Shidlovsky

Ocular Therapeutics Inc. (NASDAQ:OCOL) is a biopharmaceutical company that develops innovative treatments for the treatment of eyes. OCUL already offers a commercial product called Dextenza to treat postoperative eye inflammation and ocular pain and itching due to allergic conjunctivitis. The medicine is the market Success with net product revenue of $57.9 million in 2023. OCUL’s pipeline includes Axpaxli, an intravitreal axitinib implant in Phase 3 trials for wet age-related macular degeneration (Wet AMD) and Phase 1/2 trials for diabetic retinopathy, which I consider to be effective. Key value driver. Axpaxli could potentially unlock a decabillion-dollar TAM device if successfully developed and commercialized. Hence, I rate it as a ‘buy’ at these levels.

Betting on Axpaxli: Business Overview

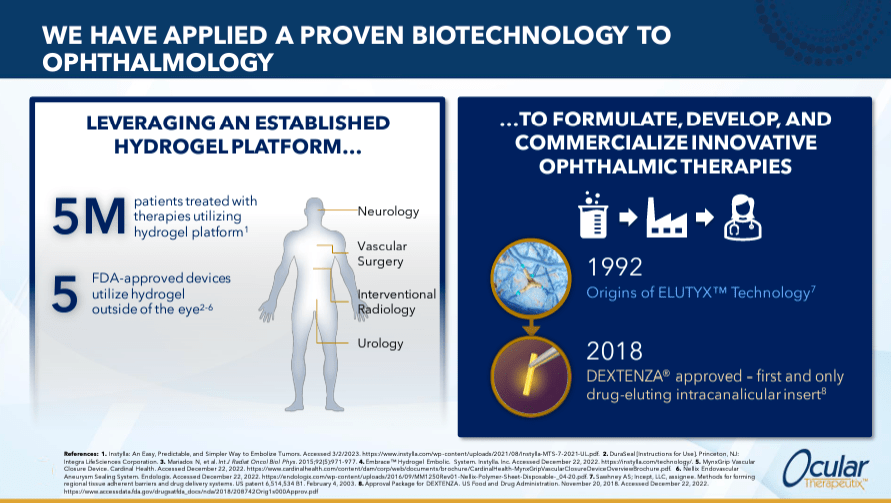

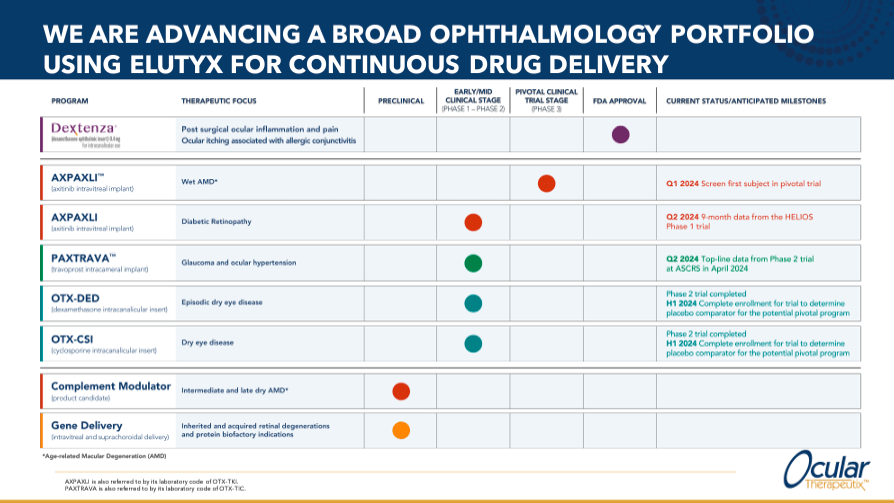

Ocular Therapeutix is a biopharmaceutical company founded in 2006 and headquartered in Bedford, Massachusetts. It develops new treatments for eye diseases, leveraging its drug delivery platform. This technology is called Elutyx, consists of a bioabsorbable hydrogel that provides sustained and targeted release of therapeutic drugs. Other promising candidates for OCUL are OTX-DED for episodic dry eye disease and OTX-CSI for chronic dry eye disease, which is also advancing through clinical trials.

Source: Company presentation – January 2024.

Specifically, OCUL’s flagship product is Dextenza for the treatment of post-operative eye inflammation and pain, which is also indicated for eye itching due to allergic conjunctivitis. As of 2023, the company claims to have treated approximately 400,000 eyes, with net product revenue of $57.9 million.

OCUL’s pipeline also includes Axpaxli, an intravitreal implant of axitinib, in phase III clinical trials. It is indicated for the treatment of wet age-related macular degeneration (Wet AMD), with the first subject being investigated in the first quarter of 2024. Axpaxli will also likely be indicated for the treatment of diabetic retinopathy, and OCUL is testing this in a Phase 1/2 clinical trial. For this indicator, 9-month Helios Phase 1 data is expected in the second quarter of 2024.

Axitinib is a tyrosine kinase inhibitor that targets vascular endothelial growth factor receptors (“VEGFRs”) associated with the formation of new blood vessels. As an intravitreal implant, the drug is delivered over a long period to the vitreous humor of the eye without repeated injections. This is one of the product’s selling points, as repeated injections can lead to infection.

Source: Company presentation – January 2024.

Another OCUL candidate is Paxtrava, also known as OTX-TIC, a phase II travoprost intracameral implant for the treatment of glaucoma and ocular hypertension. This drug is in Phase 1/2, with positive results from a Phase 2 trial announced in April 2024. Travoprost is a prostaglandin analogue prescribed to reduce intraocular pressure (“IOP”) to avoid damage to the optic nerve that can lead to vision loss. Loss. The intracameral implant delivers the drug directly to the anterior chamber of the eye, the space between the cornea and the iris, providing continuous delivery over a long period.

Source: Company statement – January 2024.

Furthermore, OCUL’s OTX-DED is an intraductal dexamethasone insertion. This can help treat occasional dry eye disease. It is undergoing phase II trials that are supposed to be completed by the first half of 2024. It is worth noting that dexamethasone is an anti-inflammatory and immunosuppressive agent that reduces inflammation, swelling, and pain. Intraductal insertion delivers the medication into the tear ducts, which are the ducts that drain tears from the eye into the nasal cavity. Therefore, it is undoubtedly a promising treatment if successfully developed and marketed.

Finally, OCUL’s OTX-CSI is an intracanalicular cyclosporine insert indicated for the treatment of dry eye disease. Phase 2 trials for OTX-CSI are expected to be completed by the first half of 2024. Cyclosporine is an immunosuppressive drug used to reduce inflammation and increase tear production.

Global expansion and pipeline advancement

OCUL is currently collaborating with AffaMed Therapeutics to develop and distribute Dextenza and Paxtrava in the Greater China, South Korea and Asian markets. On 19 February 2024, AffaMed announced that the Health Sciences Authority of Singapore (“HSA”) had accepted Dextenza for its New Drug Application (“NDA”). Affamed has also initiated a registrational trial in mainland China evaluating Dextenza versus placebo, with key data expected in Q3 2024. These milestones represent significant progress in scaling Dextenza in Asian markets and underscore the potential of the partnership with AffaMed.

Source: psmarketresearch.com.

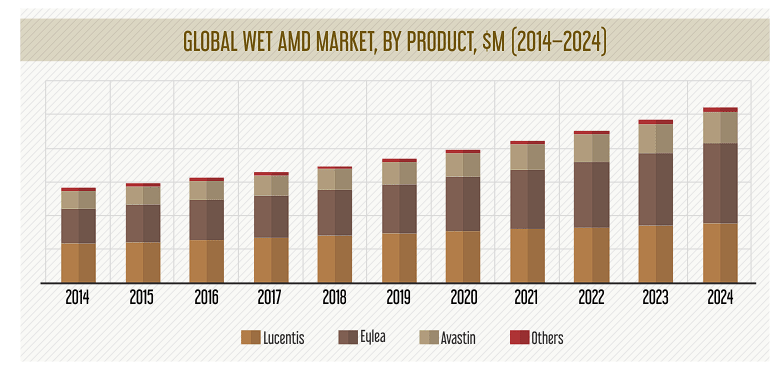

Moreover, in the most recent 10-Q, Axpaxli was the most important in its upcoming pipeline due to the SOL-1 and HELIOS trials. OCUL revealed that the SOL-1 trial should finish enrollment by the first quarter of 2025 and that the FDA appears receptive to this trial, as evidenced by the Special Protocol Evaluation designation. If successful, OCUL will likely file Axpaxli’s indicated NDA for Wet AMD in 2026 (speculative), allowing the company to tap into a large market. For context, Wet AMD is mostly in the hands of 3 players and is expected to generate revenue of $10.4 billion in 2024.

Justified Bonus: Valuation Analysis

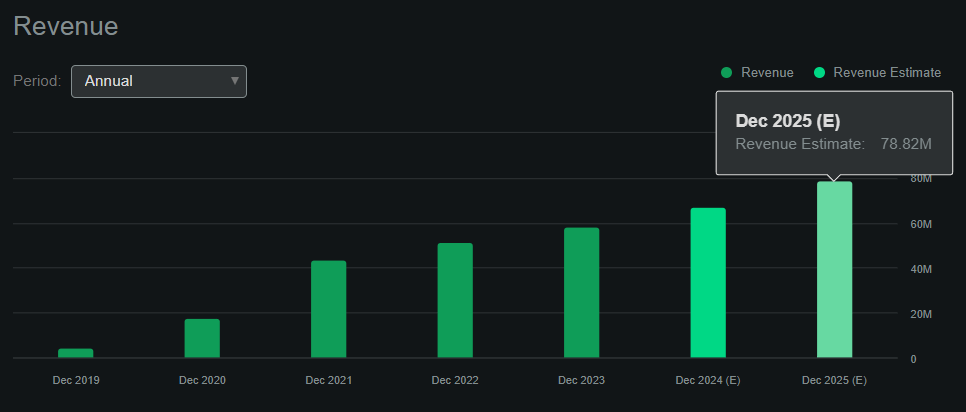

From a valuation perspective, OCUL trades at a market cap of $882.9 million. So it’s rapidly approaching a $1 billion valuation, so it’s a mid-sized biotech company at this point. But this makes sense because it is now generating ever-increasing revenues. According to Seeking Alpha’s dashboard on OCUL, the company is expected to generate sales of $78.8 million by 2025. However, the problem is that this implies a relatively high forward P/E ratio of 11.2. For comparison, the average forward P/E for its sector is just 3.63, so OCUL is trading at a significant premium compared to its peers.

Source: Searching for Alpha.

However, there are some caveats here. OCUL is still relatively small in the bigger picture. As I noted, its current revenue stream, Dextenza, will likely continue to increase for the foreseeable future, as its market acceptance appears favorable. But more importantly, OCUL’s Axpaxli has a clear path to FDA approval for Web AMD. Of course, the third phase is still pending, and this poses a risk to new investors.

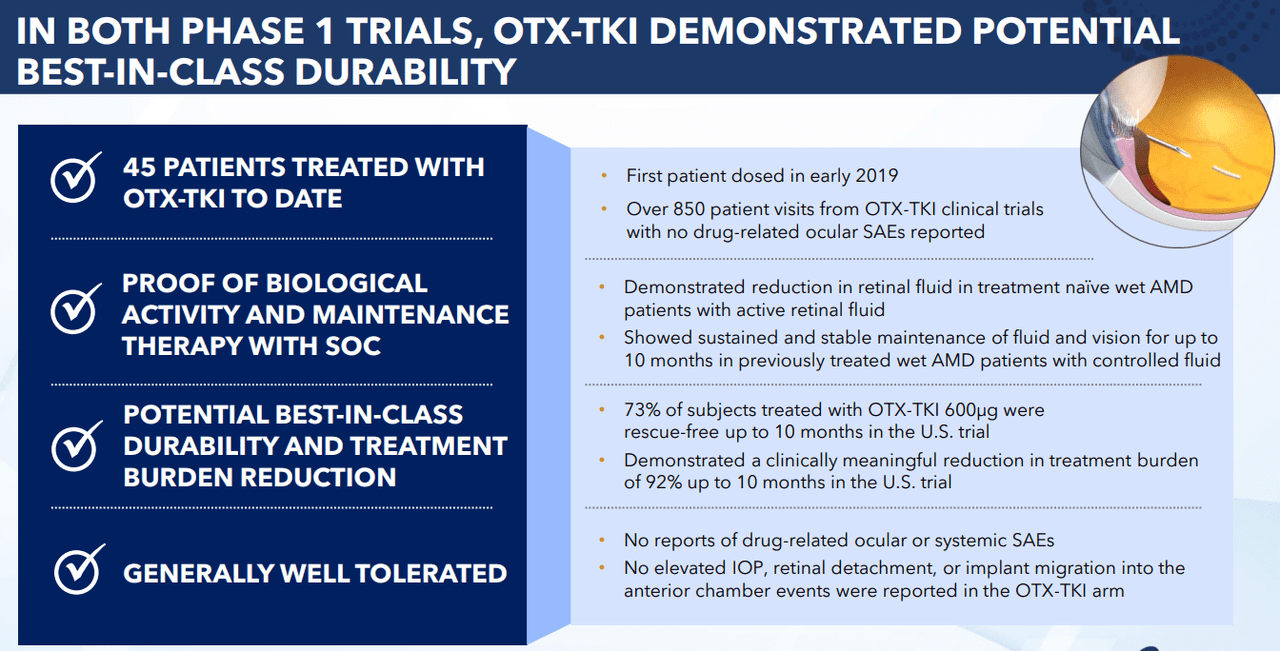

However, I believe Axpaxli is one product OCUL has under its sleeve, as early clinical trial data shows it could revolutionize treatment in this indication. The main attraction of achieving results similar to current treatment alternatives is its revolutionary point, with a 92% reduction in treatment (i.e. fewer injections required). I believe this would position Axpaxli as a best-in-class drug for Wet AMD, which means it should lead to a significant market share in this market. So, I think there’s good reason to believe it’s safe and effective, and as long as the Phase III trials confirm that, OCUL is on track to tap into a huge market in the next few years. If so, this would likely result in a significant market share for Wet AMD, meaning billions of dollars in annual sales.

Source: Company statement – January 2024.

In addition, data from the phase ½ trial show that Axpaxli for NDPR is well tolerated in patients, with no meaningful flare-ups observed. Importantly, 46.2% of patients taking Axpaxli saw improvements in the DRSS after 40 weeks, compared to the control group, which showed no improvement. So, I think the market is pricing OCUL’s potential with Axpaxli rather than its current revenue with Dextenza.

Furthermore, OCUL currently holds $482.9 million in cash against long-term debt of $66.5 million. I estimate that the company’s latest quarterly cash burn was $34.2 million by adding CFOs and net capital expenditures. If we annualize this number, it would mean an annual cash burn of $136.8 million. This means OCUL has a healthy 3.5-year cash runway. If Dextenza’s sales continue to increase, its runway could improve with this internally generated cash flow.

Therefore, OCUL has enough resources for the foreseeable future and is a very promising drug candidate that could unlock billions in revenue at Wet AMD in Phase 3. Unlike other biotech stocks, I would argue that OCUL has virtually no dilution risk at this stage for this stock . Reasons, which is also a bonus. Therefore, with that in mind, OCUL’s current valuation seems more reasonable. Therefore, I consider OCUL a good ‘buy’ in this price range, especially for investors who are betting on Axpaxli.

Investment Warnings: Risk Analysis

Of course, it should be noted that my thesis is based on the successful development and commercialization of Axpaxli. This is not guaranteed since the FDA has a relatively complex approval process, but I think the SPA designation is promising and may increase the odds of approval. However, if the FDA rejects or causes major setbacks for OCUL with Axpaxli, the stock’s valuation is meaningless based on Dextenza sales alone. Therefore, investors will be exposed to significant downside risks.

Source: Trading View.

Finally, if approved, I also assumed that Axpaxli’s value proposition would lead to significant market share for Wet AMD. However, this also depends on factors beyond Axpaxli’s core characteristics, such as OCUL’s marketing strategies, communication with healthcare providers, and insurance policies. These variables can reduce the potential of Axpaxli if management fails to navigate through them. Overall, I think these risks seem manageable and reasonable, but more importantly, justified in light of Axpaxli’s potential in Wet AMD.

Worth “buying”: conclusion

OCUL is a promising biotechnology company moving from its clinical stage to the commercial stage. Today, its main revenue stream is Dextenza, but I believe its main value driver is Axpaxli. Dextenza’s current revenue projects to be approximately $78.8 million by 2025. However, if OCUL receives FDA approval for Axpaxli in Wet AMD, it has the potential to be a best-in-class drug in a market worth tens of billions of dollars. This means that Axpaxli has greater potential than Dextenza, as the SOL-1 and HELIOS trials have shown promising early results. Furthermore, the company has a 3.5-year cash runway, with growing internal cash flow. This means that OCUL has minimal dilution risk and a concrete path to approval for a remarkably promising drug targeting a wide range of TAMs, setting it apart from other biotech investment alternatives. So, despite the inherent risks in the biotech space, I view OCUL as a ‘buy’ at these levels.