microstockhub

People’s Bancorp (Nasdaq: Bebo) is a bank with a history of more than 100 years and is headquartered in Marietta, Ohio. In terms of size, it is very small. In fact, its total assets do not exceed the threshold of $10 billion, but it proves that it is Great bank. High interest rates have been a challenge for many banks, but not PEBO, which is performing better than its peers.

Of course, the typical issues of high deposit costs and declining profitability are also present here, but the magnitude of these problems is relatively low.

Outperforming their peers

Peoples Bancorp Inc. (PEBO) Q1 2024 earnings call

These slides refer to the annual report and not to the first quarter of 2024, but they remain reliable as a single quarter cannot distort this ranking.

As you can see, PEBO’s net interest margin is the highest among its peers at At least 100 basis points above the average for the group under consideration. This is not a small gap, and is mainly due to the ability of this bank to finance itself at a relatively low cost.

Peoples Bancorp Inc. (PEBO) Q1 2024 earnings call

The cost of deposits is lower than the average of its peers, allowing the bank to get a better spread on an individual investment at the same rate.

Peoples Bancorp Inc. (PEBO) Q1 2024 earnings call

To be sure, Bebo Bank is also seeing a constant shift in capital from non-interest-bearing deposits to interest-bearing deposits, but the fact that the latter is still cheaper than average means it does not significantly impact profitability. In addition, non-interest bearing deposits, although declining, still constitute 22% of total deposits.

According to management forecasts, this trend is likely to continue if there is no interest rate cut, but the estimated range for the net interest margin in 2024 remains high, from 4.10% to 4.30%. There is strong optimism about this estimate that it will not be revised downward, partly because its balance sheet is relatively neutral. Therefore, if interest rates are raised or lowered by 75 basis points in the next few meetings, the impact on profitability will be minimal.

Beyond the moderate cost of financing, PEBO has sufficient liquidity to take advantage of current market opportunities. While some of their peers have a strict financial structure due to a loan-to-deposit ratio of over 100%, in the case of PEBO it is only 84.70%.

Peoples Bancorp Inc. (PEBO) Q1 2024 earnings call

The growth prospects in 2024 are there, and are mainly related to the sectors that achieved the greatest growth in the first quarter: premium finance, C&I, and CRE.

We have seen good growth, and we expect to continue to see good growth in our national premium financing business. And then on the C&I and CRE side, we continue to get again that broad-based market in Louisville, Lexington, Washington, D.C., Columbus, Cleveland, Cincinnati, et cetera.

CEO Tyler Wilcox, Q1 2024 conference call

In particular, the expected growth in total loans in 2024 is expected to be between 6% and 8% compared to 2023. While increasing commercial real estate loans in such a difficult period where commercial real estate is struggling to rise, the bank has managed The company handles this market well.

Peoples Bancorp Inc. (PEBO) Q1 2024 earnings call

Compared to its peers, PEBO has a CRE concentration risk well below the 300% threshold, and below the average of its peers.

Earnings analysis

PEBO’s current dividend yield is 5.37%, which is well above the industry average of 3.30%.

Seeking alpha

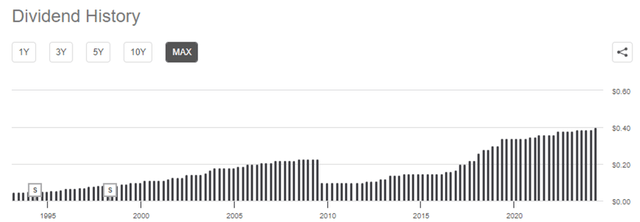

As you can see from this image, PEBO’s dividend history is quite controversial. Dividends almost always rise from the previous year, but in the event of a major recession, there is a risk of losing 10 years of progress with the cut. As for its growth in detail, there are other considerations that must be made.

Seeking alpha

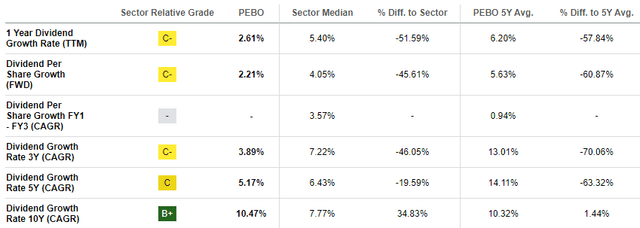

The stock’s 10-year dividend growth rate was 10.47%, much higher than its peers. However, the closer we get to the present, the lower the growth: over 5 years it was half, and over 3 years, it was only 3.89%.

What we can see from this data is that after the 2008 financial crisis and the sovereign debt crisis in Europe, when major central banks implemented highly expansionary monetary policy, PEBO increased dividends significantly from year to year. Subsequently, as macroeconomic conditions worsen, growth declines.

This phenomenon is evident in many banks, they are ultimately a cyclical business, but in the case of PEBO Bank, I think it is even more pronounced. Compared to last year, profits increased by only 2.21%, showing some doubts about the future growth rate. In any case, at least for the time being, its sustainability is out of the question.

The bank is well capitalized (Tier 1 common stock is 11.69%), and its dividend payout ratio is just under 50%, so there is no reason to expect any cut.

Peoples Bancorp Inc. (PEBO) Q1 2024 earnings call

In my opinion, I believe management is voluntarily giving less weight to dividends at this time, as it is more important to maintain a high degree of capitalization in the current macroeconomic environment. By the way, I remind you that unrealized losses on securities of AFS and HTM amount to 226 million US dollars, and equity is a little more than 1 billion US dollars. This means that the growth potential of TBV per share is stunted by unrealized losses, which is why capital preservation may be the best solution at this point.

Increasing the size of the total value per share is more important than the dividend, as it is the main driver of long-term share price growth.

Conclusion

PEBO is a strong bank, with a lower cost of deposits and a higher net interest margin than its peers. Loan growth prospects are good, while earnings growth prospects are rather weak: I doubt they are equal to the historical average of the past 10 years.

Overall, its financial stability combined with the current economic rating makes this bank a buy.

Seeking alpha

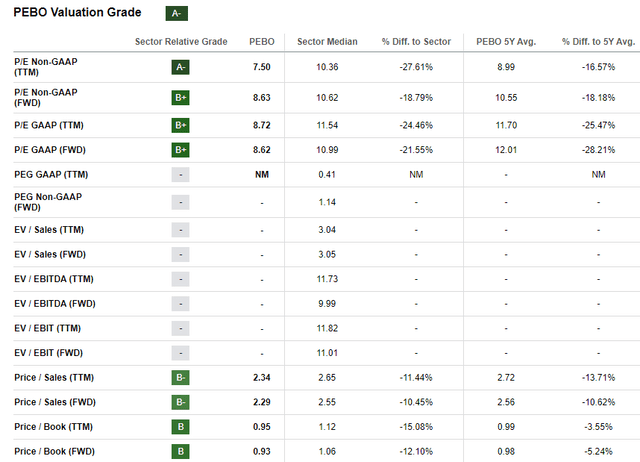

Both its P/E and P/B are lower than their peers and historical values, although their growth prospects are good. In the short to medium term, I expect good performance, but the same cannot be said from a long-term perspective.

Peoples Bancorp Inc. (PEBO) Q1 2024 earnings call

In terms of total return, PEBO has outperformed its peers over the past three and five years, but has consistently underperformed the S&P 500.

Before investing in this bank, you need to carefully evaluate your opportunity cost, as a simple solution like investing in the S&P 500 is likely to give you higher returns in the long run. However, not everyone has the same goals, and for those looking for a high, sustainable dividend yield in the short term, PEBO appears to be a viable option.