Maks_Lab

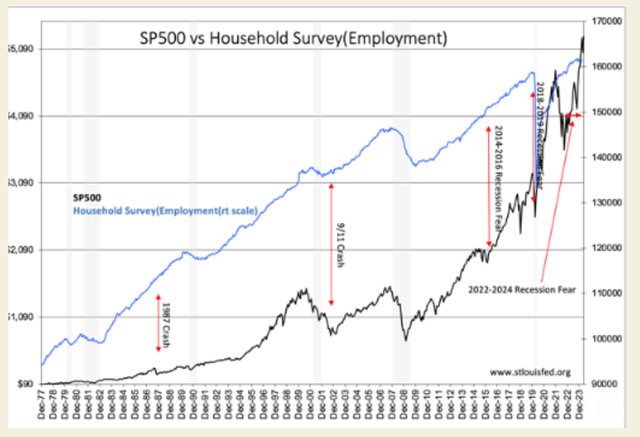

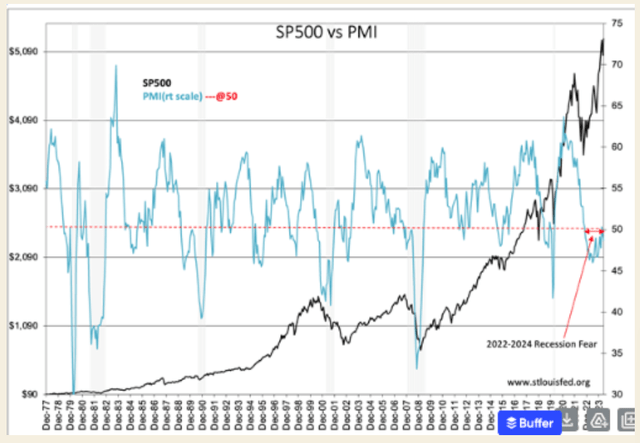

The Purchasing Managers’ Index (PMI) is considered by many to be a leading economic indicator. not. It is related to market psychology and market prices, not to economics. History since 1977 clearly shows that declines in the SP500 are closely linked to falls in the PMI (manufacturing) below the benchmark level of -50. But PMI It has fallen below its benchmark nearly three times (3x) more than in actual recessions, making this more like a shepherd boy who cries when he fears a wolf rather than when he sees one. For comparison, the SP500 vs. Domestic Employment Index shows that during the economic cycle, there are many times investors fear a recession for one reason or another, and it doesn’t show up. There are several red arrows in this chart to identify just a few of the periods when concerns rose without economic significance. To flag all these instances during upgrades that were header bogus would make this chart unreadable.

In the current cycle, we’ve had our share of “recession at the door” forecasts, yet employment continues to rise, although in a slow trend, real personal incomes continue to rise and real retail sales remain at elevated levels. The same can be said about total construction spending and new manufacturers’ orders for durable goods. The old adage “the market is rising on a wall of worry” still holds true, as the SP500 is approaching record highs. One could say the market is bullish this time based on recession fears fueling the few issues thought to be safe havens of capital, those 10 or so over-owned high-tech issues that make up 25%-30% of the SP500. CNBC referred to them as the Mag 7. Much of the rest of the SP500 remains discounted compared to previous investors’ pricing of their financial performance. The heavy overpricing of a few versus the heavy underpricing of many makes this swing extreme and ready for a pullback.

The Purchasing Managers’ Index, currently below 50, reflects market pessimism. However, we have had several better than expected earnings reports with raised guidance that investors have ignored. These earnings reports are linked to upward trends in fundamental economic indicators. “Wolves at the door” will give way as economic indicators trend higher. I thought this would have happened by now, but the recent drop in the PMI has caused more concern. For PMI, mind over matter, and history shows that it takes time for fear to dissipate. In my opinion, the rise in the Purchasing Managers’ Index (PMI) from its June 2023 low of 46 is telling. It appears that pessimism is beginning to subside, and the next two reports may take us to above 50. This level would lead to investors turning towards the long-awaited industrial/manufacturing issues.

Original post

Editor’s note: The summary points for this article were selected by Seeking Alpha editors.