andresr/E+ via Getty Images

thesis

B3 Health Partners (Nasdaq:BI) works in the health care field, where it partners with health care providers in different states in five states, and provides them with assistance in obtaining compensation.

It was P3 revenue It has grown steadily over the past years from $452 million to $1.5 billion, but it has not been profitable yet. However, profitability in 2024 is on the doorstep given the company’s guidance, and once profit is achieved, I think the company’s valuation should start to look very different. Perhaps for this reason, the P3 rating according to all Seeking Alpha metrics is A+. With an EV/sales of 0.31, I think P3 is undervalued.

The recent announcement of a new CEO could lead to renewed interest in the stock.

As the company moves toward its guiding goal of profitability, so do I The company is rated as Buy.

a company

introduction

P3 operates in the healthcare service, working with healthcare companies as members with the aim of creating added value. P3 has a team of physicians and healthcare providers with a variety of healthcare management services, such as patient and physician education, patient management, proactive screening, and resource access.

A quick look at the P3 slide (Jefferies’ recent presentation) Growth File (Needham’s last show)

P3 has a network of providers across the country, who manage the care of thousands of patients, by providing coordination and administrative services that lead to better patient outcomes and reduced costs, taking care of patient care, hospital visits and related services. P3 uses local doctors to partly provide these services. P3 charges a per-member monthly fee (PMPM) and medical providers get a percentage of the money not spent on member care and an additional bonus.

P3 is active in five states and 23 markets.

The path to profitability in 2024

P3’s market cap currently stands at $183 million, which is grossly out of proportion to its recent quarterly revenue of $388.5 million and expected annual revenue of between $1.45 and $1.55 billion. Moreover, these revenues continue to grow year after year, while the stock price continues to decline, adding to the disproportionality.

One could argue that perhaps the valuation is low because the company will never be able to make a profit. These arguments fail in light of the company’s repeated guidance that 2024 will be profitable, with an estimated EBITDA margin of $20 million to $40 million. While the company typically does not provide guidance on potential earnings, the fact that it does is an indication that the outlook is good. If this trend continues, the profit margin could grow rapidly over the coming years. There’s a lot of scope, as $20 million to $40 million represents only a small portion of the company’s projected revenue of $1.5 billion, which is expected to continue to increase year over year.

Medical Margin and EBITDA Guidance (Recent Needham Presentation)

P3 reaffirmed profitability guidance in its Q4 2023 earnings call and did so again when releasing Q1 2024 results.

Factors behind the path to profitability

There are several elements that play in favor of the P3 guidance here, and I will mention some of them below. Over the past five years, while memberships have increased by 155%, revenues have increased by 209%. Since revenues are expected to reach between $1.45 and $1.55 billion at the end of 2024, this corresponds to approximately 14% to 19% growth through 2023.

As annual membership registration numbers continue to improve, P3 also continues to expand into new territories. The company currently operates in 25 countries, two more countries than at the beginning of 2024.

Revenue growth is also consistent every year. In 2023, total revenue growth compared to the previous year was 21%. In the first quarter of 2024, revenue growth compared to the first quarter of 2023 was 29%.

Existing members continue to pay more, 16% compared to the previous year in 2023, despite the decline in repayments.

P3 has made some cost reductions and other operational efficiency improvements, such as reducing its platform expenses by 32% in 2023.

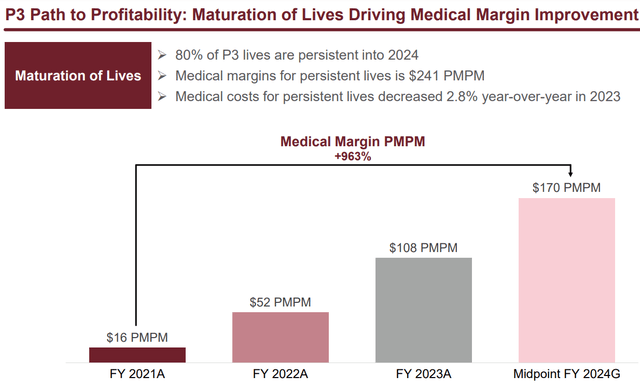

Additionally, P3 expects the maturity of life to improve medical margins.

Life Maturity Slice (Needham’s Final Presentation)

Latest quarterly results

The first quarter of each year is generally not a large contributor to annual revenue.

However, in its most recent quarterly results for Q1 2024, P3 noted overall revenue growth of 29% year over year. Total revenue for the quarter was $388.5 million, an increase of 29% compared to $302.1 million in the prior year’s first quarter.

The net loss and EBITDA loss were similar year-over-year, but with revenue up 29% compared to the prior year, the net loss and EBITDA loss are actually an improvement over the prior year, or a relative decline of about 30% compared to In the previous year. last year.

The net loss was $49.6 million, compared to a net loss of $52.4 million in the first quarter of the previous year. Adjusted EBITDA loss was $19.8 million, compared to Adjusted EBITDA loss of $19.1 million in the prior-year quarter.

This relative annual decline in losses as a function of total revenues may be due to several reasons, such as a 26% decrease in operating expenses to $26.2 million for the first quarter of 2024, a 12% decrease in medical expenses, and a 12% decrease in medical expenses. Reducing institutional, general and administrative expenses. If these operational efficiencies continue, I believe the company’s guidance could be correct. In addition, P3 expects to see a significant reserve release, as 2023 claims have shown a trend of strong improvement from what was previously reserved.

P3 guidance for profitability in 2024 ranges from $20 to $40 on an adjusted EBITDA basis.

Transition to Profitability Slide (Needham Presentation)

In my view, neither the company’s projected revenue of $1.5 billion nor its expected trajectory warrant a market capitalization of less than $200 million.

The average price target of Wall Street analysts is 386% higher than the current valuation.

Wall Street Analysts Average Target (Seeking Alpha)

PIII’s Alpha rating is A+. In fact, all available metrics are A+.

Rating scales (seeking alpha)

Given its lack of profitability, I would primarily look at this company by its EV-to-sales ratio. For PIII, this value is around 0.3, while companies generally trade around EV/sales ratios of 1 to 3. The company looks significantly undervalued from this perspective, and certainly in light of its guidance.

New CEO on board

In May 2024, P3 announced that Aric Hoffman would join P3 as the new CEO, while the previous CEO would remain as an advisor and member of the board of directors. Mr. Hoffman knows the P3 team well, having worked for the company in the past, before moving on to serve as CEO of Everett Clinic and Northwest Physicians Network.

His return to the company and the people he already knows, who have more experience as CEO, could bring added value and fresh wind to the company. This could also be good news for investors, allowing the company to turn the page.

financial affairs

According to P3’s most recent quarterly results, the company had approximately $32 million in cash and received approximately $15 million in regular cash installments and an additional $15 million in equity capital at the beginning of the second quarter.

The company recently raised nearly $42 million from a private placement at a price of 0.62 cents. In total, this should result in about $100 million in cash, which could be enough if the company actually becomes profitable.

Recent financing at a higher rate than the current rate reduces the risk of further financing.

Furthermore, last year’s financing was also a private placement at $1.12, so I assume investors in this financing will be reluctant to sell at current prices.

Finally, short interest in PIII is around 7% with around 18 days to cover current volume.

Risks

Investing in a company that is not yet generating revenue is risky. The company may need more financing, thus diluting existing shareholders and increasing market value. I think the risks, at the moment, are limited given the recent financing.

The profitability thesis as projected by the company may be affected by regulatory or macroeconomic factors, and may simply appear wrong, or it may take the company longer to reach that pivot point. A positive market reaction in case of profitability is not guaranteed.

The price of P3 is below the dollar at the moment, which means it does not meet Nasdaq requirements. If this situation continues, P3 may eventually have to take measures to ensure compliance, such as a reverse stock split.

Finally, despite its high revenues, PIII’s valuation is low, making it qualify as a small-cap company. Investing in small cap stocks is always risky.

Conclusion

P3 is a healthcare player with a growing business on its way to profitability.

With the recent closing of the financing, I think now may be a good time to consider a potential investment in P3 Health Partners. P3’s revenues have continued to grow over the past several years, and the guidance is that revenues will ultimately be between $1.45 and $1.55 billion this year. These revenues stand in stark contrast to the company’s market capitalization, which is less than $200 million. It also contrasts with an EV/sales ratio of about 0.3, which contrasts with EV/sales ratios that typically range between 1 and 3. The average price target of Wall Street analysts shows an upside of 386%.

PIII’s cost structure recently became more lenient over the past quarter.

For the above reasons and because the company believes 2024 will be transformative, I believe now is a good time to cover PIII with a Buy rating.

Editor’s Note: This article discusses one or more small-cap stocks. Please be aware of the risks associated with these stocks.