John M. Lund Photography Company

Palo Alto Networks (NASDAQ:BANO) is currently going through a major transformation phase as the company prioritizes its security product platform as IT departments seek to simplify their IT infrastructure through a single vendor approach. With the addition of their own co-pilot and security features related to GenAI, I believe Palo Alto has the potential to deliver continued revenue growth and margin expansion as the company expands its ability to sell additional security products. I expect Palo Alto to achieve continued growth as the company builds on its partnerships with IBM and Accenture as the security vendor of choice for the next generation of GenAI threat vectors. I reiterate my Buy recommendation on PANW shares with a target price of $352.74 per share at 13.34x FY25 price/sales.

As a disclaimer, my forecast and price target have been lowered from my previous recommendation earnings before Q2 2024. The report can It can be found here:

Palo Alto Networks still has gas in the tank

Palo Alto Networking Platform Strategy

Palo Alto Networks set the stage in its third-quarter 2024 earnings call for future periods as the company shifts its strategy more toward platforms and away from single-product sales. Although the strategy may seem less attractive up front from a corporate perspective, I believe this model will allow the company to further boost sales in the long term by cross-selling additional subscription features, such as AI Access Security, AI SPM, and AI Runtime Security features. From an IT integration perspective, I expect enterprise customers to gravitate more toward a single security platform form factor because that allows for simplicity and reduced customization and overlap between security features. I believe this will allow organizations to manage their operational expenses better as less complexity allows for reduced overhead. I also expect a single platform solution to become the preferred method for cybersecurity departments, as it may reduce overall capital expenditure and reduce vendor exposure as a result. Customers who bring the Palo Alto suite of platforms achieve a 30-40% improvement in efficiency and better security scores as a result, management reported in its Q3 2024 earnings call. Management also recognized that customers using a single platform solution achieve a 10% reduction in security-related platform costs. The move to bring clients to a unified platform has increased meetings by 30%. Although it is still too early to say how successful this shift will be, I believe this strategy will catch on as IT departments become more sophisticated with the use of multiple cloud platforms combined with private data centers.

Given this move to platforms, management took the initiative to evaluate its entire customer base to target conversional sales towards its single and multi-platform solutions. Management noted in its Q3 2024 earnings report that among the top 5,000 customers, half had two or more platforms with 20% on Prisma Cloud and 40% on Cortex. The ARR for full platform clients falls much higher than existing clients at $2-14M for $200-800K. With the goal of bringing more customers to the full-spectrum platform model, management expects to achieve $15 billion in next-generation ARR by fiscal 2030 with more than 2,500 platform sales. In total, Palo Alto has 900 customers who converted with 65 added in 3Q24 alone.

In addition to its platform strategy, Palo Alto is actively launching new AI features across its platforms, including a basic and advanced co-pilot feature powered by Precision AI technology, which can help eliminate the complexity of security operations and can effectively improve productivity across departments. Cyber security. Their co-pilot feature is available on Strata, Prisma Cloud, and Cortex, and provides actionable insights, automation, and targeted actions for rapid response to security threats and for day-to-day security operations. I believe these co-pilot features will drive development of the platform since the offering uses natural language processing to streamline security operations and may allow for faster incident detection. These features may also be highly attractive to companies seeking to reduce operational expenses within their IT and security departments because they reduce the complexity of security operations and allow more breathing room in staffing departments.

Palo Alto Networks Partnerships

In addition to this tactic, Palo Alto has also partnered with IBM (IBM) to offer industry-specific capabilities on XSIAM using IBM watsonx. This partnership will enable IBM’s more than 1,000 security consultants to leverage the Palo Alto portfolio and has the potential to increase platform sales. The partnership has some moving parts, including the acquisition of IBM’s QRadar SaaS assets, QRadar IP, and IBM’s on-premises QRadar customer list. Total consideration for the deal is up to $500 million plus earnings. In return, Palo Alto will become IBM’s partner of choice for cybersecurity across the network, cloud and SOC, potentially driving business to Palo Alto’s security platform. IBM will also utilize Palo Alto products and integrate Watsonx into Cortex XSIAM to deliver Precision AI solutions, enhancing Palo Alto’s AI offerings. Once the deal closes, Palo Alto will transition QRadar customers to their XSIAM offering over the next few years and will begin generating revenue in fiscal year eFY25. Accordingly, management expects some decline in QRadar’s customer base, which brought in $100 million in SaaS revenue during FY23.

Palo Alto also expanded its strategic alliance with Accenture to combine Palo Alto’s Precision AI technology with Accenture’s secure GenAI services to help enhance AI security features. I believe this partnership will create more synergies between the two companies as companies seek to use GenAI more to automate and optimize business processes in a secure manner. The strategic partnership will be driven by Accenture’s comprehensive AI diagnostics services that will leverage Palo Alto’s Prisma Cloud AI Security Posture Management and AI Access Security to ensure the security posture of clients’ LLM/AI applications. Given the rate of transformation across GenAI applications, I believe this offering will see significant growth as GenAI opens the door to new threat vectors that could leave a sea of corporate data exposed. Given that organizations are working on a variety of on-premises, cloud, and hybrid solutions, I expect organizations will seek to secure their data before jumping into new GenAI solutions.

Palo Alto Networks Financials and Outlook

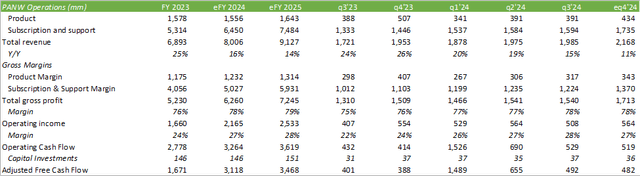

Palo Alto Networks reported 15% overall growth in Q3 2024, with 80% of sales coming from subscription and support services. This has resulted in margins strengthening year over year, with adjusted operating income improving from 23.6% in Q3 2023 to 25.6% in Q3 2024. Management expects FY24 operating margin to fall in the range of 26.8-27%. This is an improvement over the previous year’s operating margin of 24%.

Corporate reports

Looking ahead to FY25, I am adjusting my forecast as it relates to a slightly slower growth rate than initially expected. Although I expect Palo Alto to face some tailwinds as a result of selling its AI features across its security platforms, I expect some minor adjustments to the sales cycle as it adapts to the platform model.

Palo Alto Networks: Valuation and Shareholder Value

Corporate reports

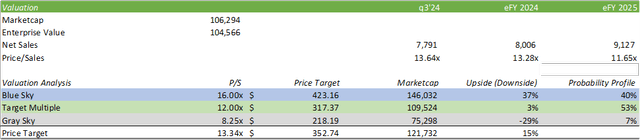

PANW shares are currently trading at 13.64x TTM price/sales. Comparing my current forecasts to my previously reported estimates, I will significantly lower my price target from $427 per share to $352.74 per share at 13.34x FY25 price/sales. The adjustment is primarily due to the more challenging sales environment and revised compositions due to the system Basic. As a result, I expect PANW shares to remain relatively restricted to the P/S range until the macro environment improves. Given the price decline resulting from Q2 2024 earnings, I believe investors can see modest upside in the stock’s value when considering the current price level. I reiterate my Buy recommendation with a price target of $352.74 per share.

Corporate reports