Maridav/iStock via Getty Images

Park Hotels and Resorts Company (New York Stock Exchange: BKFounded by Hilton Worldwide Holdings (HLT) in 2017 and headquartered in Tysons, Virginia, it owns and operates hotels and resorts in the United States.

Investors looking for Exposure to the US hotel sector might be interested in this REIT because it appears to be a good addition to a dividend portfolio given the industry outlook in 2024. Dividends are well covered, the business is conservatively funded offering strong liquidity, and the stock is trading at a discount slight of tangible book value, providing management practically free of charge.

Portfolio and outlook

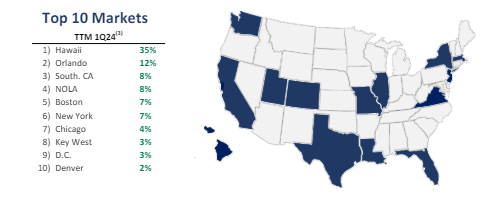

The REIT’s portfolio consists of 43 hotels totaling 26 rooms spread across 16 states, with the highest concentration in Hawaii and Orlando which together generate nearly half of its EBITDA:

Investor presentation

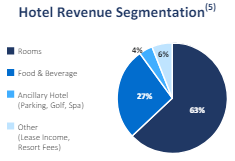

Its revenue comes primarily from room bookings, but it also generates a significant portion from food and beverage services and additional hotel offers:

Investor presentation

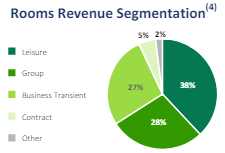

The business is further diversified by client type with a significant portion of revenue being generated through passing businesses and groups:

Investor presentation

Although there is a lot of reliance on the two-state solution, I do not think it represents a big risk. In January 2024, room demand in Hawaii reached 1.3 million hotel nights, an increase of 3.7% year over year. Room supply was 1.7 million room nights, just 0.1% higher than the same month a year earlier. Orlando, the most visited travel destination in the United States, is experiencing a rebound with RevPAR already posting some year-over-year growth in 2023 and expected to increase further as demand continues to grow and latitude remains limited.

However, the U.S. hotel industry as a whole faces several headwinds to RevPAR growth this year, based on CBRE. Also, in an economic downturn scenario, Park Hotels may be more impacted since most of its portfolio is upscale/luxury and RevPAR is more resilient when coming from mid-tier hotels because guests typically trade in lower rates.

performance

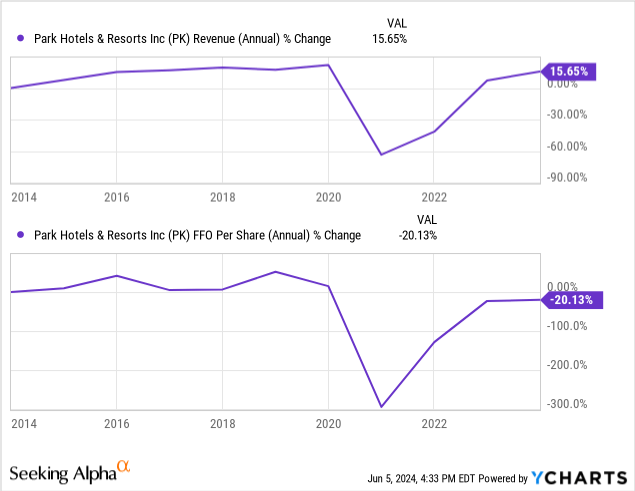

Looking at long-term operating performance, it’s clear that barring a hiccup during the pandemic, this is a stable business. However, growth was slow before that:

Of course, it’s been recovering since 2021, with revenue reaching and exceeding pre-pandemic levels and FFO per share on its way there.

Newer, more relevant KPIs highlight this recovery as well, with RevPAR last quarter at $178.25, 4.11% higher than in the same period last year. ADR also showed growth, rising 1.85% to $250.93. In 2023, revenue per available room and average room rate increased 8.7% and 1.3% year over year to $178.62 and $245.80, respectively.

Average daily rate growth that lags behind RevPAR growth indicates higher occupancy, and certainly the occupancy rate at Park Hotels rose from 67.8% in 2022 to 72.7% in 2023; This is also higher than the 63.6% average expected for U.S. hotels this year.

Q4 FFO was also 15.6% higher year over year at $0.52 per share. For 2023, FFO per share increased 32.5% to $2.04, indicating a significant impact of revenue recovery on the bottom line.

These trends appear set to continue as management has updated its guidance based on stronger-than-expected results in the first quarter of 2024. Specifically, adjusted EBITDA is expected to range from $655 million to $695 million, i.e. 10 million dollar. Increase midway. AFFO stock is also expected to rise about $0.05 at the midpoint to a new range of $2.07 to $2.27 per share. These changes represent year-over-year growth in EBITDA and AFFO per share of 2.5% and 6%, respectively.

Leverage and liquidity

In October 2023, Park Hotels strategically defaulted on a $725 million non-recourse loan secured by the two Hilton San Francisco hotels it owns. Subsequently, the REIT’s improved leverage led S&P Global to raise its credit rating from B to BB-.

Today, about 50% of its assets are financed through debt, and after adjusting the $725 million loan, Park Hotels has a debt-to-EBITDA ratio of 5.45 times. Its interest coverage of 2.8x (weighted average interest rate of 5.24%) and $378 million of liquid assets (4.16% of total assets) also highlight its strong liquidity.

Additionally, the REIT currently has access to a $950 million revolver that could be increased by up to $500 million; It matures on December 1, 2026 and has a one-year extension option. This allows the company to more easily handle upcoming mortgage maturities of approximately $1.5 billion in 2026, which represents 42.4% of debt. The amounts due in 2024 and 2025 are more manageable at 1.6% and 8.46% of the total debt, respectively.

It is also worth noting that the company recently redeemed 7,500% senior notes due 2025 for $650 million and issued 7,000% senior notes due 2030 for an aggregate aggregate amount of $550 million.

Dividends and Valuation

PK currently pays a quarterly dividend of $0.25 per share, resulting in a forward yield of 6.55%. With a payout ratio of 47.43% based on the latest quarterly AFFO report, this looks very attractive. The distribution record is what you’d expect from a hotel REIT, which was forced to suspend payouts after the pandemic hit and even ensure it could safely redistribute dividends:

Seeking alpha

But given the seasonal nature of hotel REITs, the trend, and the overall industry outlook, it’s justifiable to expect a higher return from the special dividend potential here.

The stock price also reflects good value. This is established by PK’s FFO multiple which is currently the lowest among its more relevant peers:

| stock | F/Effu |

| PK | 7.01 |

| Camel | 8.75 |

| what | 11.36 |

| D.R.H | 8.59 |

| middle | 8.92 |

The shares are also trading at a slight discount to tangible book value ($16.36) which is not justified given the outlook and the fact that you are not paying any premium to management. Speaking of this topic…

administration

We also need to note a few things about management before we get into risks. First, each of the directors and directors owns less than 1% of the common stock, and there have been no meaningful purchases of open market stock recently. However, this is offset in some ways by other useful indicators of management quality.

First, the highest compensation package in 2023 appears to be shareholder-friendly. The $10.8 million CEO compensation package in 2023 seems reasonable given both its operating results and that it represents only 1.44% of net cash income generated in 2023. Furthermore, Park Hotels has a history of consistently generating capital gains from real estate dispositions since In 2017 when she broke up. Finally, in 2023, the board approved a stock buyback program that allows the company to buy back $300 million through February 2025, and over the past year, it has repurchased $180 million worth of stock.

Also given the prospect of lowering the cost of debt, deleveraging, and continuing to buy properties at good prices, I believe management can continue to deliver shareholder value beyond dividend payments.

Risks

However, there are some risks that we need to highlight. First, we already mentioned that an economic slowdown can impact the performance of properties more because they are upscale/luxury; As a result, the REIT may not achieve its objectives, posing a significant risk to shareholders. This also creates a risk to the dividend as the company may choose to suspend or reduce.

Although Hawaii and Orlando are clearly good markets to focus on, there is still risk here if certain events make travel to those destinations less attractive in the future. Even if such potential events do not impact a REIT’s bottom line in hindsight, they nonetheless pose a major risk and may lead to increased selling pressure.

I also find the opportunity risk present here worth mentioning because the stock price has risen significantly since its 2023 low of around $11. Shares traded near TBV even in 2020 before the pandemic, so there’s no reason to believe that current risks are what prevents the market from assigning a premium to tangible book value; Trading near TBV seems normal for this REIT even when profitable. Investors should at least gauge whether the potential gains they can realize from dividends are worth the potential opportunity cost.

Judgment

However, I think the expectations outweigh the risks here. This is a conservatively funded, undervalued REIT that should trade closer to where its peers are these days based on FFO while taking into account portfolio quality, revenue diversification, and overall positive outlook for the Hawaii and Orlando markets. Therefore, I evaluate PK a He buys.

what do you think? Do you own this REIT or intend to? Let me know and I will get back to you soon. Please also leave a comment if you found this post helpful; It means a lot! thank you for reading.