Justin Sullivan

My first article on Searching for Alpha appeared on PayPal (Nasdaq: BPL), a company that is priced in the market as if it will not grow at all over the next ten years. At the time, PayPal was trading at $60 per share I haven’t done much since then, but was I wrong in my assessment? There have been two quarterly reports since then, and PayPal is actually still growing across all KPIs. In this article, I will revisit the thesis, expand on my ideas, and draw a conclusion.

Any growth equals less than its true value, which is the strongest investment thesis

The investment thesis for PayPal is simple, straightforward, and easy to understand: If PayPal grows at all, it means it’s currently undervalued. That’s it, it’s that simple. It is a powerful thesis and very rare in my opinion. This is because the company is trading at a price A level that means it will not grow over the next 10 years, and by no growth, I mean 0%.

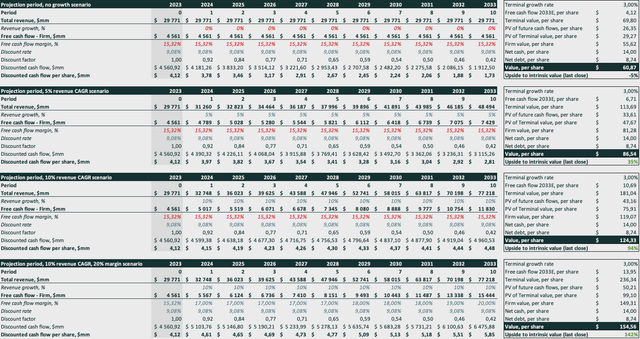

To test this, we can implement a reversible discounted cash flow (DCF) model. I took the 2023 results and extrapolated them, and 2023 was a weak year in terms of free cash flow margin, which strengthens the hypothesis further because it creates a margin of safety by making the base period weak.

Amir Mulhalilovic, PayPal filings with the Securities and Exchange Commission

In the image above, I modeled 4 different scenarios: one where PayPal doesn’t grow its revenue or margin for 10 years, one where revenue grows at a 5% compound annual growth rate (CAGR), one where revenue grows at a 10% CAGR, and the The fourth is where margin and revenue grow. They all use the same assumptions of 3% terminal growth and a discount rate of 9.08%, which is the sum of the US market implied equity risk premium (Source: Aswath Damodaran) and the risk-free rate. Here are the summaries:

| Scenario | Intrinsic value |

| There is no growth | $61 per share |

| 5% CAGR of revenue | $87 per share |

| 10% CAGR of revenue | $124 per share |

| Revenue CAGR of 10% and free cash flow margin of 17% | $155 per share |

Through the inverse DCF scenarios, we can see that the intrinsic value product, where there is no growth of assumptions, is where PayPal currently trades. The only caveat here is that PayPal is actually growing, which shows us just how abnormal current trading levels are. PayPal reported stronger adjusted FCF margins in Q1 2024 (16.37%) than Q4 2023 (15.25%), which was the holiday quarter and historically the strongest margin quarter for PayPal. While it may be too early to tell whether PayPal under new management will thrive and expand, we can at least conclude that PayPal is not significantly weakened.

PayPal’s intrinsic value is approximately $110 using a weighted average cost of capital of 11% and terminal growth rate assumptions of 2%. This model was presented in my previous article and works to grow free cash flow at a CAGR of 12.87% through revenue growth of approximately 10% and by expanding margins from approximately 17% to 20% by 2033.

In short, investors have a large margin of safety by buying into the current trading range, which means there is currently no growth for the next 10 years. However, if PayPal can grow revenues during this period, expand margins, or even both, there will be significant upside to the intrinsic value. The only risk we face is if PayPal loses revenue or its FCF margins fall significantly, which seems unlikely to me for several reasons.

Why the market might be wrong

So why is the market pricing PayPal this way? One common argument is that the payments industry is a race to the bottom, meaning there are too many competitors vying for the same dollar. There is no shortage of payment solutions. Bears are quick to point out that Apple Pay, Google Pay, Stripe, and Adyen are coming to PayPal’s lunch.

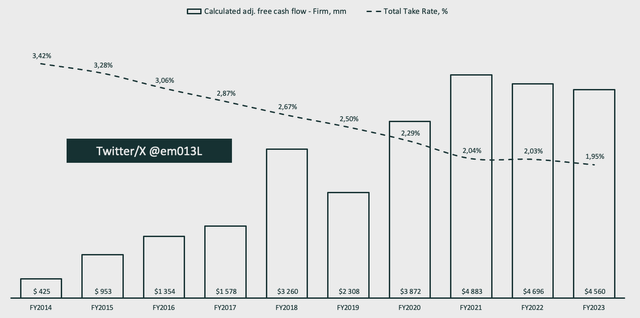

The following chart shows the time period in which all of the above competitors were launched. While competition may have eroded the take rate, free cash flow has been steadily increasing.

Amir Mulhalilovic, PayPal’s SEC filings

It may seem alarming to see that free cash flow has been trending downward over the past couple of years, but it’s worth noting that 2021 and parts of 2022 saw a significant increase in the number of consumers transacting online, attributable to the pandemic. The 5-year free cash flow margin is approximately 17% on an adjusted basis, where EBIT is adjusted for stock-based compensation, restructuring expenses, and amortization of intangible assets. This is 200 basis points higher compared to our inverse DCF assumption of 15%, creating more margins of safety for us as investors.

Among the most important questions that we must ask ourselves regarding the thesis are:

- Is PayPal losing market share to its competitors?

- Is PayPal growing?

Remember, the market is implying that PayPal will not have any growth in the future. So, for our thesis to have some merit, we have to find evidence of PayPal’s growth. In fact, PayPal is gaining market share despite intense competition.

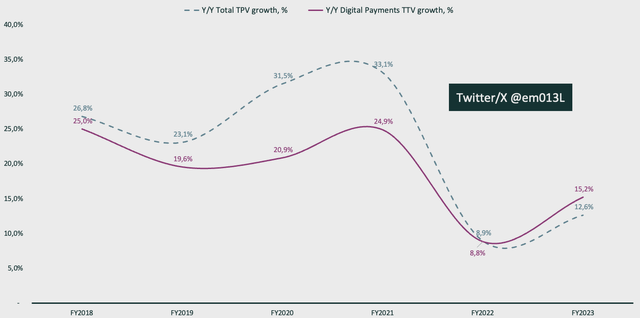

We can come to some conclusions by looking at the volume of digital payments transactions around the world (source: Statista) and comparing it to PayPal’s Total Payment Volume (TPV).

Amir Mulahalilovich, Statista, PayPal SEC filings

During the 2018-2023 periods, PayPal TPV grew at a CAGR of 22.3%, while digital payments worldwide grew at a CAGR of 18.9%. This means that PayPal has gained market share in the digital payments space, while operating among a large number of competitors.

Even if PayPal loses market share in the coming years, it wouldn’t break our thesis. Remember, PayPal is currently priced at zero stock market growth, while we have evidence of growth faster than or on par with the global digital payments market. If PayPal grows at all in the next 10 years, it is currently undervalued. For our thesis to be invalidated, PayPal would have to significantly reduce its market share and have negative results over the next 10 years, something the data does not currently support.

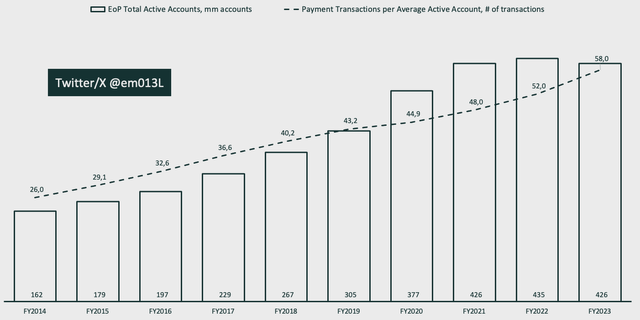

Another angle that the bears are looking at that could indicate that PayPal is on the decline is the decline in the total number of active accounts from fiscal year 2022 to 2023. Management has been talking about this for several quarters, pointing to the increase in poor quality accounts that have resulted in About the previous campaign run by PayPal. These were primarily based in Latin America. The counterargument to this is the fact that active accounts are transacting more on average, a trend that has only been positive since the company went public. As an investor in the company, this is quite a positive thing: PayPal maintains high-quality accounts while producing low-quality ones; The accounts that remain use PayPal more with each passing year.

Amir Mulhalovic, PayPal’s SEC filings

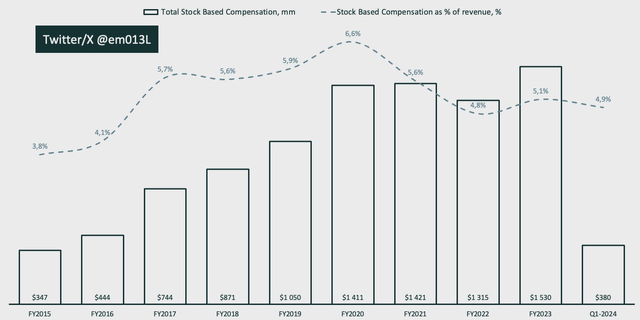

Aside from the two main arguments regarding active accounts and take rate, stock-based compensation (SBC) exists in the background as a negative aspect of the business. To me, SBC is not outrageous in PayPal. It’s more or less in line with its peers and has been pretty steady at around 5% for the better part of a decade. We also know that the administration is reducing the Small Business SBC and will instead increase cash compensation going forward.

Amir Mulhalilovic, PayPal’s SEC filings

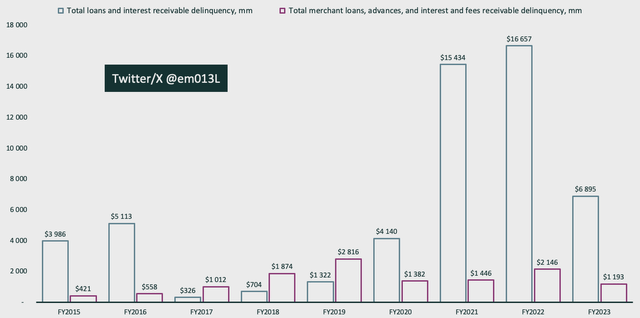

Another minor issue that PayPal faces is the balance sheet risks the company has taken on during the fallout from the pandemic. The risk of deviation for consumers and merchants has been greatly reduced and, in my opinion, is under control.

Amir Mulhalovic, PayPal’s SEC filings

Summary The carrot to be patient

The investment thesis is very simple and straightforward, as PayPal is currently undervalued if the company grows at all in the future. The company is currently priced as if it will not grow FCF over the next 10 years, which we can infer by simulating an inverse DCF model with 0% growth assumptions. However, the company is, in fact, growing and gaining market share in the global digital payments space while facing competition from companies like Apple, Adyen, and Stripe.

The original investment thesis is sound and sound, even though the stock price does not reflect it, and as such, we have an asymmetric opportunity with PayPal. There are several hints that investors can point to as evidence of PayPal’s continued growth in the future. Additionally, the arguments for PayPal’s demise can be deconstructed. PayPal is seeing FCF margin expansions on a quarterly basis as of Q1 2024, which is a very impressive feat considering Q4 is historically its strongest quarter due to holiday shopping. For this hypothesis to be invalidated, PayPal would need to see significant declines in FCF margins and negative revenue growth.

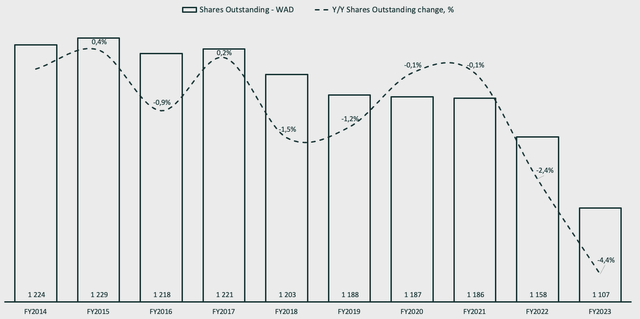

Another reason I feel comfortable waiting for PayPal to become somewhat more valuable is the fact that PayPal has been aggressively buying back stock. The company takes advantage of the suppressed (and unfair, in my opinion) stock price and returns shareholder value through buybacks. The company is committing most of its cash to this end, and I expect that will continue while the stock is undervalued. Until the stock reflects reality, PayPal remains a solid buy and one of the best opportunities in the market.

Amir Mulhalilovic, PayPal’s SEC filings