a potential delay of Fed rate cuts. In order to avoid capital outflow, which has accelerated recently, and attract foreign direct investment, the People’s Bank of China seeks a fixed fixation of the Chinese yuan to maintain a stable currency (see Figure 6). However, this practice is likely not sustainable in the face of any sudden shocks. We believe that the path of least resistance for the Chinese Yuan and the gradual depreciation of the US dollar has been measured. If the US dollar weakens, the Chinese yuan tends to underperform as other currencies rise.

-

- The rise in Chinese government bonds may stall and consolidate in the short term with the market giving rescue measures the benefit of the doubt. The People’s Bank of China (PBOC) aims to keep nominal interest rates low with potential rate cuts. We expect the increased bond supply to be accompanied by liquidity injections and potential purchases from the People’s Bank of China. Banks and insurance companies, suffering from a shortage of safe assets, are buying Turkish central bank bonds, which still look attractive due to the high real yield compared to their counterparts (see Figure 7) and the high foreign currency-hedged yield. In contrast to the “higher for longer” story of US Treasury yields, Chinese central bank yields are likely to remain lower for longer, given structural deflationary pressures in China. We believe there is a better entry point if the 30-year CGB yield exceeds 2.65%.

The rescue package constitutes a step towards stabilizing the real estate market in China, but its success depends on overcoming major challenges and reviving families’ confidence in purchasing housing. However, the stimulus may fail again due to the scale of the supply problem. The size, financing and execution of inventory purchases is very small and unclear. Hence, the rescue package is not yet a game changer. Large amounts of unsold housing require strong and persistent policies. Policymakers must make significant efforts to revive homebuyer confidence. Absent further intervention, the scale of the real estate supply problem likely means that China’s real estate sector will be a drag on growth for years to come.

1 Barclays Research, “The devil is in the details,” May 16, 2024

2 Rhodium Group, “Comments from Rhodium on Stimulating New Real Estate Sector in China,” May 17, 2024

Original post

Editor’s note: The summary points for this article were selected by Seeking Alpha editors.