Domo/iStock via Getty Images

Investment thesis

Play Studios (Nasdaq: MBS) underwent a successful restructuring during 2023 which was aimed at simplifying the organization and reducing costs. Since then, the company has significantly improved its profitability, at the expense of increasing its revenues. After failing to reignite organic growth Post Covid-19, this year promises to be the year the company shows growth in both its bottom line and revenue. Furthermore, the company’s low valuation and the options available to it due to its huge net cash position make me optimistic about its prospects as an investment opportunity.

Company overview

Playstudios has a diverse selection of 17 games, along with a unique loyalty program that allows players to play games and earn real rewards. The loyalty program is thus able to keep its players engaged longer, thus earning more money from them.

Prior to its acquisition of Brainium in In 2022, Playstudios has mostly social casino games, with a few casual games. The addition of Brainium increased the number of unofficial games to eleven. In addition, Tetris games that Exclusive rights acquired In 2021, it also helped significantly diversify Playstudios’ portfolio, while significantly increasing its player base. The restructuring process that began in 1Q23 reorganized the company into two separate business divisions, PlayGames and playAwards. In addition, this also resulted in a decrease in overall headcount of more than 10%.

The company’s core social casino games continued to experience revenue declines due to competition as well as management’s focus on higher-spending users. The revenue decline was offset somewhat by contributions from Brainium and Tetris. Although Brainium was fully integrated into the Playstudios operating framework at the beginning of 2023, the integration of the playAwards program into the full suite of Brainium products is expected to be completed only this year. Meanwhile, the Tetris Prime product has grown significantly, according to management’s commentary on the 2023 fourth-quarter earnings call. Due to its success, the Tetris game license has been extended through 2028.

The company’s key priorities for the year were summarized by CEO Andrew Pascal during the first quarter 2024 earnings call:

As a quick summary, initiatives in 2024 include adopting a refreshed MyVIP loyalty program group-wide, restoring MyVegas and MyKonami, rolling out PlayAwards, launching at least one new Tetris game, and expanding monetization within Brainium. file. We are making significant progress on all of these fronts, and I believe we are on track to emerge from the year with an improved operating rate.

Financial snapshot

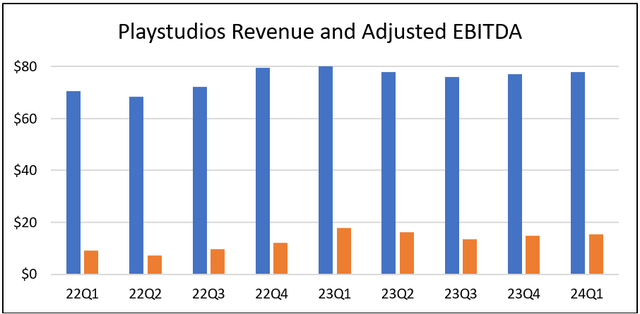

Created using company data

Throughout 2023, management shifted its focus away from revenue growth, toward achieving higher margins. As shown above, this has led to revenue stagnating in recent quarters, while adjusted EBITDA has increased significantly. In the most recent quarter, revenue was $77.8 million, down 2.8% year over year, although marginally higher than the previous quarter. However, adjusted EBITDA remained strong at $15.3 million, a solid margin approaching 20%.

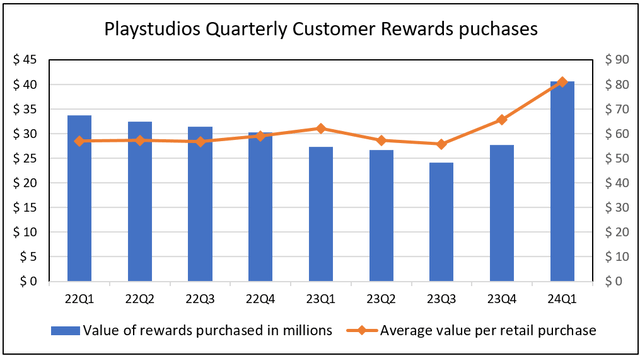

Management focused on maintaining the company’s existing user base, while increasing payer conversion and spending. This trend is evident when tracking the key metric, which is virtual currency spending in the market. Despite a continuous decline throughout most of 2023, the last two quarters showed a significant successive increase, as shown in the figure below. Furthermore, the integration of the remaining Brainium games into the loyalty platform this year should further support this growth.

Created using company data

evaluation

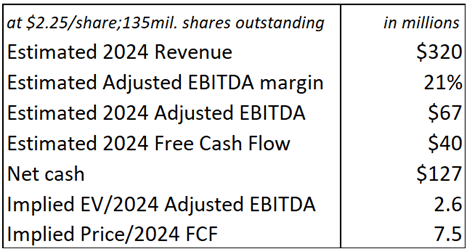

Using the midpoint of management’s 2024 guidance, the company is expected to earn about $67 million in adjusted EBITDA. In line with analyst estimates, I expect their free cash flow to be close to $40 million after accounting for their internal and growth-related investments, as shown in the table below.

My rubric is based on grades

Based on the above estimates, Playstudios currently trades at an EV through 2024 adjusted EBITDA multiple of just 2.6 and a price through 2024 FCF multiple of 7.5. Its most relevant peer in the market today is Playtika (PLTK) which has similar growth rates, yet trades at more than double its valuation with a forward EV to EBITDA ratio of 6.2. Zynga and Sciplay Corp are also industry peers, but they are no longer public companies and therefore cannot be used for comparison. However, it was acquired at a much higher valuation multiple than what Playstudios is currently trading at.

Potential catalysts for a stock price rise

Capital allocation

The company has a strong financial position with $133 million in cash (40% of its market capitalization) and no debt. Mergers and acquisitions remain a company’s primary use of its capital, and if done at the right price, can be a positive catalyst for its stock price. Jason Hahn, the company’s head of corporate and business development, also emphasized this during the first quarter 2024 earnings call when he said:

Yes, we remain committed to our M&A strategy. There are a lot of opportunities available in the market. We have an active group of companies with which we continue to engage in mergers and acquisitions. As you know, getting these M&A deals is complicated. We need to structure deals that accumulate in our financial profile, both growth and margin. It must also be strategically compelling and timed at the right time when we are able to deal with it.

The company also has a $50 million stock buyback program authorized through November of this year. The company’s CEO spoke about the company’s share repurchases during this quarter, saying:

We restarted our stock repurchase program in the first quarter and purchased an additional $4 million worth of shares for the day. We view our stock price as highly discounted and believe the buyback of our stock prices represents value for all shareholders.

Likewise, another catalyst that I think the market would welcome is the initiation of a special dividend as cash on the balance sheet is expected to accumulate each quarter going forward.

Launching the loyalty platform as a service

Management said that third-party gaming companies have shown interest in its unique PlayAwards loyalty program because it is a compelling way to retain players. If Playstudios is successful in making such deals, it could become a very lucrative additional income stream for the company.

Risks

Current investments are not paying off

As the CEO mentioned during its Q3 2023 earnings call, Playstudios is investing heavily in initiatives like loyalty-as-a-service, which are not currently generating any revenue. There is a possibility that these initiatives fail to gain traction in the market and end up becoming poor investments that destroy shareholder value.

Impact resulting from application development platform changes

Changes in platform privacy rules may have a negative impact on its business.

Ongoing lawsuits

According to its 2023 annual report, the company received four arbitration requests during 2023 related to illegal gambling.

Playstudios stock is a buy

Despite declining revenues in social casino games, Brainium and Tetris games are showing strong growth, offering plenty of room for margin expansion in the future. Management has performed well in recent quarters and the business is set up for future organic growth, while at the same time returning capital to shareholders through buybacks. At today’s share price, I think investors have an attractive risk reward to initiate a long position in Playstudios.