D-Keine/E+ via Getty Images

Investment thesis

Palo Alto Networks Inc (NASDAQ:BANU) Its stock fell almost 30% after its third-quarter fiscal 2024 earnings results. I think this big sell-off can be justified due to high expectations Generative AI drove gains, with the stock up 170% in February from a CY2023 low. in Previous article, I initiated a buy evaluation and discussed the company’s sustainable path to achieving the “Rule of 40” as its bottom line growth slows. Since then, the stock has risen more than 40%.

While the company still held its 40 bases last quarter, it is approaching the 40% edge, despite resilient underlying demand. My main concern is that sluggish billings expectations and mid-teens revenue growth will significantly hamper FCF growth. Meanwhile, the stock continues to trade as if it were a high-growth software company in the past. Therefore, I downgraded the stock to Neutral from Buy rating due to the outstanding valuation amid slowing growth. In particular, the P/E multiple has become more expensive compared to last year.

40-The rules still stand

Company model

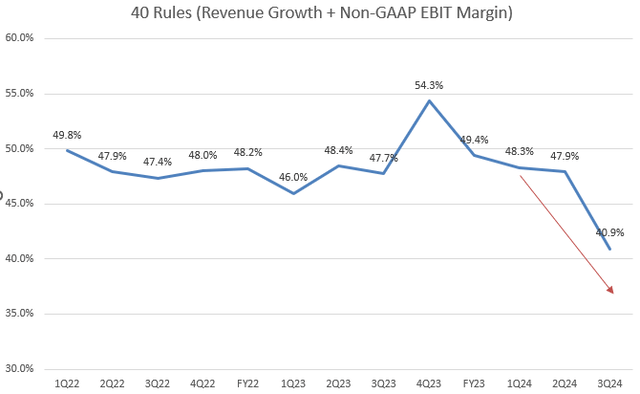

While PANW still achieved the 40 rules at a combined rate of 40.9% (revenue growth + non-GAAP EBITDA margin) in the most recent quarter, we note that the trend line has shifted downward, falling below 45% threshold for the first time since then. First quarter of fiscal year 2022. I believe this decline is primarily due to weak overall growth. Specifically, subscription and support revenue increased 20% year-over-year, down from 29% year-over-year in Q3 FY2023. However, it is encouraging to see that growth in the subscription revenue segment has remained relatively healthy, with increased By 25% on an annual basis.

In the press release, the company expects total revenue to grow 10%-11% year over year in the fourth quarter of fiscal 2024, approaching the “single-digit club.” Given last week’s initial price reaction to CRM’s earnings results, I believe there is anecdotal evidence that it could knock down investors’ psychological thresholds, potentially leading to increased volatility going forward.

Margins continue to expand

Company model

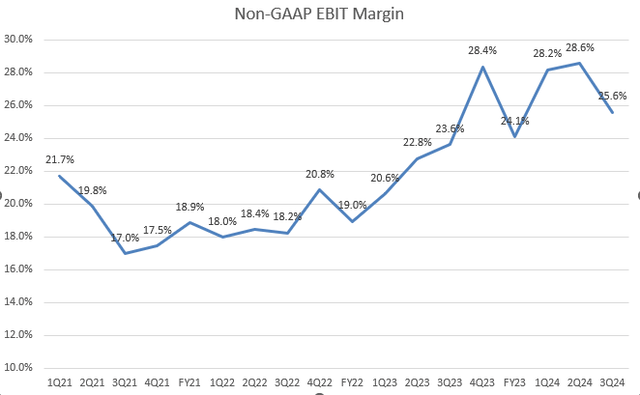

In addition, the company’s margins remain resilient, which is a positive sign. It is typical for a company’s margins to expand when revenue growth slows. However, we should keep in mind that some investors may not view PANW as a high-growth stock, which could impact the current premium valuation. As many SaaS companies position themselves as beneficiaries of generative AI, investors are eager to see accelerating growth and increased demand reflected in earnings reports. However, some software companies disappointed investors in the recent earnings season.

Significant slowdown in billing growth

Company model

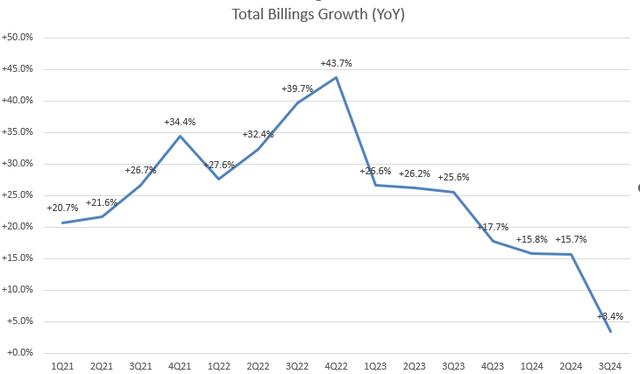

Let’s take a look at the chart. Billings play a crucial role as a key driver of FCF growth, reflecting the actual cash flow a company receives during a given period, as opposed to revenue. In my last article, I highlighted the company’s impressive billing growth. However, in Q3 FY2024, growth in total billings slowed to 3.4% year-on-year. It is worth noting that growth in current billings has slowed to single digits, rising 8% year-on-year for the first time in the company’s history.

As for guidance, the company is expected to grow at an average rate of 9.5% YoY in Q4 FY2024 and 10.5% YoY in FY2024, which is significantly lower than the +20% annual growth in fiscal years. Previous. “We have seen a higher volume of larger deals with some of these customers who have chosen to defer payments over the life of the purchase, rather than pay up front while they grapple with the rising cost of money,” management explained on the earnings call. They also expected this trend to continue in the future. I believe continued deferred billings will create significant headwinds to cash flow generation and free cash flow margin going forward. Typically, we would have seen free cash flow growth decline sharply to 14% y/y in Q3FY2024 from 40% y/y in Q3FY2023. So I expect the company to experience negative free cash flow growth over The coming quarters.

However, PANW bookings remain on track. This indicates that its AI products are seeing increasing demand, as evidenced by existing bookings growing by 20% YoY in Q3 FY2024 compared to 15% YoY in Q3 FY2023, driven by Significant with 20% YoY growth in Current Remaining Performance Obligations (cRPO). RPO shows the obligations in contracts that the company must fulfill later. This backlog can turn into future invoices and ultimately help generate revenue. While management stresses the importance of focusing on RPO and bookings, I consider it a red flag for PANW if we see a slowdown in both revenue and FCF growth.

evaluation

JP Morgan

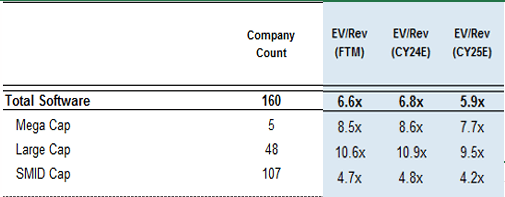

PANW currently trades at 53 times its non-GAAP P/E FTM even after a 20% decline from its February peak. This is roughly double the Nasdaq 100 P/E FTM of 27.5x. Meanwhile, the EV/Sales FTM ratio is currently 11.7x, which is higher than the large software average of 9.5x. I know it’s not a perfect comparison, but many investors were surprised by NVIDIA’s (NVDA) rise to the moon over the past 12 months. However, its non-GAAP P/E FTM ratio is only 41x, which is still cheaper than PANW.

Furthermore, PANW’s current non-GAAP FTM price/earnings ratio is roughly in line with its 5-year average of 54.3x. Despite a significant slowdown in total revenue growth, from +25% in FY2023 to the expected 16% in FY2024, the multiple remains roughly the same. I think this explains the optimistic view of re-accelerating growth under generative AI trends. Therefore, I would prefer to stay on the sidelines until there is more clarity on revenue growth from AI security services.

Conclusion

The bottom line is that buying the dip in PANW after the recent sell-off may not be advisable as the company’s recent earnings results did not meet the high expectations surrounding Generative AI and its previous rally. While PANW has maintained its accretive growth, there are concerns about the continued downward trend in revenue growth, which could result in PANW being removed from the 40 rules club in the coming quarters. The significant slowdown in billings growth and conservative forward guidance also raises doubts about future free cash flow growth. Although margins and bookings remain good, I believe the deceleration in revenue and free cash flow growth raises concerns about the current valuation multiple. Furthermore, PANW’s multiples, compared to the industry average and companies like NVDA, still look expensive. Therefore, I am downgrading the stock to Neutral to reflect these concerns. I think the current assessment has already taken into account the potential tailwinds for AI growth.