Thanks for your help

It’s difficult to paint the American consumer with a broad brush. There is growing evidence that low-income families are under increasing pressure while high-income families are doing just fine. The bearish trade effect is well underway, at least that’s a reasonable guess after a strong report From Ross stores (Roast) previously this month. foot locker (Florida) also scored well, saying consumers were willing to pay full price, while companies like LVMH Moët Hennessy – Louis Vuitton, Société Européenne (OTCPC:LMV) expressed concerns about the luxury market. Finally, DICK’S Sports Products (Dex) Shares rose after the first-quarter report earlier this week.

I am promotion Nike shares (New York Stock Exchange: NYSE). With the stock now trading near a 10-year low in its price-to-earnings ratio and with earnings stabilizing, the stock could stand out if its management executes well in the coming quarters. However, stocks should receive critical support Which I will detail later in the article.

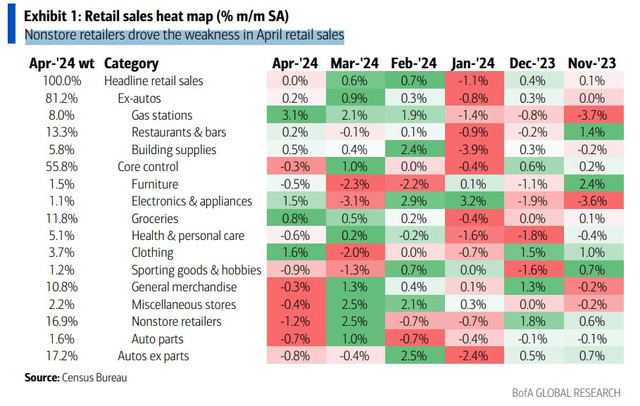

April soft retail sales report

Bank of America Global Research

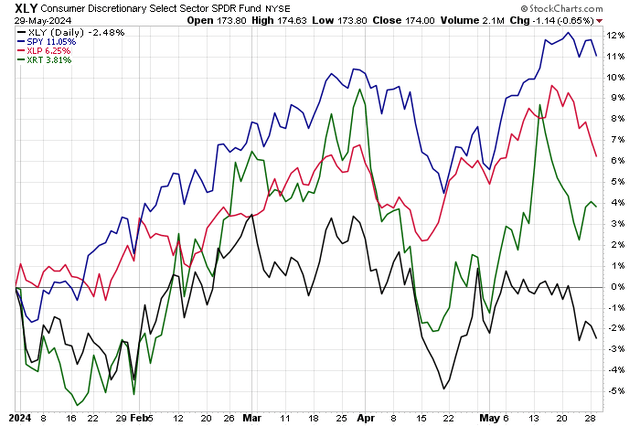

Consumer stocks decline in 2024, S&P 500 +11%

Stockcharts.com

Nike is the world’s leading sports footwear and apparel company with a market share of approximately 40% of the global sports footwear market. It also sells Jordan, Converse and Nike branded golf shoes and sports apparel. It is produced through independent contracts and overseas sources.

Nike to publish Mixed set of Q3 2024 results in March. Non-GAAP EPS of $0.98 It beat Wall Street expectations of $0.65 while quarterly revenue came in at $12.43 billion, up just 0.3% from year-ago levels, topping $130 million. NIKE Direct reported revenue of $5.4 billion, slightly better than estimates on a constant currency basis, while NIKE Brand Digital sales fell 4% on a foreign currency adjusted basis. The wholesale segment saw sales of $6.6 billion, an increase of 3% year over year. However, direct-to-consumer (DTC) product revenue declined in the quarter, with digital sales declining significantly. The bright spot was a 200 basis point improvement in gross margin, driven by full-price selling and lower product costs. China remains a sensitive point.

After a third straight EPS beat, shares initially rose, but then fell nearly 8% after the March earnings update, and options traders priced in a 5.6% earnings-related stock price swing when analyzing an in-the-money stretch that expires soon . After the reporting date of June 27. Nike issued a cautious outlook following its third-quarter report that reflected ongoing broad consumer challenges, particularly at the lower end. I see a lot of the consumer and China challenges now priced into this strong brand, but the upcoming Q4 report will be key. Risks include continued weakness in consumer spending, weak currency market trends (a stronger dollar), and further decline in China.

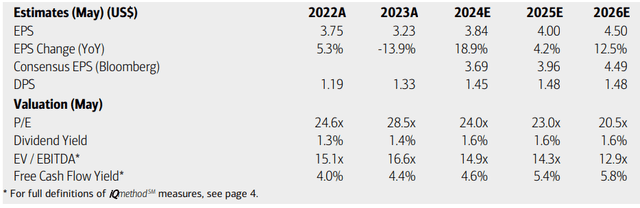

on evaluationAnalysts at Bank of America see profits up 19% this year with off-year EPS reaching $4. The bottom line is expected to accelerate by 2026. Seeking Alpha’s current consensus numbers show a stronger operating EPS number for fiscal 2024, but then slightly lower numbers in recent years. Nike’s top line is expected to rise 1-2% this year and next, with strong sales increases in 2026.

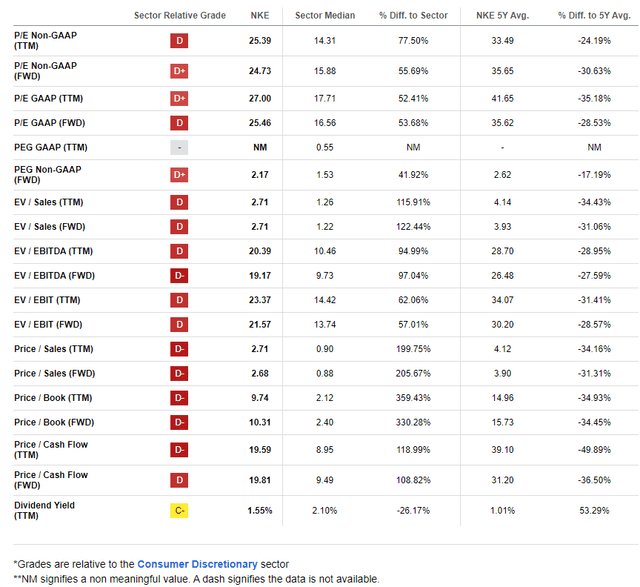

Meanwhile, the dividend is expected to remain at its current annual run rate of $1.48, so the 1.6% yield, which is slightly higher than the S&P 500, is unlikely to attract income investors. But with an earnings multiple now well below its 5-year average and an EV to EBITDA ratio close to that of the broader market, there is a good value case emerging. Finally, the free cash flow yield is solidly above 4%.

Nike: Earnings, Valuation, Dividend Yield, Free Cash Flow Forecast

Bank of America Global Research

If we assume $3.90 non-GAAP EPS over the next 12 months and apply a 28 multiple, roughly eight cycles cheaper than its long-term average, shares should trade near $109, giving That makes the stock undervalued by 20% today. Almost every valuation metric suggests the stock is cheap compared to history, though I don’t expect the mid-30s multiple to come into play anytime soon given growth estimates.

Nike: P/E has fallen by four more handles since late 2023

Seeking alpha

Compared to its peersNKE has a weak valuation score, but relative to its long-term trend, the valuation is attractive in my view. The footwear maker’s growth trajectory has been lackluster, and the main risk remains the tepid EPS growth outlook over the next few quarters.

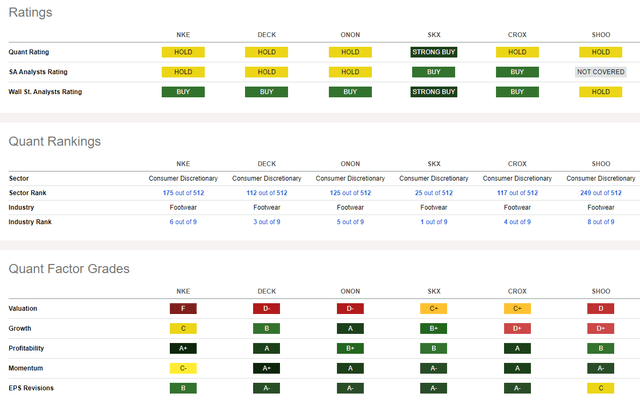

But Nike Profitability metrics Very strong sell side EPS Reviews It was on the good side, with 14 EPS upgrades and nine downgrades. finally, Stock price momentum The price remains tepid, and I will point out important chart levels to monitor the trend towards profits.

Competitor analysis

Seeking alpha

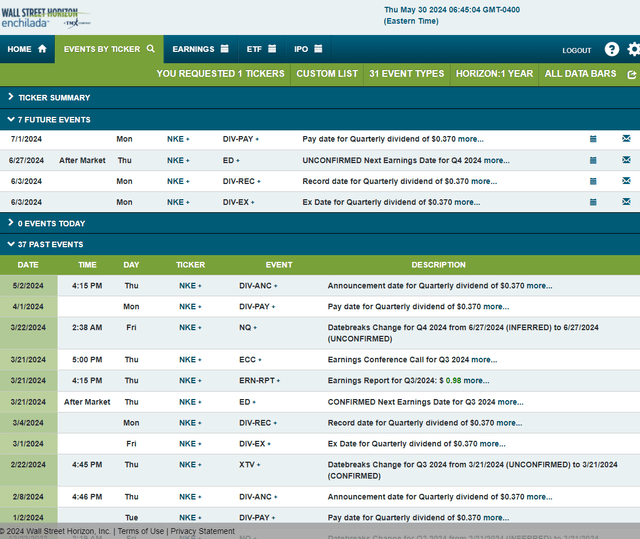

Looking ahead, corporate events data provided by Wall Street Horizon shows an uncertain Q4 2024 earnings date of Thursday, June 27. Prior to that, shares trade with a $0.37 ex-dividend on Monday, June 3.

Assessing the risks of corporate events

Wall Street Horizon

Technical take

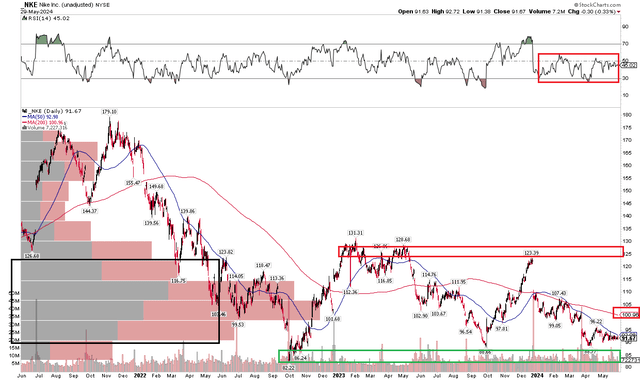

Since my last report on Nike, stocks have fallen while the S&P 500 has risen significantly. Notice in the chart below that stocks are now approaching key multi-year support in the low to mid 80s. As the stock continues to test this area, I am increasingly concerned that we will see a bearish collapse, but as long as the October 2022 low holds, a long bet could make sense.

I see resistance in the $123 to $131 area, but take a look at the RSI momentum gauge at the top of the chart – it is in the notorious bearish zone between 20 and 60. I would like to see a price increase come along with a breakout in the RSI that will hopefully break the bears’ hold on the underlying trend. With the long-term 200-day moving average having a negative slope, buying here is definitely going against the grain. Finally, it is possible that we could see NKE continue to trade between $85 and $100 based on significant volume in terms of price in the current area.

Overall, the NKE chart is not strong. It is showing absolute and relative weakness, but we have the October 2022 low to watch for support.

Nike: Stocks near critical support, resistance at $130

Stockcharts.com

Bottom line

I’m upgrading Nike from Hold to Buy based on review. While the technical situation is risky ahead of next month’s earnings announcement, the risk/reward setup seems reasonable in my view.