Kortnik/E+ via Getty Images

Investment summary

My recommendation for Nutanix, Inc. (Nasdaq:NTNX) is a Buy rating. Despite strong Q3 2024 results, share price trading has declined for reasons I believe are non-structural. Fundamental demand momentum remains strong and could be more so Viewed through multiple data points. The large deal won during the quarter was strong evidence that NTNX offers a solid solution, giving me confidence in its ability to continue winning deals.

Business overview

NTNX provides enterprise hyper-converged infrastructure solutions to address the need to store, move, and use data across multiple cloud platforms and endpoints through the enterprise cloud platform. Segment-wise, NTNX reports product revenues accounting for approximately 49% of total revenues and support and other services representing approximately 51% of total revenues. Subscription is ~93% of total revenue. Geographically, about 56% of total revenue comes from the United States and the rest from abroad. NTNX’s competitive moat is its leading position as the best hyper-converged infrastructure Provider in the industry. Its software infrastructure enables it to disrupt legacy storage solution providers as enterprises shift toward a hybrid, multi-cloud architecture to run applications and data.

Third quarter results update 24

Issued on 29y In May 2024, NTNX reported Q3 2024 revenue of $524.6 million, representing a change of approximately 17% year over year. This growth was driven by annual contract value (ACV) billings growing by 20% to $288.9 million. The main reason for the strong growth in both metrics was a large eight-figure deal with a North American-based Fortune 50 financial services company. YoY adjusted gross margins expanded 250 basis points to 86.5%, keeping adjusted EBIT margins at the mid-teens level (14% in 3Q24). In terms of guidance, management has narrowed FY24 revenue guidance to a range of $2.13 billion to $2.14 billion ($2.13 billion indicates ~14% growth) versus previous guidance of $2.12 billion to $2.15 billion, Keeping the midpoint unchanged. ACV billing guidance was raised by approximately 2%, implying approximately 18% year-over-year growth at the midpoint.

I was puzzled to see the NTNX stock price decline after such a very strong set of 3Q24 results. Looking at the headlines, it appears that the market is disappointed with management’s guidance for FY24, as it indicates a significant slowdown in growth on a Annual through Q4 2024. Whatever the case may be, this was a positive for me because the valuation went down a lot. In my view, NTNX posted a very strong quarter in Q3 2024, and there are several data points that point to very strong demand momentum and future growth potential.

Very strong billing performance

First and foremost, strength was evident in value-added billings growth of 20% year-on-year, which fell 700 basis points above management’s guidance, driven by better-than-expected renewal performance. I don’t think this massive outperformance is just a blip, as the dollar value of the $1M+ line of opportunities at ACV is up 50% year over year over the last three quarters, and the same set of opportunities is up 30% in Q3 24. It is clear that demand momentum remains strong, especially considering that we are in a somewhat uncertain macroeconomic environment.

The problem with this volume of high ACV trades flowing into NTNX’s P&L is that it results in greater variance in new and expansion business, and this looks bad on the surface because it makes it seem as if NTNX is advertising double the value of its ACV and Annual Recurring Revenue (ARR). ) ) Performance (due to the timing of closing trades and the way these trades are structured). Hence, I urge investors to take a step back and see how NTNX has performed over the long term. In my opinion, this volatility situation will improve over time as NTNX expands its portfolio of large clients, which will give it a larger pool of renewals each year, and this should somewhat offset the disparity in the performance of its new and expansion business.

The highlight of the quarter was an 8-figure ACV deal with a North American Fortune 50 financial services company. This is a good example of how new and larger ACV deals can impact ACV and ARR performance. It takes a long time (about 2 years for this client) to complete a trade, and naturally a lot of resources are allocated to completing it, which means there will be periods when ACV/ARR performs less. Most importantly, it demonstrates that NTNX solutions offer a good value proposition to organizations, and have the potential to turn these potentially large deals in the pipeline into actual revenue. Another example cited during the call that indicates NTNX’s momentum in winning share is the renewal and expansion with a North American-based Fortune 500 consumer packaged goods company (previously split between NTNX and a competitor, but NTNX is now the sole provider).

Partnering with Dell has significant benefits

The next positive point is the new relationship with Dell. At the .Next conference, NTNX revealed its plans to release its AHV hypervisor with support for triple-tier architectures that use Dell PowerFlex storage. When it arrives in 2025, it will be the first to allow AHV use without undergoing the transition to a hyperconverged architecture. This is huge because it eliminates the need for organizations to upgrade hardware (saving costs), essentially reducing adoption friction and making it easier for NTNX to convince potential customers.

evaluation

Redfox Capital Ideas

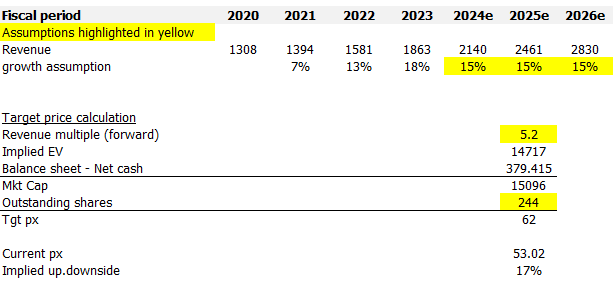

I model NTNX using the forward revenue approach, and using my assumptions, I believe NTNX is worth $62. I expect NTNX to easily grow 15% over the next few years, using the high end of FY24 revenue guidance as a baseline. I point out to readers that my assumptions on growth are somewhat conservative, considering that the industry is expected to grow at a CAGR of 23% from 2024 to 2032. The reason I am conservative is not because I believe NTNX will lose share in the near term. , but because the macroeconomics are still uncertain (some organizations may continue to delay migrations).

The growth in revenue base should directly benefit NTNX’s bottom line, which can be seen from the strong expansion in EBITDA margin since FY22 (from -11.1% in 1Q22 to 14% in Q3 From the year 24). I expect this move to continue as there is still plenty of room for expansion, given that pro forma gross profit margin is trending in the high 80s.

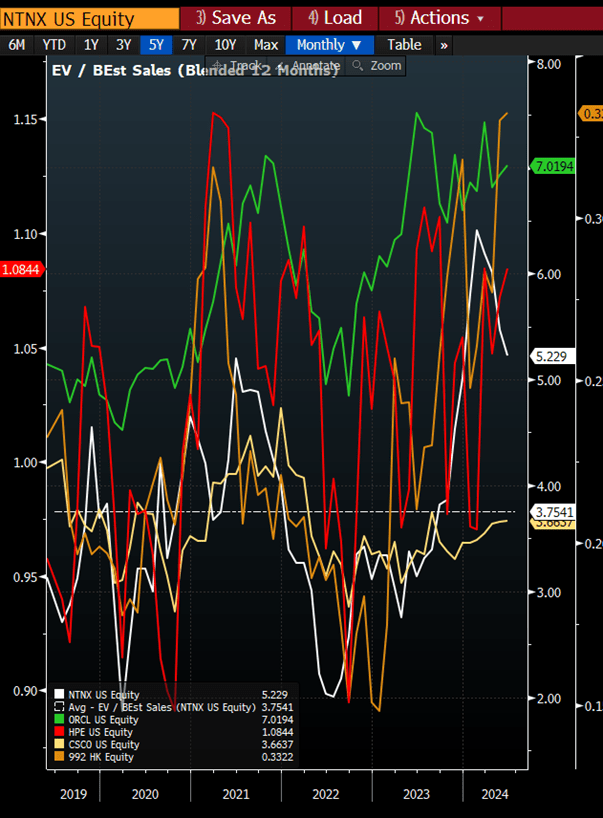

The good thing is that even assuming conservative growth, the upside is attractive considering that the valuation has fallen so much. For background, since the beginning of the year, NTNX’s stock price has risen very strongly, increasing the valuation to as much as 7.4 times forward revenue (which is roughly a 75% premium versus the average of other infrastructure software peers like Oracle and Dell and Hewlett). Packard Enterprise, Cisco, Lenovo, etc.).

NTNX is currently trading at 5.2x forward earnings, and I would argue that NTNX is worth trading higher than 5.2x given its better relative growth rate versus some of its peers. For example, NTNX is growing in the mid-teens but is trading at 5.2x, while Oracle is growing at 10% and is trading at 7x. However, I assumed 5.2x in my model, as I didn’t want to be too aggressive in assuming an upward rerating.

Bloomberg

risk

Moving to NTNX requires the purchase of a server, which increases the initial investment required to move. The danger is that this still poses significant friction when NTNX attempts to convert a prospect, thus limiting growth potential. New Dell partnership provides an alternative for enterprises. However, for NTNX to truly demonstrate its value proposition, it is still better for customers to shift to hyperconverged infrastructure. Without this step, the quality of solutions provided by NTNX may not be the best, and this may impact NTNX’s ability to retain customers.

Conclusion

My view for NTNX is a Buy rating due to strong demand momentum and future growth potential. Several data points support this, including a large eight-figure deal with a Fortune 50 financial services company in North America and a 50% year-over-year increase in the dollar value of the opportunity pool. The new relationship with Dell is another positive factor. While the upfront cost of purchasing a server can be a hurdle, I believe enterprises will continue to move to hyperconverged infrastructure as the long-term value proposition remains attractive.