Hiroshi Watanabe

the Novin Churchill Direct Lending Company (New York Stock Exchange: NCDL) is one BDC that benefited from the prevailing tailwinds and went public this year (late January). While NCDL’s net asset base is quite large, compared to Morgan Stanley Direct Asian Development Bank lending (MSDL), another BDC that executed an IPO this year, is about 2x smaller in total size.

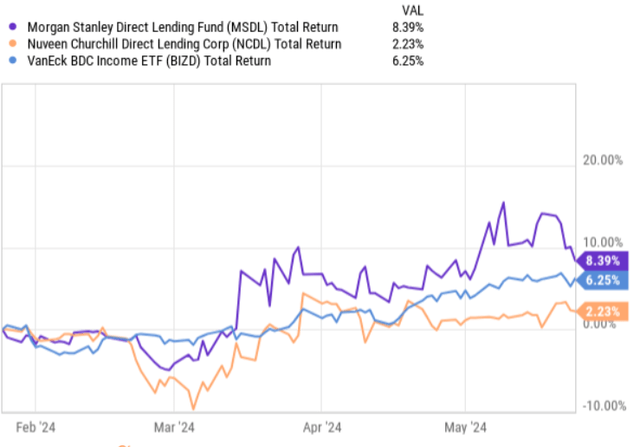

In April, I wrote an article on MSDL, assessing the underlying fundamentals to understand whether it is attractive enough to buy and compensate for the lack of a track record as a public company. The conclusion was positive and since then, MSDL has clearly outperformed the BDC index.

However, if we look at the chart below and compare NCDL’s total return performance to that of MSDL and the BDC index, we will notice that there is a very large gap Or negative alpha associated with NCDL.

YCharts

With this context in mind, let’s dig a little deeper into NCDL’s fundamentals to understand whether the combination of recent weak performance and financials justifies continuing to buy here.

thesis

NCDL’s focus is predominantly investing in senior secured loans of private equity-backed U.S. middle market companies. This is in line with the investment strategy of the majority of business development companies out there.

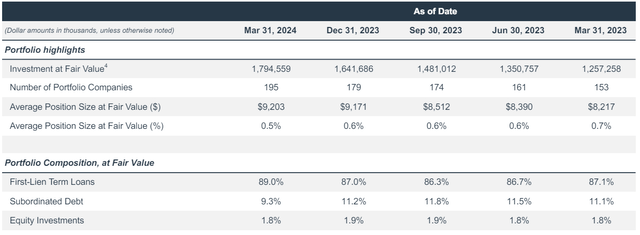

As we can see in the table below, the total value of NCDL’s portfolio is approximately $1.8 billion, with investments spread across 195 different companies, providing a good element of diversification. For example, the average position size as of Q1 2024 was 0.5% of portfolio value, something typically associated with large-scale BDC positions.

It is also worth highlighting NCDL’s focus on first lien structures, which currently take up 89% of the total exposure, with the remainder mostly placed in second lien or secondary investments (a small allocation is also directed towards equity investments).

NCDL Q1 2024 Earnings Presentation

The mix of first lien, subordinated loans and equity investments is within the parameters we would typically observe in the BDC space, where there is first lien dominance and more tactical allocations being made in riskier (higher return) sectors.

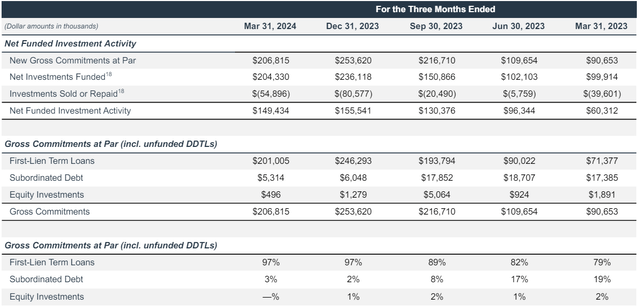

However, as the table below indicates, management has assumed a clear focus on increasing the first lien component to de-risk its portfolio. For example, in the past two quarters, most investments have been at the first lien level – about 97% of total net financing activity.

An additional point we can point out here is that NCDL has managed to keep its recent net investment funding levels positive despite the challenging backdrop in the capital markets and LBO space. Over the past two quarters, there have been more and more BDCs experiencing negative levels of net investment financing due to an inability to provide sufficient amounts to offset organic investment premiums. Such dynamics, by definition, impose headwinds on maintaining stable net investment income.

NCDL Q1 2024 Earnings Presentation

However, assessing the situation a little deeper, we can identify some signs that are not encouraging in terms of NCDL’s growth outlook and overall income predictability.

There are two specific aspects.

First, NCDL is currently experiencing notable pressure on spreads, as the annual portfolio income level has already declined for four consecutive quarters. Part of this is due to a general decline in the returns that business development companies can charge to investment firms (due to intensifying competition), and part of it stems from NCDL’s increasing focus on first-franchise products. For example, the direct spread NCDL obtained from financing activity for Q1 2024 was 4.9%, which is about 150 basis points lower than what it was able to obtain in early 2023.

s

NCDL Q1 2024 Earnings Presentation

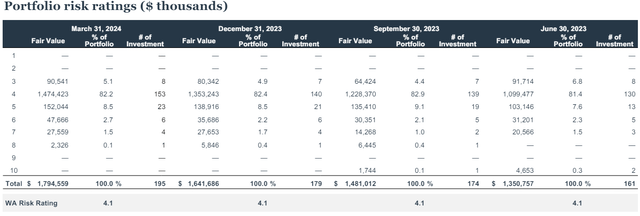

Second, the quality of the current portfolio is not great. As of now, NCDL’s portfolio-level weighted average risk rating is 4.1x, which identifies investments as in line with expectations. However, there is a relatively large portion of investments that fall under the “Rating 4” category, which already indicates that these specific investments or loans are not performing well and have high risk levels.

NCDL Q1 2024 Earnings Presentation

Currently, about $140 million is concentrated in the “Rating 5” category, where management has already sent notice to boards of directors to take concrete actions to stabilize financial performance.

Overall, the picture is not as rosy and solid as the underlying fundamental metrics might indicate. The combination of material spread pressure and subpar portfolio quality creates too much risk and speculation about NCDL’s continued growth prospects compared to the overall ability to absorb current earnings.

Bottom line

In my opinion, there is no strong enough evidence that would justify opening a long position in Nuveen Churchill Direct Lending Corporation.

On the surface, the fundamentals look strong as there is good diversification in place and the right focus on secure first franchise structures through already cash generating businesses.

However, the problem is that NCDL appears to be experiencing structural momentum in margin compression, making it difficult to maintain current net investment income levels. Furthermore, there are elevated risks to NCDL’s portfolio quality which could materialize in a negative (and amplified) manner under a scenario in which we see some economic weakness.

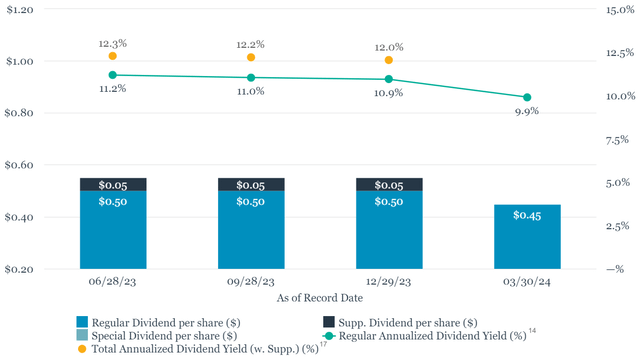

Given that NCDL offers a dividend yield of approximately 11.2% (which is slightly below the sector average), and given the above context, I see no logical reason why you should continue to buy NCDL.