com. primaryimages

Welcome to another installment of our weekly Favorite Market review, where we discuss preferred stock and baby bond market activity from the bottom up, highlighting individual news and events, as well as from the top down, providing an overview of the broader market. We are trying too To add some historical context as well as relevant topics that appear to be driving the markets or that investors should consider. This update covers the period up to the last week of May.

Be sure to check out our other weekly updates covering the Business Development Company (“BDC”) as well as the closed-end fund (“CEF”) markets for views across the broader income space.

Market action

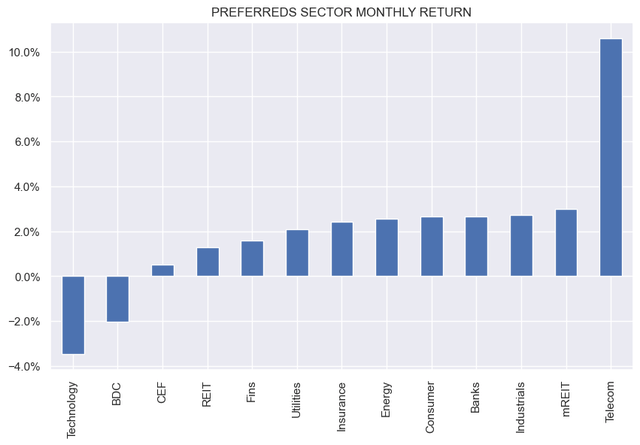

The favorites had a good week and a good month, with most sectors finishing in the green. May was the sixth month in the last seven months for the asset class.

systematic income

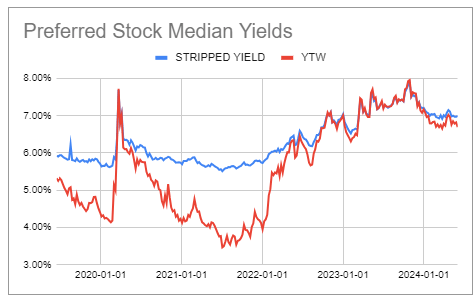

Yields have traded mostly within a range this year at just under 7%.

Systematic Income Preferences Tool

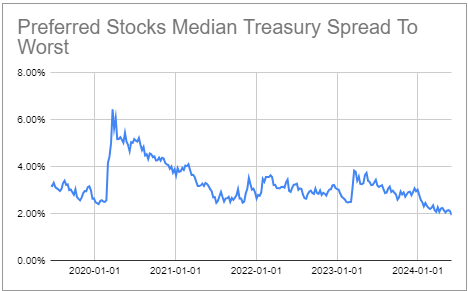

Spreads continue to trade at very tight levels – a common theme across the broader income space.

Systematic Income Preferences Tool

Market topics

BDC Main Street (MAIN) is issuing $300 million in 6.5% bonds due 2027. Aside from the issuance itself, which is nice to see, what is interesting here are two features of the new bonds.

First, the bonds are fairly short-term at 3 years, at the shorter end of the typical 3- to 5-year BDC bond range. Bonds of similar quality tend to be significantly longer term. Investment-grade corporate bonds have a duration in the high single digits on average, or nearly twice the duration of a typical BDC bond.

Because the yield curve is inverted, shorter-term bonds tend to have higher yields, all other things being equal. For example, MAIN pays 0.15-0.25% more than it would if it issued a 5-year bond. In short, the shorter maturity of relatively high-quality BDC bonds provides investors with higher returns in the current environment (not to mention lower interest rate exposure).

The second interesting feature of Sindh is its universal provision. This is not uncommon in the BDC space but uncommon in the broader corporate bond space. This means that if the company calls the bond early, it must repay future coupons, discounted appropriately. The discount is usually made at a margin less than the company’s market spread. In other words, if a bond is called, it will likely be called at a price above the market price of the bond but below the price where coupons are simply valued as risk-free.

Because this feature is favorable to bondholders in the event of a redemption (versus a traditional purchase), the yield on the bond is lower than it would be in a more traditional purchase structure, such that the bond could simply be redeemed at face value. At the same time, there is little chance of a windfall for bondholders if the company decides to redeem the bonds, such as if it needs to deleverage or if it wants to opportunistically replace the bonds with another instrument.

This is the second bond issued by the company this year. Interestingly, MAIN issued a 6.95% 2029 bond in January – a 5-year bond that will likely be used to repay the 5.2% bonds due this year. The 6.5% use of proceeds for the 2027 bonds indicates repayment of the credit facility, which makes sense because the interest on the facility is more than 7%. Replacing credit facilities with bonds is one way companies manage the rise in interest expenses from bond refinancing (i.e. replacing 5.2% bonds with 6.95% bonds, etc.). There is a limit to this, however, as few BDCs will want to completely replace their secured variable rate facilities with bonds.

We still like BDC’s baby bonds sector for a number of reasons. This includes the strong performance of book values in the sector, especially compared to other investment companies sectors such as real estate REITs or many mutual funds. Second, companies are subject to the asset coverage requirements of the Investment Company Law, unlike real estate REITs, for example. Third, most BDCs have on average half of their commitments in secured financing – instruments such as repurchase agreements or bank facilities that outperform unsecured bonds. This is in contrast to REITs where the secured financing is much larger than bonds in a typical capital structure. In this sector, we like bonds such as HTFC, OXSQZ, TRINZ, which are all trading at yields of around 8% or higher.