Richard Drury

OKTA continues to present a compelling investment thesis in cybersecurity, thanks to its established consumer base

We’ve previously covered Microsoft (MSFT), CrowdStrike (CRWD), and Palo Alto Networks (PANW) in various Other articles, covering the bullish rise of its shares thanks to strong cybersecurity booking trends, attributed to the ongoing cloud migration after the Covid-19 pandemic and now renewed, thanks to the generative AI boom.

In this particular article, we’ll look at Okta (Nasdaq:OKTA) and share our findings on the stock, continuing the theme surrounding the cybersecurity sector.

OKTA is a cybersecurity SaaS company that provides secure digital access technology to cloud-based consumers ranging from small and medium-sized businesses to enterprises, universities, and government agencies, also known as “single point user authentication.”

As evidence of its strong market share of 22.15%, it was not surprising that the company announced amazing results within 4 years. Highest CAGR of +40.2% between FY2020 (FY19) and FY2024 (FY2023), while finally turning moderately profitable in FY2024 (FY2023).

This has also resulted in an impressive 3-year stock return of +240% compared to the broader market of +77% between FY19 and FY2021.

Unfortunately, OKTA also reported a series of security breaches in January 2022 and August 2023, leading to painful market capitalization and stock price corrections of more than -60% at its worst, as management also lost some credibility as a cybersecurity company.

Then again, it’s important to highlight that OKTA is not the only one targeted by hackers, as MSFT and CRWD face similar issues to varying degrees, an expected outcome due to the continued proliferation of the Internet and cloud migration.

For now, we think it’s important to highlight OKTA’s double earnings call for Q1 2025, with total revenue of $617 million (+1.9% QoQ/+19.1% YoY) and adjusted EPS of $0.65. (+3.1% QoQ/+195.4% YoY).

With growing annual subscription revenues of $2.41B (+2% QoQ/+19.8% YoY) and gross subscription margins expanding by 83.5% (-0.2 points QoQ/+2 YoY), it’s clear Consumer demand for cybersecurity offerings remains strong despite potential headwinds from breaches to date.

The same was observed in its total client base growing to 19.1K (+0.15K QoQ/+1.05K YoY) and an excellent Net Dollar Retention Rate of 111% (QoQ/+6YoY), indicating To its ability to continually cross-sell to existing consumers while stimulating new adoption.

Readers should also note that OKTA’s bottom-line improvements are largely attributable to improved management operational costs (reduced headcount, among other things) at a longer sales cycle time.

This resulted in its dedicated operating income expanding by $133 million (+3.1% QoQ/+259.4% YoY) and 22% richer margins (+1 point QoQ/+15 y/y).

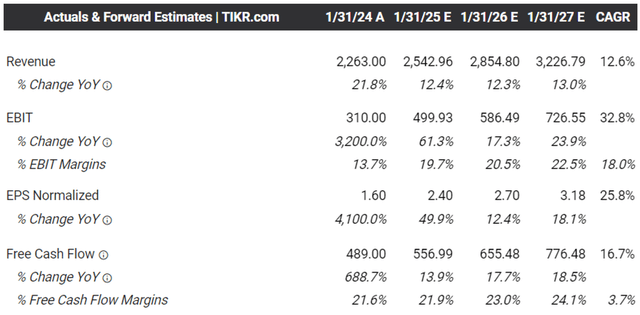

Finally, OKTA provided promising guidance for fiscal 2025 revenue of $2.535 billion (+12% y/y), adjusted operating margins of 19.5% (+5.5 y/y), and adjusted EPS of $2,375 (+48.4% y/y). Annually), which indicates management’s confidence to achieve accelerated profitable growth in the future.

This is also supported by the large addressable market size of $80 billion, which puts the cybersecurity company in a fairly competitive position once the macroeconomic outlook returns to normal.

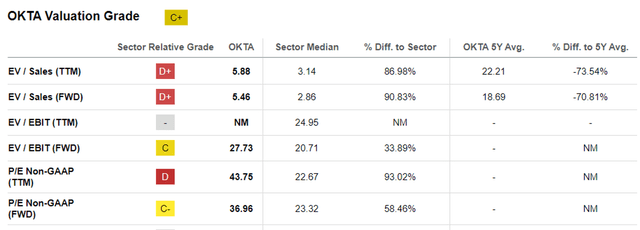

OKTA appears to be fairly valued compared to its peers

Okta Reviews

Seeking alpha

Currently, OKTA is trading at a significantly discounted FWD EV/EBIT of 27.73x and P/E FWD of 36.96x. This compares to its cybersecurity peers, such as CRWD at 82.27x/80.68x, Zscaler (ZS) at 55.99x/56.71x, PANW at 43.39x/52.74x, and Fortinet (FTNT) at 26.64x/32.74x, respectively. . .

Consensus future estimates

Taker station

This is likely attributable to OKTA’s mixed top/bottom growth with a projected CAGR of +12.6%/ +25.8% through FY2026, which is lower compared to CRWD at +27.5%/ +27.9% and ZS at +26.2%/ +31.4%, however improved from PANW at +15.8%/ +18% and FTNT at +12.2%/ +12.5%, respectively.

These numbers suggest that OKTA is reasonably valued at a FWD P/E of 36.96x, providing interested investors with a decent margin of safety.

Readers should also remember that the company continues to report growing multi-year remaining performance obligations (RPO) of $3.364 billion (quarterly included/+14.4% annualized) in the latest quarter, providing further insights into top-line performance over the medium term.

Combined with $214 million of incremental free cash flow generation (+28.9% QoQ/+72.5% YoY) and a 35% richer margin (+7 points QoQ/+11 YoY), we believe OKTA remains well positioned to invest opportunistically in its growth going forward.

This is done while reporting a healthier balance sheet, based on a net cash position of $1.16 billion in fiscal Q1 2025 (+11.5% QoQ/+115.2% YoY).

So, is OKTA stock a buy?Sell, sell, or hold?

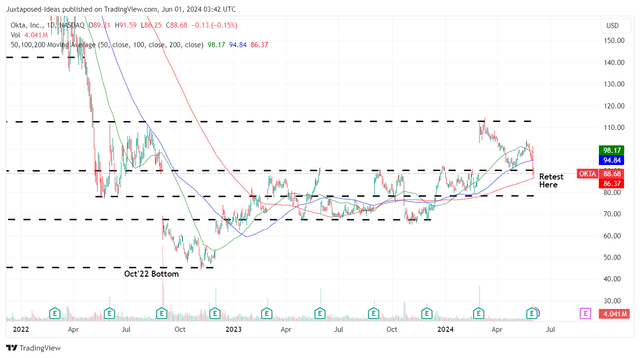

OKTA 2Y stock price

Trading offer

For now, OKTA continues to be penalized for security breaches, with the stock failing to recover to pre-January 2022 and pre-August 2023 levels.

It’s also why we believe OKTA’s reasonable valuations offer opportunistic investors the opportunity to capture dollar-cost averaging, especially since the stock is trading close to our fair value estimate of $75. This is based on LTM adj of $2.03 and a forward P/E of 36.96x.

Based on FY2026 consensus estimates for EPS of $3.18 (recently downgraded from $3.39, due to management’s cautionary tone on the recent earnings call), there remains excellent upside potential of +32.4% to the long-term price target of Also $117.50.

As a result of the attractive risk-reward ratio, we have initiated a Buy rating for OKTA, although there is no specific entry point as it depends on the dollar cost averaging of individual investors and their risk appetite.

For now, with the stock appearing to break through the previous $90 support levels, readers may want to monitor its movement a little longer and add a moderate bounce to its previous trading ranges between $78 and $83, as it presents patient investors with improving long-term upside potential.