com.iantfoto

public storage (New York Stock Exchange: BSA) is one of the most popular REITs in the world, and it’s easy to understand why:

- Individual investors see their self-storage properties everywhere, which gives them a sense of familiarity with their real estate Property.

- It has a very strong balance sheet, which is a clear advantage in today’s environment.

- Historically, self-storage properties have generated consistently high returns in all market environments, including recessions.

- The REIT has a very broad reach with a $50 billion market cap and inclusion in the S&P500 (SPY), which reduces risk.

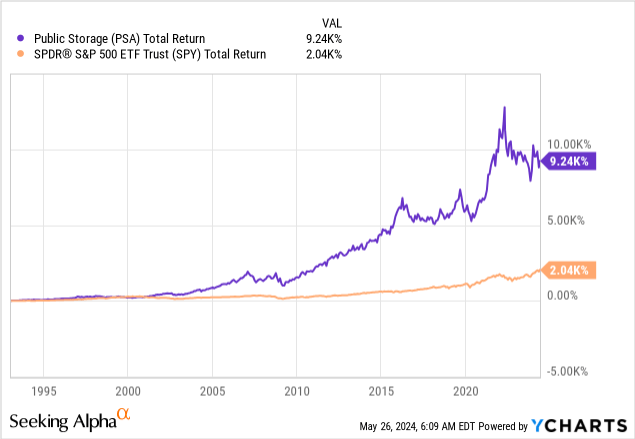

- PSA has a multi-decade track record of steady earnings growth and has significantly outperformed the rest of the REIT market:

Public storage

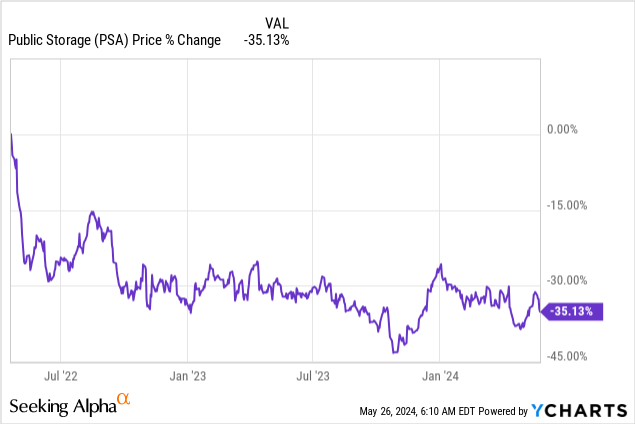

But that strong reputation didn’t protect PSA from the REIT bear market that began in 2022. It took Below every REIT, including even the best ones.

As a result, PSA is down 35% since the start of 2022, even though its cash flows have grown 25% since then. This basically means that its valuation has been cut in half:

Is now a good time to buy its shares while they are discounted?

Or should you sell before the price drops further?

I’m generally very bullish on REITs (VNQ) and that might lead you to think I’d be a buyer here, but I’m not, and here are three reasons why:

Reason #1: Significant oversupply risks

The pandemic has led to a surge in demand for self-storage spaces due to four main reasons:

- Suddenly people needed to make space for a home office

- The older generations have passed away and left behind a lot of things

- People bought a lot of new toys abroad

- Finally, many people moved from one city to another.

Furthermore, this surge in demand occurred at a time when very little new supply was being built, and as a result, the market was severely undersupplied, allowing PSA to dramatically raise its rents and increase occupancy rates.

But that attracted a lot of developers in the self-storage space, and now the company is facing quite the opposite environment.

Demand is returning to normal as the world gradually returns to normal, with an increasing number of people returning to their offices, selling their toys, and moving less than they did in previous years.

At the same time, a huge wave of new supply hits the market, putting it in a state of oversupply.

As a result, PSA’s NOI fell 1.5% in the first quarter, after already struggling in 2023. The occupancy rate also decreased by 0.8% to 92.1%.

Unfortunately for PSA, this difficult environment is likely to continue for much longer as there is so much supply, and the coronavirus-fueled demand has not been fully sustainable:

Public storage

Its management suggests that things will improve in 2025 and 2026, and perhaps they are right.

But I fear that if we enter a recession, demand may not be quite as recession-proof as it was in the past, because the rents for self-storage are much higher today. In previous recessions, it was easier to simply ignore storage expenses because they represented a smaller percentage of your income, but after massive rent increases due to the pandemic, more people will likely put their leases on hold as they look to cut back on spending.

Finally, in the long term, I have another concern about self-storage space, especially in the USA.

Today, there is 10 times more warehouse space in the US than in the UK and 40 times more than in mainland Europe. I think some of this vast difference can be explained by cultural and geographic reasons.

But I believe that consumer spending in the United States will gradually move more and more from buying “things” to buying “experiences” instead. Europeans don’t buy as many games, but they spend more on experiences, and I see American people heading in the same direction.

The “experience economy” is growing rapidly, I don’t see this going away, and it represents a long-term headwind for self-storage facilities. Not only that, but the “sharing economy” is also growing rapidly, which is also a headwind for self-storage facilities. For example: If you can easily rent an RV and it’s affordable, you’re less likely to buy one for yourself.

Reason #2: Too big for its own good

I have previously shown that this measure has advantages. It leads to lower expenses, improved access to capital, and lower risk.

But after a certain point, economies of scale turn into economies of scale, and I’ve often used Realty Income (O) as an example of this.

Its growth rate has slowed because it is much more difficult to grow from a $50 billion base than from a $5 billion base. New acquisitions no longer move the needle much, and you need to acquire a significant amount of new properties just to keep the ball rolling. You will then lose flexibility, agility and bargaining power with real estate sellers, which will likely result in you lowering your underwriting standards and paying more than you would have paid otherwise.

Well… PSA is just as large as Realty Income, so I think its size will likely slow its growth in the future as well. I would rather have a much smaller self-storage ETF.

Reason #3: Better opportunities elsewhere, including her peer group

PSA’s rating has declined significantly since the start of 2022.

Even then, it’s priced at 17x FFO today, which doesn’t seem “cheap” to me when you consider that it’s facing some severe headwinds and that its cash flow is declining.

There are plenty of REITs that are priced at lower multiples and are actually growing their cash flows. For example, Big Yellow Group ( OTCPK:BYLOF / BYG ) is the UK leader, at 16.5x PE, despite having much better long-term growth prospects.

Therefore, I find it difficult to justify investing in PSA.

Sure, it’s no longer priced at the “Champagne” valuation it was in 2021, but that doesn’t make it cheap today. I still expect it to do relatively well over the long term, but I just think some other REITs will do much better, and for that reason, I have no interest in owning PSA at this time.