com. grandriver

Nabors (New York Stock Exchange: NPR) Financial performance has stabilized in recent quarters, but the stock remains under pressure due to a slowing macro environment and the potential end of OPEC supply cuts. This presents a problem for Nabors because it has some A risky balance sheet that will likely find it difficult to weather an extended downturn.

I have previously suggested that Nabors’ profitability should improve if the number of rigs in the United States stabilizes and international activity continues to rise. This has not been the case so far, as Nabors’ earnings have declined and the stock is down nearly 12%. I am now more pessimistic about Nabors’ prospects, given the physical threats to oil and gas prices.

Market conditions

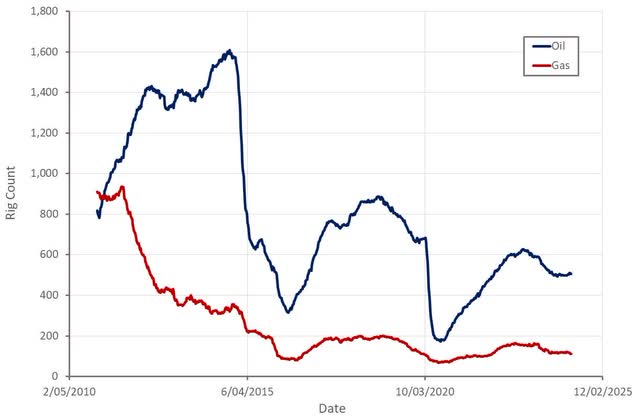

While the industry’s rig count was fairly flat in the first quarter, Nabors’ rig count expanded modestly, despite the company choosing to prioritize pricing over usage. poll From the lowest 48 clients indicate that The number of rigs will decrease slightly In 2024, which appears to be related to merger activity. Mergers aside, customers remain cautious, especially in gas basins. With the recent decline in oil prices, it is possible that the number of drilling rigs will decrease more than expected.

Figure 1: Number of US drilling rigs (Source: Created by author using data from Baker Hughes)

International activity remains strong, with Nabors reporting that it has been more than a decade since it has seen such a strong demand environment based on tenders and rig award negotiations. Nabors had 80 international rigs at the end of 2023, which could expand to 89 by the end of 2024 and 101 by the end of 2025. The company currently expects to deploy 5 rigs in Saudi Arabia in 2025 and one rig in Argentina, with the possibility of adding three rigs. Additional in the Middle East.

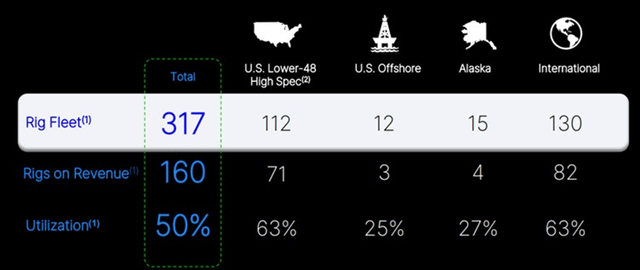

Figure 2: Nabors Platform Usage and Availability – March 2024 (Source: Nabors)

However, the future path will depend largely on OPEC and economic conditions. OPEC’s willingness to maintain supply cuts is likely to depend on oil demand. If macro conditions continue to deteriorate, I would not be surprised to see supply cuts continue, or even increase.

Nabors Business Updates

Nabors is currently focused on achieving growth in the following areas:

- international

- High specification fleet in the United States

- Nabors Drilling Solutions

- Carbon reduction solutions

- Automation and robotics

Nabors’ average rig count rose by 4 rigs in the first quarter, as international gains offset weakness in the United States. Nabors had hoped for increased Lower 48 activity in the first quarter but was disappointed. Despite this, prices for high-performance excavators remained stable. I have low expectations for Lower 48 drilling activity even though productivity gains continue to weigh on demand. This is a negative for drillers as daily rates do not reflect productivity gains.

Nabors deployed two platforms in Algeria in the first quarter and another in the second quarter. The company has also successfully negotiated the acquisition of three more platforms in Argentina, two of which are expected to come online in 2024. All three of these contracts are long-term contracts at favorable prices. Idle drilling rigs in the United States will be transported to Argentina for this work. Nabors has also been shortlisted for three drilling rigs in the Middle East (possibly Kuwait) and believes there are additional opportunities in Mexico and elsewhere in the Eastern Hemisphere.

Regarding Saudi Arabia, sentiment has been weak recently after the kingdom announced that it would not expand its oil production capacity. This appears to be targeting offshore activity and should not have a material impact on Nabors, as it is more vulnerable to onshore gas exploration. Aramco remains focused on developing natural gas resources, and unconventional resources in particular. Sanad has obtained 15 platforms so far. Nabors’ sixth new construction platform in Saudi Arabia is expected to begin drilling soon. Two more platforms will be deployed in 2024, another 5 platforms in 2025 and 2 platforms in 2026. It is expected that 50 platforms will be deployed over 10 years.

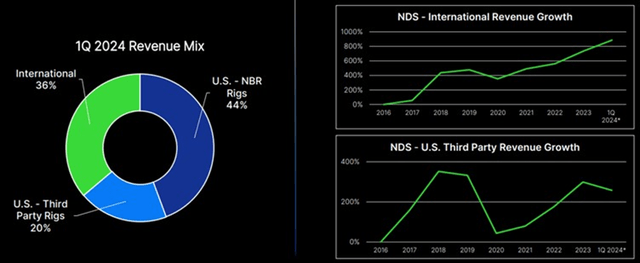

While NDS revenues from third-party platforms in the Lower 48 were under pressure, NDS revenues internationally and from Nabors platforms in the Lower 48 increased in the first quarter. This is important given the relatively high margin nature of this part of the business. Managed pressure drilling and RigCLOUD led Q1 performance.

Figure 3: National Development Plan revenues for the first quarter of 2024 (Source: Nabors)

financial analysis

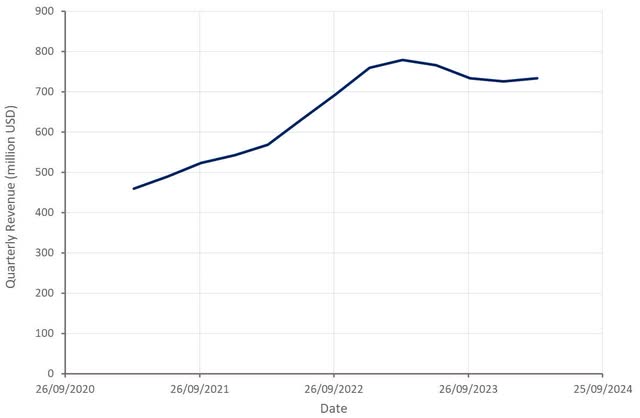

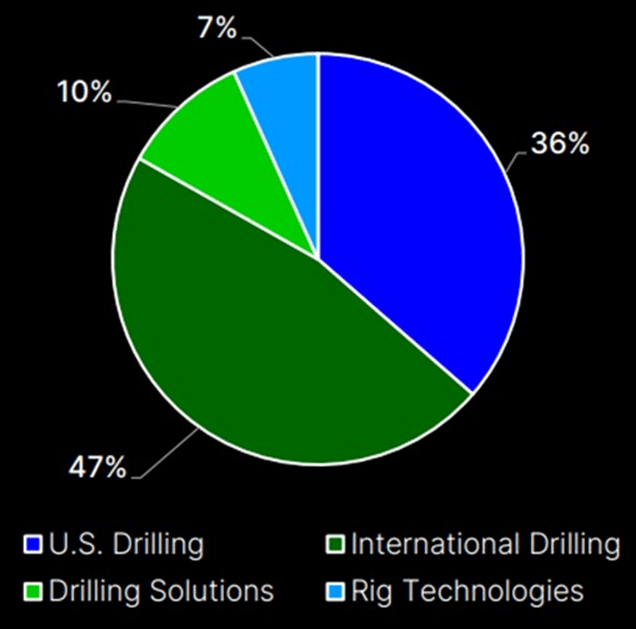

Nabors generated revenue of $734 million in the first quarter, down approximately 6% year over year. U.S. drilling revenue increased 2.3% to $272 million, driven by additional activity in Alaska. International drilling revenue was $349 million, an increase of 1.9% sequentially. This increase was a result of the deployment of drilling rigs and operational improvements in Saudi Arabia. Nabors Drilling Solutions revenues decreased modestly as a result of decreased activity in the lower 48 U.S. market. Rig Technologies’ revenues declined approximately 15% sequentially, which Nabors attributed to seasonality.

Nabors’ revenue and profitability will likely be flat again in the second quarter. International activity continues to increase, but this will be offset somewhat by onshore activity in the US, driven by gas-focused drilling.

Figure 4: Nabors revenue (Source: Created by author using data from Nabors) Figure 5: Nabors Q1 2024 revenue by segment (Source: Nabors)

Adjusted EBITDA in the first quarter was $221 million, down 4% sequentially. The gains in Alaska were offset somewhat by lower daily margins in the lower 48 regions. Nabors’ Drilling Solutions and Drilling Technologies segments generated $39 million EBITDA in the first quarter.

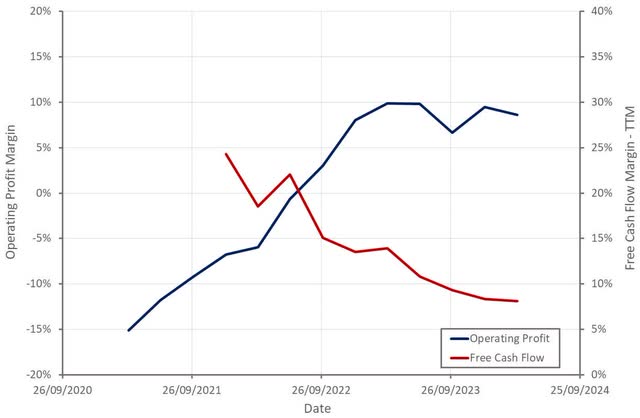

Figure 6: Nabors profitability (Source: Created by author using data from Nabors)

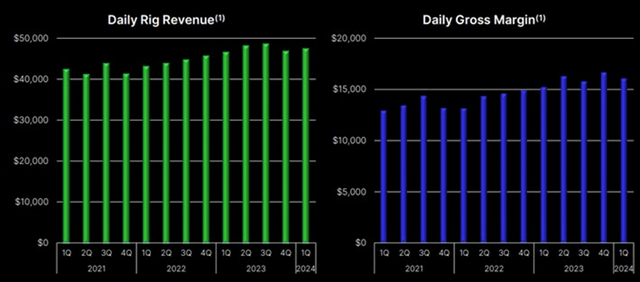

Nabors International’s daily margin declined slightly in the first quarter due to labor unrest in Colombia involving four platforms. The company expects international daily margins to move toward $17,000 over the course of the year.

Figure 7: International rig economics (Source: Nabors)

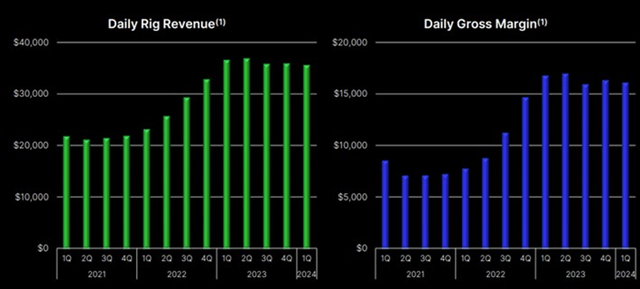

Low daily margins of $48 in the US have been fairly consistent in recent quarters, which Nabors believes has been helped by its position at the higher end of the market. Nabors’ minimum daily drilling margin of 48 does not include NDS.

Figure 8: Economics of the Lower 48 Drilling Rig (Source: Nabors)

Nabor’s free cash flow now appears to be stabilizing, albeit at a low level. Much of this was driven by higher CapEx. Free cash flow was slightly above break-even in the first quarter, even though the first quarter had the largest cash outflows. Outside of the bond, Nabors expects to generate approximately $160-260 million of free cash flow in 2024. While this is large compared to the company’s market capitalization of approximately $600 million, it is dwarfed by the company’s debt position of $2.5 billion American.

Nabors recently redeemed its bonds maturing in 2024 and 2025 using proceeds from bonds issued at the end of 2023. Nabors will continue to direct free cash flow toward reducing net debt and improving its credit rating. While Nabors has been able to reduce its debt load in recent years, the company’s position is still somewhat precarious, as interest expenses continue to eat up much of the company’s earnings and cash flow. Nabors really needs strong market conditions to continue for some time so that debt can be reduced to more sustainable levels.

Conclusion

Nabors stock has faced difficulties in recent weeks on the back of weak economic data and the potential end of OPEC supply cuts. The cancellation of plans to expand oil production capacity in Saudi Arabia likely also contributed to negative sentiment. However, Nabors may not be affected by the cancellation of production capacity expansion plans in Saudi Arabia as the market expects. The company’s exposure is primarily to onshore gas, and growth is expected to come from unconventional sources.

While Nabors stock may ultimately prove relatively inexpensive, risks remain high due to the company’s weak balance sheet. If oil and gas prices continue to decline and drilling activities are affected, Nabors could soon find itself facing significant losses. Although I believe this scenario is now increasingly likely, some international activities may be relatively insensitive to the macro environment.

Figure 9: Nabors’ EV/S ratio (Source: Seeking Alpha)