Nutanix Stock: Buyable Decline, Weaker Outlook May Just Be Related to Deal Timing (NASDAQ:NTNX)

Diverse photography

Small- and mid-cap growth stocks have seen tremendous strength this year, facing both very high expectations and major disappointments in this earnings quarter. This is what happened to Nutanix (Nasdaq:NTNX), a specialist infrastructure software vendor In hybrid and private cloud deployments.

Nutanix has been booming all year on the hope of an AI boom (as more and more organizations look to deploy generative AI applications to automate more internal processes, one of the biggest upfront expenses is setting up the data center and back-end infrastructure – which is what Nutanix specializes in). But despite strong financial results for the third quarter (May quarter), weak expectations for the fourth quarter caused Netflix shares to fall more than 25% after earnings, bringing the company’s year-to-date gains to “just” 20%.

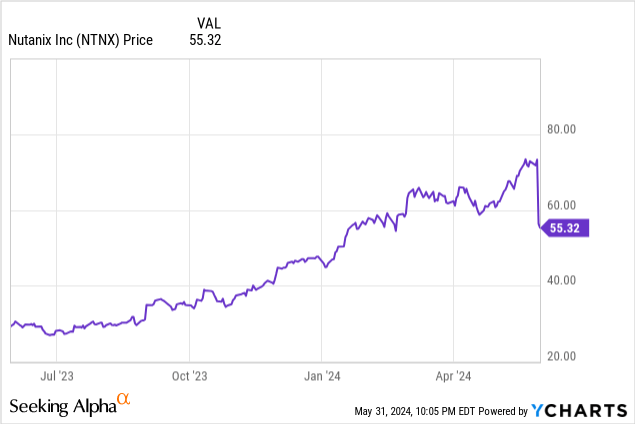

I last wrote a neutral cautionary note on Nutanix in April, when the stock was at the time It is still trading in the mid-60s. At the time, I had argued that the stock’s massive year-to-date rise had gone too far relative to its actual fundamentals, and that its valuation was a major chink in its armor. In my view, the massive post-earnings sell-off was largely driven by the cannibalization of inflated valuation.

But as usual in a volatile climate, investors have taken a very short-term mindset (ignoring, for example, the fact that Nutanix consistently beats its conservative forecasts by a wide margin). There’s a chance Nutanix’s softer Q4 outlook is just a statement when Large trades will be closed (more about this in the next section). While I still think Nutanix is fairly expensive, I think there is room for recovery in the short term. I remain neutral On Nutanix: I wouldn’t recommend getting into a long-term position here, but I would be comfortable buying Nutanix shares in the low-mid 50s for some short-term trading.

On the bright side for Nutanix: The company continues to grow its ARR strongly, as we’ll discuss in the next section. Generative AI is quickly becoming the primary catalyst for Nutanix’s workload expansion, and these deals generate recurring revenue at a very high margin. The company is shifting its sales compensation structures to maximize bonus annual Invoices rather than total invoices have helped boost the annual rate of return (ARR) with shorter contract terms, leaving more room for price increases and increased sales on renewal dates (although this also comes with higher volatility risk).

However, there are still a number of risks, the most important of which are:

- Nutanix will always compete with public clouds, and how to settle the dynamic between private and public clouds in the long term is still a question mark. Nutanix strives to create an efficient, cloud-like environment for IT infrastructure, but not the public cloud. More and more companies are abandoning their own data centers in favor of completely offloading to public cloud services. It remains to be seen how Nutanix will cope with this long-term trend.

- Slowing growth rates. Despite the AI tailwind, Nutanix is seeing a deceleration in most of its key metrics, including revenue, ARR, and ACV. This may call into question the stock’s more expensive valuation multiple.

- evaluation. AI enthusiasm has pushed Nutanix’s revenue multiples to what I think are very opportunistic heights, without much room for further expansion.

To break down the valuation details further: At current stock prices near $55, Nutanix is trading with a market cap of $13.52 billion. After we divested $1.65 billion of cash and $1.27 billion of convertible debt from Nutanix’s most recent balance sheet, the company’s result Enterprise value: $13.15 billion.

Meanwhile, for the upcoming fiscal year FY25 (year ending July 2025), Wall Street analysts have a consensus revenue target of $2.48 billion for the company, or 16% year-over-year growth. This puts Nutanix in 5.3x EV/Revenue FY25.

In my view: Nutanix will remain within range, trading at between 5-6x revenue in the short term. However, over the long term, as growth continues to decelerate, I think we will see valuation multiples compress to less than 5 times revenue in line with other software stocks generating just single-digit growth (Box (BOX), Dropbox (DBX)), etc. similar).

Bottom line here: A short-term trade might make sense for Nutanix after its significant post-earnings decline, which I consider to be a gross overreaction to the conservative outlook (and current high valuation). But I won’t be too greedy here, because I don’t think Nutanix can easily recover to pre-earnings levels of $70 or more – and that’s a position that needs to be watched closely.

Download Q3

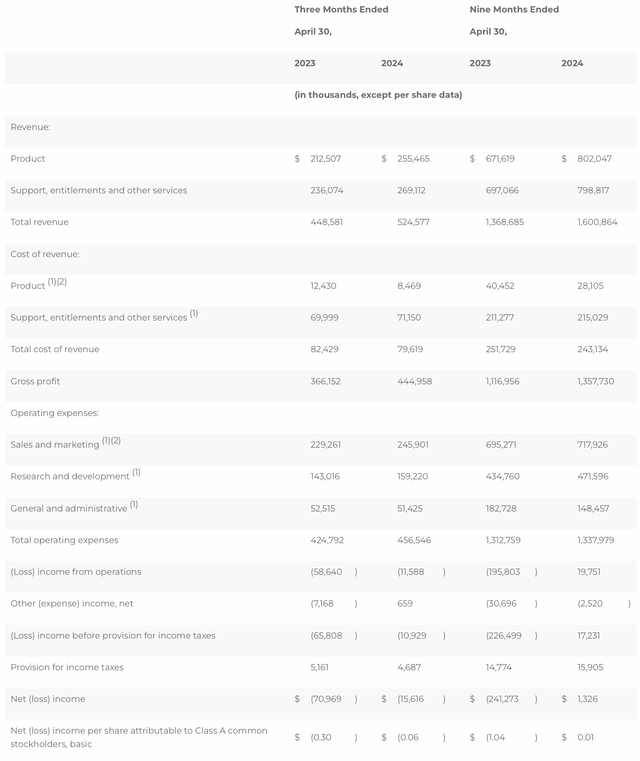

Let’s now cover Nutanix’s third-quarter results and its even more disastrous Q4 forecast in more detail. The third quarter earnings summary is shown below:

Nutanix Q3 results (Nutanix Q3 Earnings Group)

Nutanix’s revenue grew 17% year-over-year to $524.6 million, actually beating Wall Street expectations of $516.8 million (+15% year-over-year) as well as its guidance range of $510-$520 million. The company notes that despite the weaker macro environment, companies are still looking to prioritize digital transformation and AI projects, while also optimizing data center costs – which is key to Nutanix’s sales.

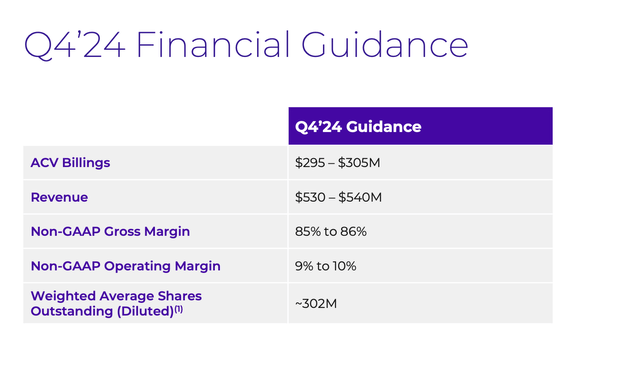

However, it was Nutanix’s forecast that angered investors. The company’s guidance for the fourth quarter calls for revenue in the range of $530 million to $540 million, or slowing to 8% growth at the midpoint.

Nutanix Q4 Forecast (Nutanix Q3 Earnings Group)

However, there is an explanation here. Nutanix management has noted that its pipeline is filled with a higher mix of larger, strategic enterprise deals — which are naturally subject to more executive scrutiny and take longer to close. According to CFO Rukmini Sivaraman on the third quarter earnings call:

I will now provide some comments regarding our updated guidance for FY24, specifically the following four points: First, we are seeing significant continued new and expansionary opportunities for our solutions. However, we continue to see a greater mix of larger deals in our pipeline resulting in more variation in our new and expansion business. The number of $1M+ ACV opportunities in our pipeline has increased by more than 30% for each of the last three quarters compared to the corresponding quarters last year.

Relatedly, pipeline dollar volume of opportunities greater than $1M in ACV increased by more than 50% and for each of the last three quarters compared to the corresponding quarters last year. These larger opportunities often involve strategic decisions and executive approvals, causing them to take longer to close and have greater variation in timing, outcomes and deal structure.

As mentioned earlier, we have continued to see a modest lengthening of average sales cycles compared to historical levels. Our fiscal ’24 ACV and ARR new and expansion performance to date has been impacted by these dynamics and has been below our initial expectations at the beginning of the fiscal year. We expect these dynamics to continue into the fourth quarter. For example, for the eight-figure ACV transaction in Q3 mentioned by Rajeev, we expect billings and cash collections to be in Q4, while the associated subscription revenue is expected to be recognized over several years starting in FY25.

The fact that Nutanix’s pipeline is full of big deals is a… good something: But we have to let go of short-term thinking and be willing to see revenues come in over a longer period of time until we feel comfortable with that.

We also note that Nutanix continues to exceed profitability, with pro forma operating margins growing 17.3% during the quarter 1350 basis points on an annual basis Compared to only 3.8% in the third quarter of last year.

Main sockets

In the short term, I believe Nutanix will overcome its guidance miss and outperform in Q4, especially if it continues to focus its messaging on a healthy pipeline. However, in the long term, I think Nutanix will grow will Moderate and its rating does not leave much room for upside. I’m willing to take a short-term trade here, but I’m not blindly holding this stock long-term.