Evening pictures

Investment summary

My previous investment thoughts (published in February of this year) were a Buy rating because I thought Paycor HCM (Nasdaq:Baker) will be able to beat its FY24 guidance given its rebounding demand and positive momentum Moving up, this would lead to a positive rating. I lowered my rating from Buy to Hold because I no longer believe PYCR can grow at the rates I previously modeled. The difficult macro backdrop and slowdown in employee hiring will put pressure on growth.

Third quarter results update 24

PYCR, which was released 3 weeks ago, reported a disappointing 14.1% revenue growth to $187 million, a decline of 370 basis points versus 17.8% year-over-year growth in Q2 2024. This is a major disappointment. Because I thought Q2 2024 was the beginning of the recovery as growth in Q2 2024 accelerated by 160 basis points versus Q1 2024. However, EBIT came as a surprise, improving from 14.6% in 2019 Q2 24 to 25.5% in Q3 24. This was an outperformance compared to the consensus forecast of $45.72 million (PYCR reported $47.73 million). As for guidance, management revised recurring and other revenue growth downward from the previous midpoint of US$653 million to US$651 million, implying a downgrade of the growth rating by 30 basis points (from 18.1% to 17.8%).

I was very early in identifying recovery.

I made a big mistake when I assumed that the strength of the second quarter of 2024 was the beginning of the recovery. It appears that overall conditions have worsened, and PYCR will not escape unscathed. After reviewing my thoughts on US macroeconomics, I believe interest rates will remain high for much longer, and will continue to be a drag on PYCR growth going forward (i.e. growth is unlikely to recover back to above 20% any time soon). The three main factors that I believe will prevent the Fed from cutting interest rates aggressively are: (1) inflation rates remain steady; (2) The problem of housing shortages in the United States is not going away any time soon, which means that lowering interest rates will only exacerbate the problem (increasing demand for housing as a result of lower mortgage rates, which leads to higher CPI ); (3) There is no good reason for the Fed to cut interest rates as the US economy appears to continue to strengthen.

The effect of rates staying higher for longer is that businesses will continue to face higher capital costs, limiting their budget for growing the business – in this case, hiring new employees. This has a direct impact on PYCR because part of its growth equation is the number of employees at the company using its product. PCYR is already feeling this pain as same-store sales growth continues to decelerate, contributing less than 50 basis points of revenue growth in 3Q24, and in particular, management has explicitly indicated that this weakness persists and will likely get worse.

Slowing headcount growth indicates slow growth in the future

There’s another issue with PYCR that I think will put a cap on how quickly the top line can grow – which is the slowdown in headcount growth. Management commented that they had made structural changes to parts of their sales team, and this had resulted in a high sales rep turnover rate, but they Won’t hire Returns these missing numbers. At the TMC conference organized by JP Morgan, they stated that headcount growth will end up in the low to mid-teens range, which is below their target growth of 20%. The important point to note is that they expect this trend of slower employment growth to continue unless there are macroeconomic changes, such as lower interest rates.

I mean we’ve seen just as others have seen and as you can see in the broader market, same source sales have seen a consistent downward trend for a while now. Recently, we have seen more early signs of potential negative growth. Q3 24 earnings call

Management’s rationale for not ramping up hiring is that they believe they can grow more than 20% with fewer employees. Although this may be true, I have learned a lesson not to be overly confident in forecasting a recovery unless there is strong evidence (proven over a few quarters). Until that evidence emerges, my view on this slowdown in hiring is that it shows that management is not confident enough that there is enough demand to justify hiring. Remember, it takes a typical salesperson 36 months (according to the JP Morgan TMC Conference) before they reach maturity. Not hiring today means that management is not confident about the outlook in the near term (less than one year) to medium term (more than one year but less than two years).

Redfox Capital Ideas

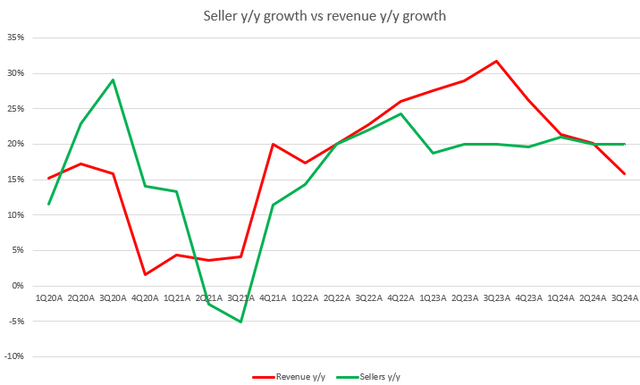

Moreover, looking at PYCR’s historical data, this is also a negative indicator for revenue growth. By plotting the annual growth in the number of sellers, we can see that there is a close relationship with the annual growth of PYCR, at least trendily. Hence, with PYCR’s headcount growth slowing now, I think a very clear data point is that growth is not going back to more than 20% anytime soon. I also repeat that it takes 3 years for new sellers to fully mature, this also means that the growth in the medium term will not be significant.

evaluation

Redfox Capital Ideas

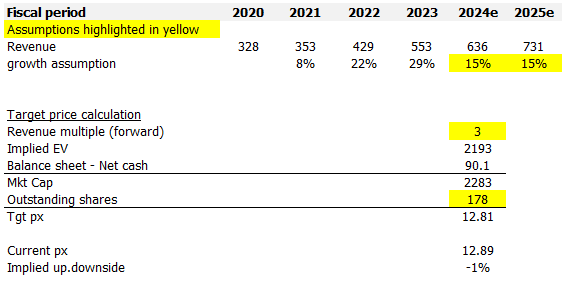

Given my renewed view of PYCR’s growth prospects, I no longer believe this is an attractive investment. I model the PYCR using the forward revenue approach, and using my assumptions, I think the value of the PYCR is around $13. I no longer believe that PYCR can recover more than 20% in the next two years. Instead, I am inclined to believe that growth will see a mid-20 year growth rate, given the macro backdrop and the slowdown in hiring. Lower growth expectations also mean that PYCR deserves a lower valuation. While PYCR is trading at a discount (PYCR at 3x vs. 4x to 5x peers) compared to other HCM and payment peers like Workday, Paylocity Holdings, Dayforce, and Paycom Software despite having similar growth outlook (mid-teens) I don’t think there is a catalyst To fill this gap. As such, I assume that PYCR will continue to trade at this current valuation.

risk

If the economy recovers and management decides to capitalize on that recovery by accelerating vendor hiring, this could push growth back to >20% earlier than I would expect. This would change the entire narrative around the PYCR, as the growth outlook is much better than the current ratio in the mid-teens. I wouldn’t be surprised to see valuations rise to the levels of its peers.

Conclusion

My view of PCYR is a hold rating. I was wrong to think there was a shift in place. I now believe that a tougher macroeconomic environment, especially a longer duration of higher interest rates, will continue to impact PYCR’s client base. In addition, PYCR’s slowdown in headcount growth indicates a lack of confidence in demand in the near and medium term. While PYCR is trading at a discount compared to its peers, I don’t see catalysts to close the valuation gap in light of the revised growth outlook.