Bill Deodato

Some of my favorite companies on the market are ones that most people don’t know about. One good example of this is Presto national industries (New York Stock Exchange: NBK), an old but young conglomerate with diverse operations Which consists not only of defense products and safety products, but also the housewares/small appliances unit. But just because I like a company, doesn’t mean I’m going to rate it bullishly. In January of this year, for example, I decided to do just that reconsidering business in order to see if there is any upside potential.

With the mixed financial performance and how the shares were priced, the end result was my decision to keep the company with a “hold” rating. This type of rating indicates my belief that stocks should generate fairly consistent performance With the broader market for the foreseeable future. However, what actually happened was less optimistic than this. While the S&P 500 has risen 11.8% since then, shares of National Presto Industries are up just 2.9%. As much as I would like to upgrade the company now, I actually think this poor performance was justified. Revenues, profits and cash flows declined year over year. This came on the heels of a fairly strong fiscal year for 2023 compared to the year before. Add to that the fact that the house’s stock is still priced, I don’t think I can justify anything higher than the rating I currently have.

Short term pain, long term gain

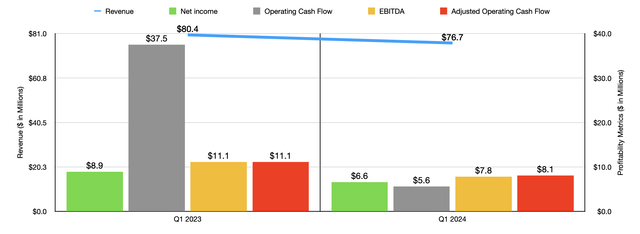

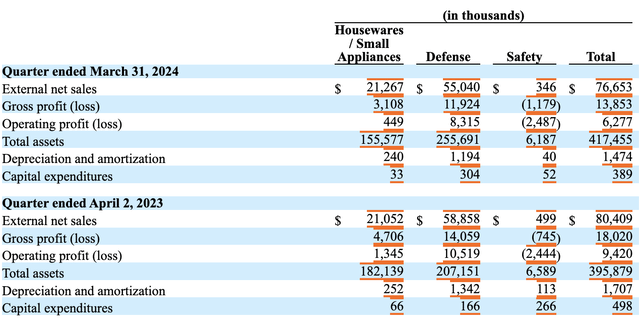

When it comes to National Presto Industries’ underlying performance, it’s best to start with the first quarter of fiscal 2024. This is the last quarter for which the company has data. I think it’s also the quarter that led to the stock’s weakness. For example, revenue was $76.7 million. This is 4.6% lower than the $80.4 million reported just one year ago. Two of the three operating segments experienced weakness leading to this decline. The smallest is the Safety segment, which consists of subsidiaries known as OneEvent Technologies and Really Innovations. Its operations include, but are not limited to, the cloud learning and analytics engine that uses sensors to control sensors that can sense things like temperature, carbon monoxide, and more. This segment’s revenues decreased from $0.50 million to $0.35 million.

Author – SEC EDGAR data

Much more important is the defense sector which includes a wide range of operations such as those involving the production of 40mm ammunition for the Ministry of Defence, the production and sale of ammunition and ammunition related products to the same customer, the production of cartridge cases that are used in medium caliber ammunition, the production of facility detonators, Booster pellets, firing cartridges, and more. This segment saw revenues drop from $58.9 million to just $55 million. This fall, according to management, came about due to lower shipments from the company’s backlog. I really wish we had more data than that. But unfortunately, the management is very vague. Meanwhile, the only sector that saw growth was the household appliances/small appliances segment. Revenue rose modestly from $21.1 million to just under $21.3 million.

Presto national industries

As revenues declined, profitability also took a hit. Net income fell from $8.9 million to $6.6 million. In addition to seeing the Safety segment post a slightly wider operating loss year over year, the company also saw very significant weakness in the other two segments. For example, the defense company saw operating profits decline from $10.5 million to $8.3 million. Management attributed this to achieving a total profit of $2.1 million for this segment due to lower revenues and an unfavorable change in the product mix. However, the Housewares/Small Appliances segment took a hit, with operating profits falling from $1.3 million to just $0.45 million. Management attributed this to a decrease in gross profit for this segment by $1.6 million, as changes in the product mix, not to mention higher repair costs at the company’s main facility, negatively affected profitability.

Author – SEC EDGAR data

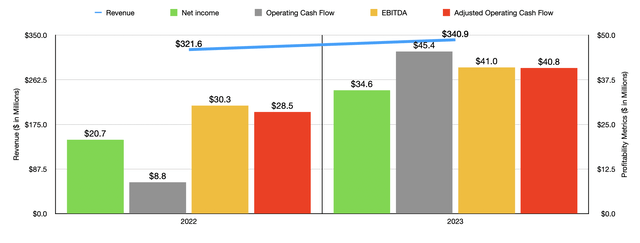

Meanwhile, other profitability metrics took a hit as well. Operating cash flow decreased from $37.5 million to $5.6 million. Even if we adjust for changes in working capital, we get a decrease from $11.1 million to only $8.1 million. Finally, the company’s EBITDA fell from $11.1 million to $7.8 million. All of this represents a dramatic turnaround from the way 2023 ended compared to 2022. As the chart above shows, revenues, profits, and cash flows all grew year-over-year.

Author – SEC EDGAR data

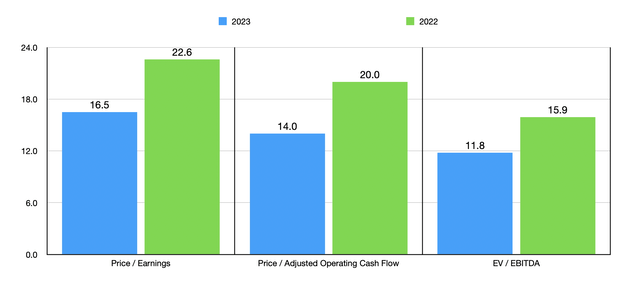

Using historical results for 2022 and 2023, I was able to easily value the company as shown in the chart above. The stock price has gotten cheaper from 2022 to 2023. Given what 2024 will look like, it might not be unreasonable to expect multiples to increase again. However, even if we give the company the benefit of the doubt, the shares probably look just a little cheap compared to similar companies. For example, on a price-to-earnings basis, as shown in the table below compared to five similar companies, three of the five companies I compared them to are trading cheaper than them. That number drops to two out of five on a price-to-operating cash flow basis. And when it comes to EV’s approach to EBITDA, National Presto Industries ended up being the cheapest of the bunch. The company has benefited greatly when it comes to this profitability metric by having no debt and enjoying $87.9 million in cash and cash equivalents. That’s quite a lot for a company with a market cap of $570.5 million as I write this.

| a company | Price/earnings | Price/operating cash flow | Value added/EBITDA |

| Presto national industries | 16.5 | 14.0 | 11.8 |

| Astronomy (ATRO) | 5.7 | 186.7 | 38.2 |

| Aircel (ASLE) | 130.6 | 17.8 | 80.1 |

| Intuitive Machines (LUNR) | 10.1 | 8.1 | 29.2 |

| Intisar Group (TGI) | 6.5 | 5.2 | 15.5 |

| Docomon (DCO) | 48.8 | 17.5 | 15.0 |

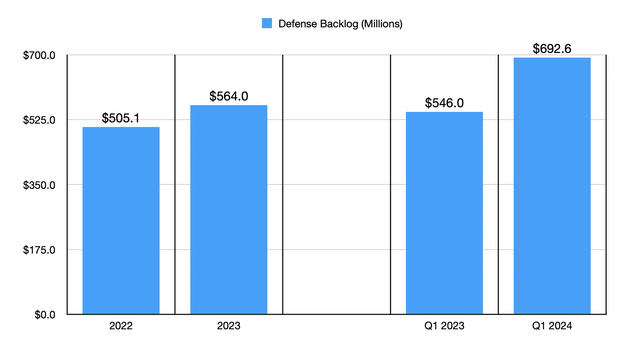

What helps keep me at a “hold” rating rather than downgrading the stock is the fact that the backlog continues to grow fairly significantly. When I say backlog, I’m specifically referring to the defense sector’s results. By the end of the first quarter of this year, the company had $692.7 million worth of backlog within this segment. This represents a massive 26.9% increase compared to the $546 million reported just one year ago. It’s also up well from the $564 million the company announced at the end of 2023. And it looks like this number will continue to grow. I say this because on May 14, management announced that the day before, National Presto Industries had been awarded another contract by the US Army. This is a five-year contract that could be worth up to $818.9 million. At the time the company announced this, it also announced that on May 10, another of its defense companies, Spectra Technologies, had received a follow-on subcontract to produce the optically tracked, radio-guided tube-launched warhead. Rocket 2B. The value of this contract is $48 million.

Author – SEC EDGAR data

He stays away

Although National Presto Industries seems stuck in a rut at the moment, the company is showing some strong leading indicators. Specifically, the value of the defense sector’s backlog is growing well. The company has a strong balance sheet and should perform well in the long term. But given how the stock is priced and the recent weakness we’ve seen, my best rating for the company is ‘hold’.