JHVEphoto

Pfizer (New York Stock Exchange: BFI) (New:PFE:CA) was not one of the favorite biopharmaceutical plays due to an unsustainable Covid push, which led to a period of declining sales. It seems that the stock has reached the bottom and can rise from it Bird flu fears, although the company is now largely focused on cutting costs. for me Investment thesis Now a little bullish on the stock due to the cheap valuation.

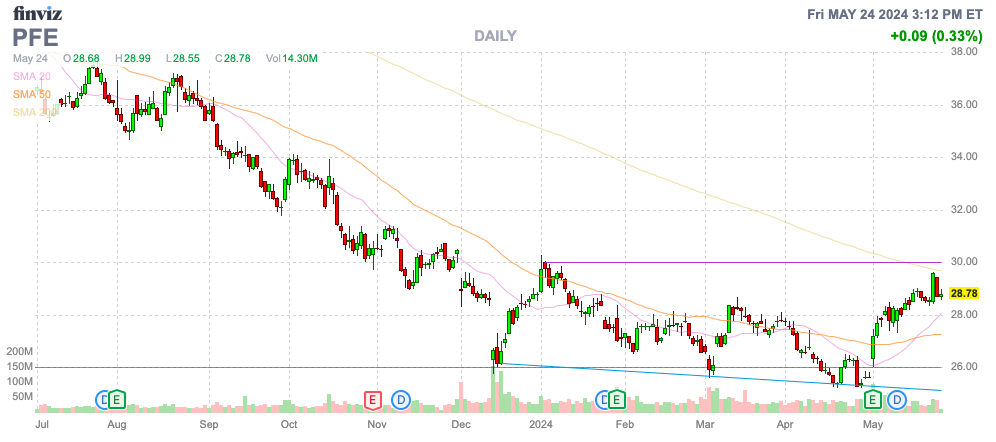

Source: Finviz

Hit the bottom

The key to the investment story is removing the additional downside risk from Covid sales. Pfizer reported first-quarter 2024 revenue of $14.9 billion, with Covid sales of more than $2 billion and revenue growth of 11% outside of Comirnaty and Paxlovid.

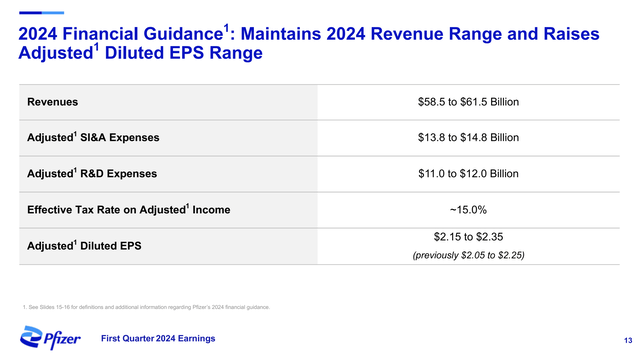

Pfizer still expects 2024 revenue to range between $58.5 to $61.5 billion. The sales target includes approximately $8 billion in projected revenue for Commernaty and Baxloved (about $5 billion and $3 billion, respectively), and approximately $3.1 billion In expected revenues from sales of older Seagen drugs.

Source: Pfizer Q1’24 presentation

Coronavirus-related sales are now targeting less than 15% of total revenue, reducing downside risks going forward. At the beginning of the year, Pfizer targeted $21.5 billion in Covid sales, resulting in total revenues of more than $70 billion.

The Covid drug market is likely to be fairly stable at current levels Moderna (MRNA) highlights a market where US coronavirus vaccination rates for the fall 2023 season were just 11%, well below the 44% flu vaccination rate, while hospitalizations for Covid were higher than for influenza and respiratory syncytial virus. .

Source: Moderna Q1 2024 presentation

The opportunity certainly exists for Pfizer to build on annual Covid vaccine sales now targeted at $8 billion in 2024. The general public has certainly lost confidence in untested vaccines, but demand will likely always be there among at-risk populations.

The biopharma company has promising drugs in oncology and respiratory syncytial virus, paving a path for growth away from any impact from Covid in the future. Pfizer may actually get a boost from Covid vaccine sales, considering the ongoing flu vaccination rate is much higher.

Pfizer is in the midst of cutting $4 billion in annual costs, representing 7% of sales. Given these stable revenues and cost reductions, the biopharmaceutical company recently raised its EPS target for the year by $0.10 to $2.25, at the midpoint.

Also remember that EPS took a loss of $0.40 from the financial costs of the Seagen deal. Analysts expect 2025 earnings per share to jump to $2.73, partly due to reducing those costs and expectations for future sales growth.

Bird flu promotion

Recent news has Pfizer and Moderna (MRNA) is working with the US Department of Health and Human Services on a potential vaccine program targeting the H5N1 virus. The government has already converted its stockpile of 4.8 million doses into bird flu shots.

The big question is how willing the public will be to take another untested vaccine from messenger RNA (mRNA)-based vaccine manufacturers. Despite persistent Covid infections, most patients in the United States are hesitant to take vaccines, with the number of doses in the 2023-2024 season falling to an estimated just over 40 million.

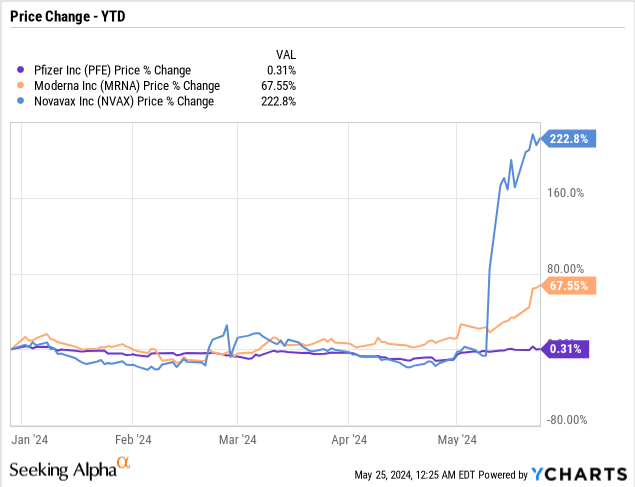

For various reasons, stocks of other Covid vaccines have actually risen this year. Novavax (NVAX) signed a joint marketing agreement with Sanofi (SNY) to supply vaccines, while Moderna jumped on excitement about its pipeline and the opportunity to boost its bird flu vaccine.

So far, Pfizer stock has held steady year over year, while Moderna stock is up 68%. Given Pfizer’s size, the biopharma company won’t get the same boost from another one-time vaccine event, but the market seems to have forgotten about the pharmaceutical company.

The stock is only trading slightly above 10 times its normalized EPS targets for 2025. Pfizer is starting to present better risk/reward scenarios and the chart is more bullish on the dips as Pfizer gets closer to hitting the bottom.

The biopharmaceutical company has significant net debt of $59 billion, due in part to the closing of the Seagen deal. The company pays a solid 5.8% dividend yield, providing a solid yield, while investors wait for the stock to rise.

The opportunity is clear to stimulate a Covid sales recovery in the 2024-2025 season, coupled with additional bird flu demand from the US government. Furthermore, the stock may be due for a speculative rally following Novavax and Moderna’s recent moves as the market becomes more bullish on battered Covid vaccine stocks after a tough few years.

Away

The main take away from investors is that Pfizer appears to have hit bottom. The biopharma industry may finally see some tailwinds to Covid drug sales while the rest of the business returns to growth mode from the Seagen deal. The bird flu outbreak may provide another catalyst for stocks.

Investors should use any declines in Pfizer to load the stock with 10x forward EPS targets with just a ~6% dividend yield to reward investors waiting for the biopharma industry to turn the corner.