Klaus Wedefelt/Digital Vision via Getty Images

Thesis summary

Nvidia company (Nasdaq: NVDA) reported first-quarter earnings last week, beating expectations and providing strong guidance. But was there anyone who really didn’t expect this?

On the earnings call, we learned a lot about the new company Product, Blackwell chips. It’s now been a year since Nvidia chips launched the AI revolution, so where does the company stand now?

In my last article, I highlighted the fact that while AI is not a bubble, Nvidia might be. You’ve pointed out some obvious similarities between AI/Internet and Nvidia/Cisco (CSCO) systems.

My opinion at the time was that Nvidia didn’t even need to do a bad job for investors to see a significant loss in value at those prices, and today I reaffirm that sentiment.

We are seeing a definite slowdown in growth in the face of competition Accelerating and profit margins are taking the lead. Blackwell’s quick launch appears to be, in my opinion, a desperate move to stay ahead of competitors and investor expectations, but it may not work out as intended.

I am, in fact, downgrading Nvidia to sell, even though I won’t sell this stock. Valuation is as high as it has ever been, while expectations are also high and growth companies going forward will become very difficult.

Great company but not at these prices.

First quarter earnings

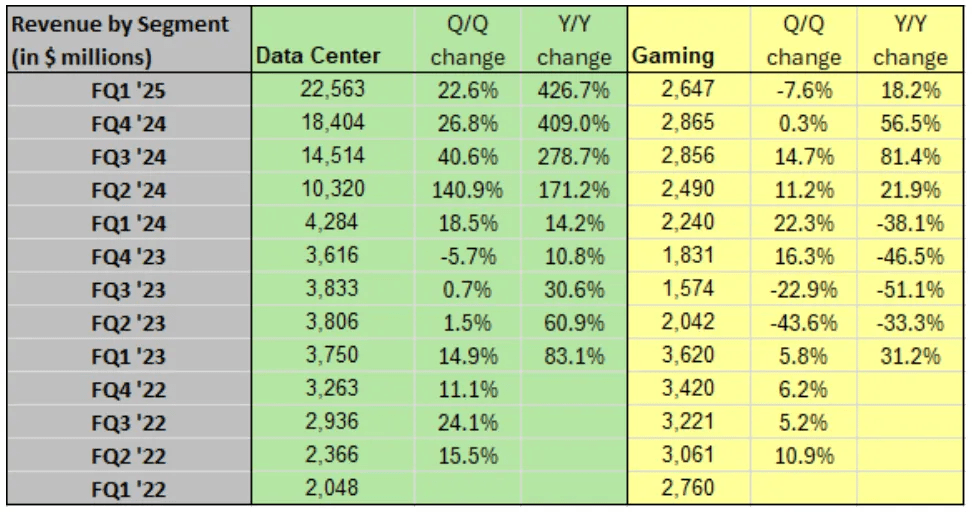

Just to quickly catch up on the latest earnings, Nvidia increased data center revenue by 426% year-over-year.

Nvidia revenue (Sa)

We can see in the chart above how Nvidia’s data center and gaming revenues have evolved. Gaming revenue actually declined on a sequential basis, while data center revenue rose 22.6%. We can also appreciate that quarterly growth is slowly slowing down, although it is still a healthy +20%.

Based on the company’s guidance, the next quarter should see approximately $28 billion in revenue, implying 25% growth in revenue.

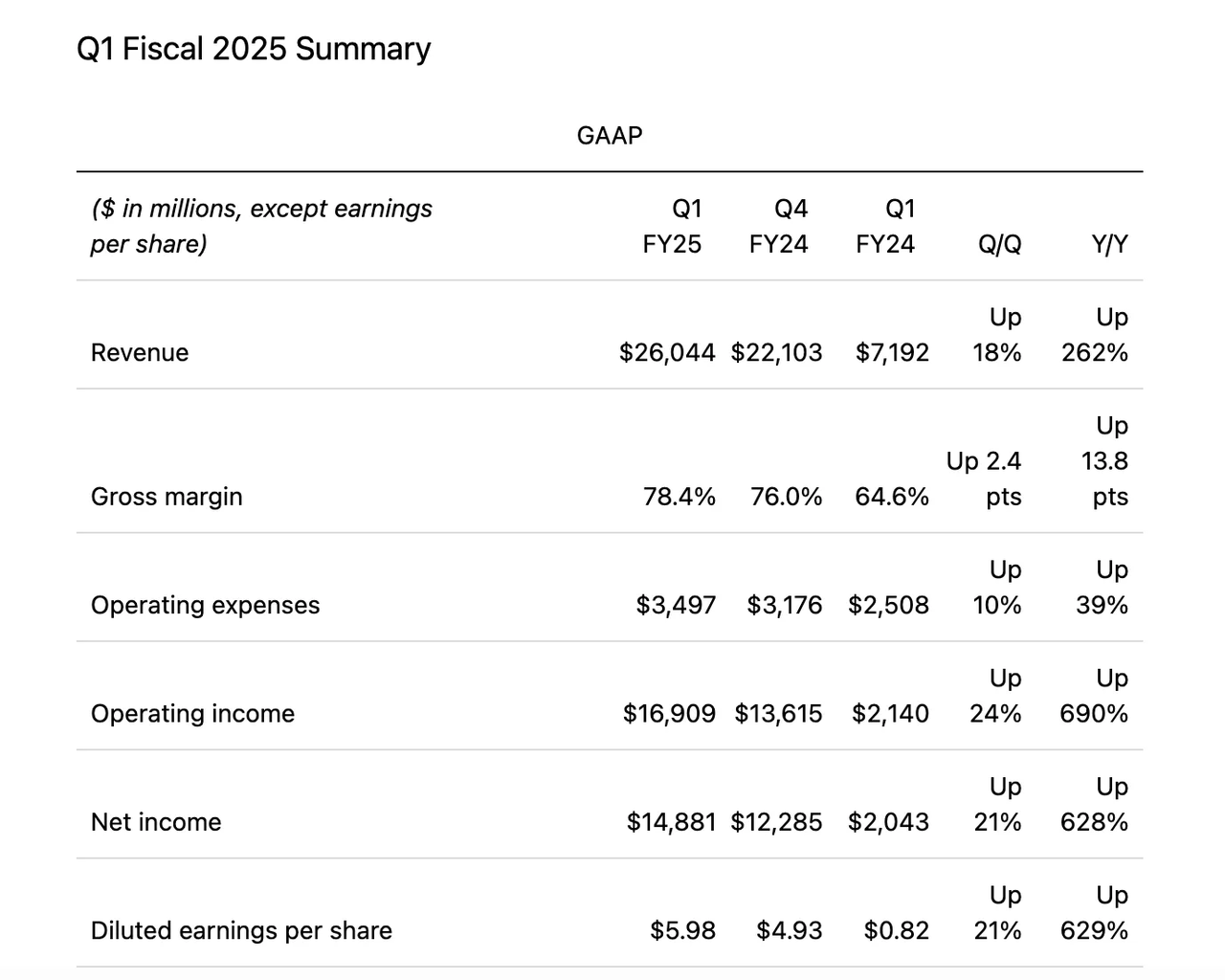

On the earnings side, Nvidia generated just under $6 GAAP earnings per share.

NVIDIA Financial Summary (press release)

Gross margin rose to 78.4%, although based on guidance, this should decline to the mid-70s range in the coming quarters.

So, overall, this was another great quarter, but with some fundamental concerns emerging in my opinion.

Nvidia will struggle to maintain these high levels of growth, which we are already seeing. Moreover, it appears that profit margins may also be through the roof.

With all eyes on the AI giant, Nvidia knows it has to keep the gas pedal on, and it’s responding with its new chips and AI architecture.

Blackwell

If AI chips are what the market wants, that’s what Nvidia will provide. The Blackwell platform was mentioned 40 times in the earnings call.

At GTC in March, we launched our next generation AI factory platform, Blackwell. The Blackwell GPU architecture delivers up to 4x faster training and 30x faster inference than the H100 and enables real-time generative AI on large trillion-parameter language models.

Source: Earnings call.

Blackwell is supported by the new H200s and the upcoming B100, GB200 and B200 GPUs. The platform is designed to be backward compatible, so customers can easily migrate from older versions.

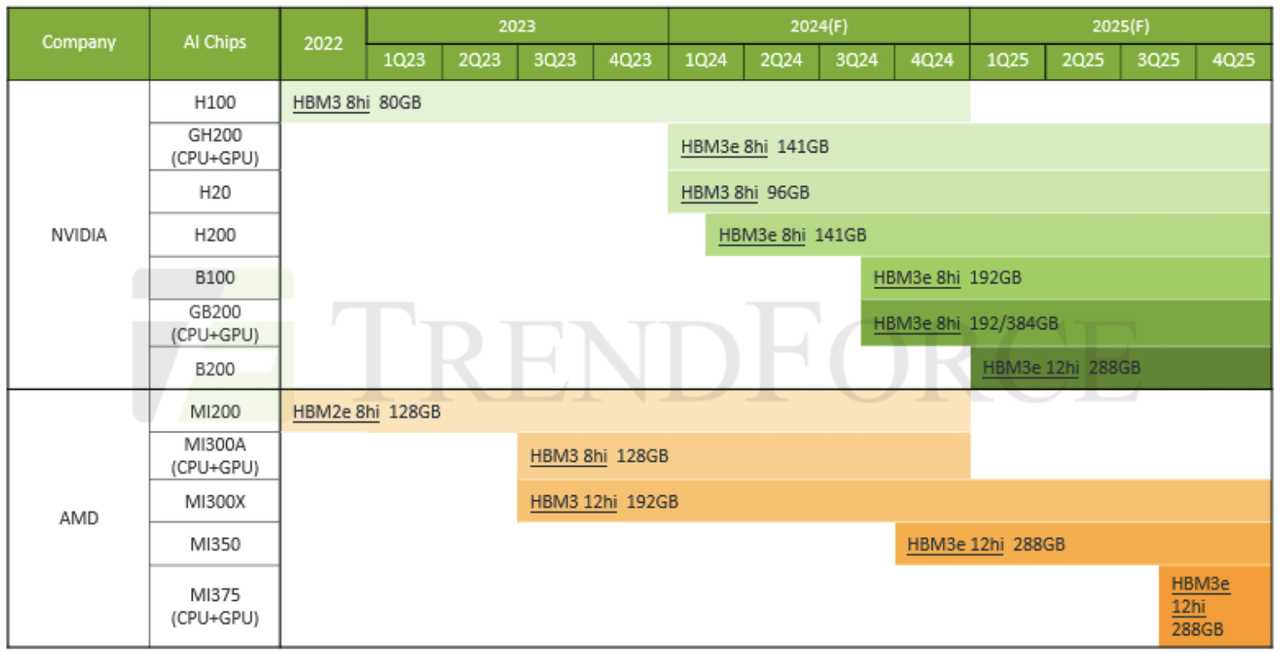

And according to the earnings call, we will actually see significant revenue from Blackwell. See below the expected timeline for Nvidia and Advanced Micro Devices (AMD) products over the next eight months.

A roadmap for its products (Trendforce)

Nvidia’s quick launch of the Blackwell may come as a surprise, given that it can already cannibalize the H200 hardware, which is only a year old. However, if the rumors about the price and performance are accurate, there is certainly no reason to wait.

According to rumors, the Blackwell architecture will be priced at $30,000 to $40,000, about 20% to 30% higher than the H100. While this may seem like an expensive upgrade, it should actually save its customers money, as Nvidia has stated that the B200 will deliver 30 times higher performance.

Competitive pressures and peak growth

However, Blackwell’s launch and the overall speed of new releases could also be symptoms of something much worse.

Nvidia’s competitors are closing in, and the company must continue to offer higher-performance chips in order to stay ahead of competitors and continue to provide more revenue and profit growth.

We can see clear evidence of this already. Just last week, Nvidia was forced to cut the price of its top chips in China, due to weak demand and competition from Huawei.

However, according to Reuters’ three supply chain sources, there is an oversupply of chips in the market, indicating weak demand.

Source: SA press release.

Moreover, AMD also seems to be ahead of Nvidia. In a press release last week, AMD confirmed that its MI300X accelerators are being used to run Azure OpenAI workloads.

According to Reuters, Microsoft (MSFT) is now offering its Azure customers an AMD alternative to Nvidia AI chips.

Overall, NVIDIA has a lot going against it at this point. Expectations are sky high as competitors catch up, and customers are clearly happy to change their models or even wait for newer models.

For example, Amazon ( AMZN ) has paused its purchases of H100 devices to wait for updated Blackwell models. Clearly, the company doesn’t mind waiting for better performance at a reasonable price.

It seems like the days when Nvidia chips were flying off the shelves are long gone before they get there.

evaluation

All of this brings us back to the main issue at stake: Nvidia’s valuation.

When I last covered Nvidia, I did acknowledge that after massive earnings growth and upwardly revised forecasts, the stock didn’t actually look that cheap.

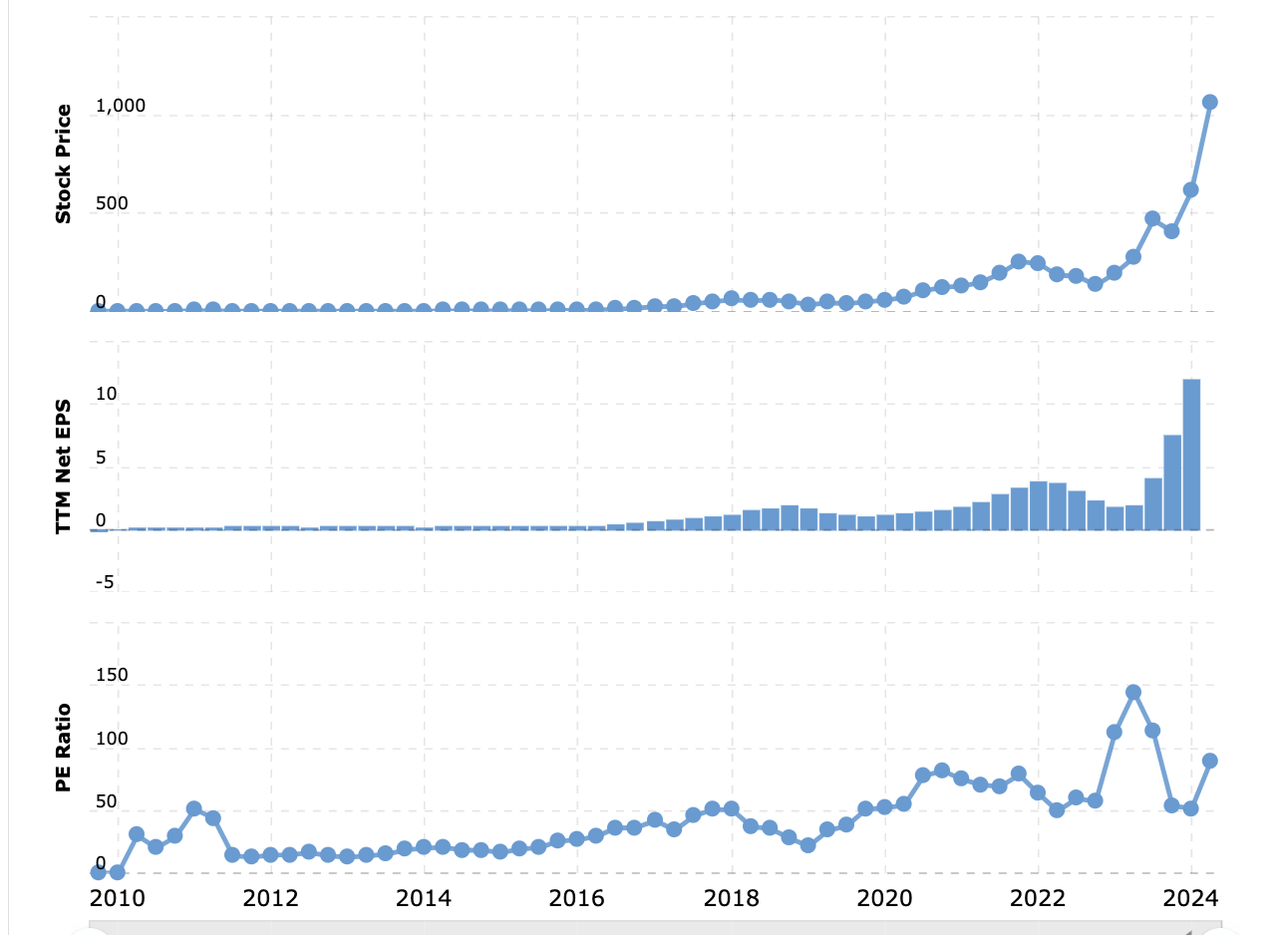

In fact, after these earnings, Nvidia was actually trading at a lower forward P/E than Apple (AAPL), which is not the case now.

NVDA EPS and PE price (macro trends)

Nvidia’s current P/E ratio is just under 90 according to Macrotrends, and this continues to expand as the stock rises.

Nvidia has always had a high P/E ratio, but it was only higher during 2023, when huge earnings growth was expected, and was therefore deserving of this valuation, as the P/E was actually revised significantly with each new quarter.

Ultimately, Nvidia is now more expensive than ever, while its growth prospects from here on out may worsen every quarter.

He stays away

While I rate Nvidia a sell at these levels, I wouldn’t recommend short selling the stock either. There is likely room to rise as the hype around AI continues, but I still believe that today’s irrational exuberance will eventually give way to a significant sell-off.

As I pretty much pointed out in my last article, Nvidia doesn’t even need to stop performing well for the stock to lose 40% to 50% of its value. All it has to do is start doing worse, as was the case with CSCO in the early 2000s.