NextEra Energy: Overvalued as Irrational Exuberance Returns (Rating Downgrade) (NYSE:NEE)

Justin Baggett

The utility and renewable energy industries have seen increased volatility recently, as rising interest rates and changing energy fuel prices pressure the electricity market. For the most part, we have seen demand for renewable energy slow as a result of the surge Capital investment costs. This change has negatively impacted major renewable energy companies such as NextEra Energy Partners, LP (Nip). This led to recalls from Dominion Energy (Dr) and others. The utilities sector, as seen in the Utilities Select Sector SPDR® ETF (XLUThe sector was the worst performer, leading the losses NextEra Energy Company (New york stock exchange: ny).

In 2021, it published a bearish forecast on NEE, citing overvaluation and anticipating slower growth. After losing 36% of its value by March of this year, I upgraded my view to neutral, believing NEE’s value was fair. Since last March, it has risen significantly By 40%. Thus, even though a little time has passed, I believe NEE’s phenomenal short-term performance warrants an outlook update.

NextEra Energy and the Future of Renewable Energy

The utilities sector has been the best performer over the past three months, returning nearly 15%. NextEra Energy is the largest holding in the utility ETF XLU at 14.7%, nearly double that of the second largest, The Southern Company (SO) at 8%. This stems from the valuation premium on NEE and its size.

NextEra Energy differs from other major utility giants because of its focus on renewable energy. However, I feel that there is often too much focus on marketing to investors regarding renewable energy, but not necessarily the realities of its business. For example, most of its energy comes from natural gas, 45% of the total. Nuclear energy represents 22%. Nearly 26% comes from wind, but only 6% from solar. So, in reality, its mix is not significantly different from its peers, especially as Duke, Dominion and others plan their own renewable energy projects. He is undoubtedly a leader, but he becomes less distinguished as time goes on. However, NextEra is focused on transition, with about 37% of NEER CapEx (renewable energy business – see 10-Q p. 33) going to solar and about 26% to wind.

I believe that this transformation will only happen if it is economically possible. Furthermore, investors should not expect to benefit from these investments unless this is true. In theory, the return on investment for renewables could be better than fossil fuels and nuclear power. Onshore wind has the lowest levelized cost of energy estimate, with a mid-range of $89 per MWh (including storage). The price of solar is $135 per megawatt hour (with storage). Nuclear power is priced at $182 per megawatt hour, while natural gas is the lowest at $76. However, solar and wind are more affordable if the storage issue is not taken into account, with onshore wind costing an absolute minimum of $27 per MWh without storage.

Of course, we can look at these data points in different ways. Across the board, the primary difference between fuel-generated power and renewables is the more significant storage needs of renewables and the higher labor needs of fuel-generated power. Coal and gas have relatively lower initial costs and high overhead expenses. Nuclear power has very high labor costs. Solar and wind have exceptionally high upfront costs but very low overhead labor costs. For this reason, high interest rates discourage renewable investments, leading to a disproportionate increase in capital financing costs. However, overall wage inflation benefits renewables, due to growing labor shortages in the traditional utility industry.

However, with today’s higher financing costs and lower natural gas prices, natural gas investments are likely to be more profitable than wind and solar. However, I believe the long-term ROI of wind and solar could still be superior due to the potential for continued rise in labor and commodity costs. As I noted in connection with NEE’s limited partnership, NextEra Energy Partners, rising solar and wind financing costs are offset by a roughly 50% decline in solar panel prices, caused by stagnant US demand and massive overproduction from China.

Therefore, I cannot argue that NextEra Energy is necessarily at a competitive disadvantage due to its heavy investment spending in solar and wind energy today. However, unlike many, I don’t think NEE necessarily has a competitive advantage either, as natural gas investments will likely have a better return, and this may remain the case for years to come, since natural gas is very cheap today, and its price is very low. Lower financing costs.

What is NextEra Energy worth today?

Given this, I don’t think NEE should trade at a premium to its peers, which also invest in wind and solar. Furthermore, the utilities sector should not trade at a large premium to bonds, given that they are income-oriented investments with minimal organic growth potential.

In addition, utilities, including NEE, are exposed to political risks amid allegations of misconduct regarding their former directors and ongoing backlash against Florida Power and Light’s (NEE’s subsidiary) electricity price hikes by state electricity regulators. Utilities earn a monopoly profit, determined largely by politicians’ willingness to let them raise prices. Recently, more utility regulators have opposed rate increases as voters have become concerned about rising electricity prices.

This problem has faded over the past year as electricity inflation has stagnated amid falling natural gas prices. However, it is likely to come back, given utility infrastructure investment needs caused by the aging of the power grid, exacerbated by rising labor and capital costs. In other words, almost all U.S. utilities need to invest more in their infrastructure investments, but they cannot do so without losing profits or increasing interest rates. Regulators, facing pressure from voters struggling with inflation, are not allowing interest rates to rise as was the case in the past. This has been a back-and-forth issue for NEE’s FPL, once again taking it to the state Supreme Court.

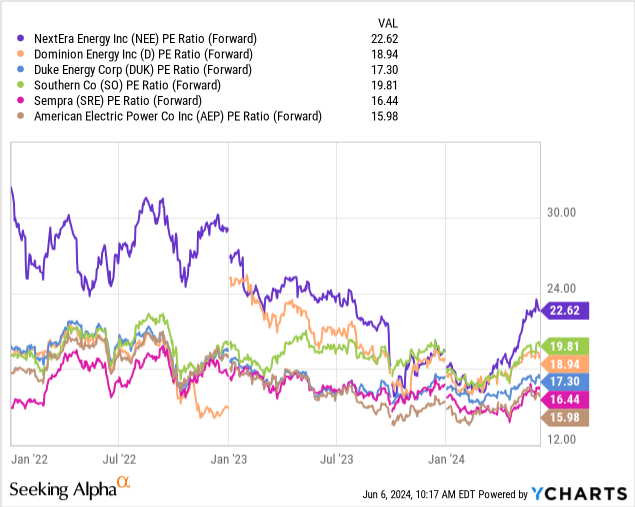

From a valuation perspective, NEE is much more expensive than its counterparts. Its forward P/E ratio is 22.6X, compared to its peer average of 17.3X, giving it a 30% premium. This premium was much lower when I published my neutral forecast for the company months ago, but it is much larger now. see below:

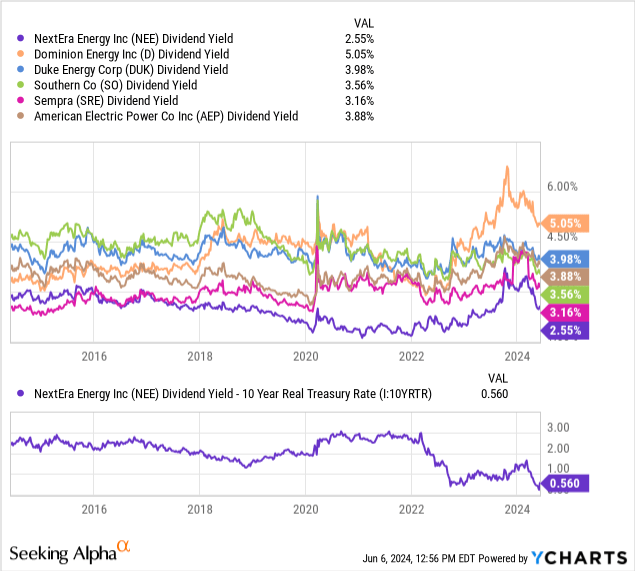

This premium is also realized in the dividend yield, which is just 2.55% compared to a peer average of 3.56%. NEE consistently has a lower yield than its peers, due to expectations of higher earnings growth. However, we must remember the possibility that renewables will not achieve the same return on investment as in past years or that their counterparts will continue to develop similar projects. Importantly, NEE’s dividend yield compared to real interest rates is very low, suggesting that it also has a high premium over bonds. see below:

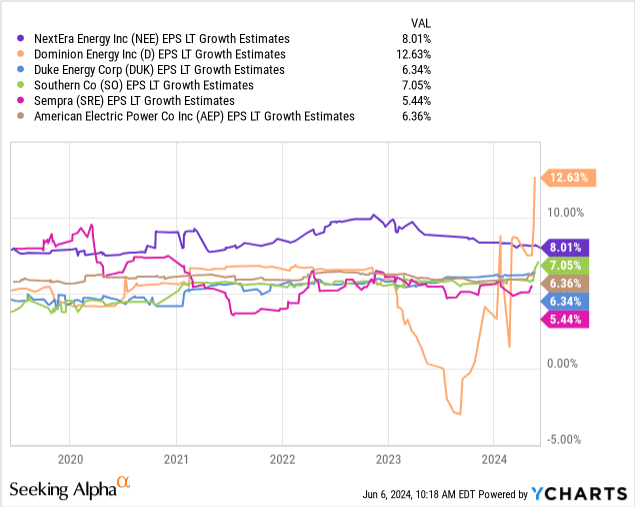

I compare utilities’ dividend yields to real interest rates, as both are likely to see their payments rise in proportion to inflation over time. Before 2022, there was a relatively flat premium among most utilities over real Treasury rates. However, with real interest rates rising, we have not seen a commensurate rise in utility dividend yields. I believe this is an indication that public utility prices are generally overvalued, especially when political pressures hamper their ability to raise their profits at the same pace as inflation. However, most analysts expect utilities to increase their income faster than inflation in the coming years. See EPS growth forecasts below:

This measure allows us to adjust P/E ratings based on growth expectations. Higher EPS growth allows for larger valuation multiples. For example, assuming that NextEra will actually grow EPS at a rate of 8.1% over the next three years, we can extrapolate an EPS level of 26.3% over three years. Therefore, the forward “earnings multiple” based on three-year expected EPS would be about 17.6X (or 22.6/1.263).

Using the same math, we get a three-year forward adjusted P/E of 16.1X for Southern (22.6% growth expected), 16.5X for AEP (20% growth), and 14.4X for Duke (20% growth). . 14X for Sempra (17% growth), and 13.2X for Dominion (43% growth). Thus, even adjusting for expected growth, NextEra has a ~19% premium to its peers, with a three-year average P/E growth estimate of ~14.8X.

Bottom line

Of course, we can look at a company’s relative valuation in different ways. However, if we compare it to real interest rates or its peers, NextEra appears to be overvalued today after its recent sharp rise. Simply put, utilities are “supposed” to be low-volatility investments. We might expect the bulk of the group to be remarkably quiet. However, abnormal fluctuations in the positive direction can quickly turn into the opposite direction. In my opinion, NEE has become overvalued due to the investor overexuberance surrounding it and renewables.

This does not mean that renewable energy is not the future, but investors should take into account its high capital costs and not assume that EPS growth will happen so quickly. In fact, given the state of the market, I doubt NEE will earn the 8% EPS growth rate that analysts are predicting. Furthermore, beyond that, I expect peers to see faster-than-expected EPS growth as they shift more aggressively toward capital investments in renewable energy today.

Overall, I think NEE is now materially overvalued and is best avoided. Although the LP, NEP, may carry more risk due to its business model, I am bullish on NEP and believe it is a much better investment in renewable energy from a risk-reward perspective. However, I am again bearish on NEE and will generally avoid major utility stocks because of their abnormally low premiums over Treasuries.