Robert Y

PVH shares (New York Stock Exchange: BVH) has had a strong but volatile performance over the past year, rising more than 50%. PVH shares fell sharply after the latest set of quarterly results were announced, but I urged on Investors bought the dip, and the stock has since risen about 10%. I have argued that we are likely to see the company outperform conservative guidance, and on Tuesday afternoon, PVH raised its EPS guidance this year to the expected range. Shares were largely flat in response after hours and near the low $120 target price, making now a good time to reconsider the stock. I’m raising my price target and will remain a buyer.

Seeking alpha

In the company’s first quarter, PVH earned $2.45, which beat estimates by $0.26. Revenue fell 10% from last year to $1.95 billion. Excluding liquidations, revenues decreased by 7%. Adjusted EPS excludes a $0.10 gain on the sale of the Heritage Brands lingerie brand. Q1 results were $0.30 above guidance. Sales decreased by $206 million, but gross profit decreased by only $52 million with margins rising 350 basis points to 61.4%, due to input cost contraction and the decision to reduce sales to lower-margin wholesale channels. Management also indicated that it is seeing improved pricing power. In addition, SG&A declined more than 4% as management continues to carefully manage costs.

We continue to see meaningful geographic divergence with the US leading the way, Asia also positive while PVH has strategically reduced lower margin sales in Europe. North America revenue increased 3% with growth in both DTC (direct-to-consumer) and wholesale channels. Globally, DTC revenue increased 1% and 3% in constant currency. Interestingly, physical stores rose by 3% while online stores decreased by 6%. Wholesale revenues decreased by 17%, and 11% after exits. He sees wholesalers being particularly cautious in Europe. PVH also made a strategic decision to reduce sales through low-margin channels in Europe.

This decision reduced revenue, but as evidenced by the broad margin expansion, there was a much smaller impact on profit and loss. By rationalizing sales, it was also able to reduce inventory to $1.35 billion, 22% less than last year. In doing so, it freed up working capital, enabling stock buybacks. Additionally, by holding less inventory, they are less likely to experience product surplus, reducing the need for discounting and keeping their sales profitable.

Given this focus on maximizing sales value rather than simply maximizing revenues, it is noteworthy that the CEO of PVH Europe will be leaving his position. He was also responsible for the Tommy Hilfiger brand globally, which was more reliant on lower-margin channels than the Calvin Klein unit. The focus on profit growth, rather than sales growth, is already paying dividends at Calvin Klein’s unit, and in the United States more broadly. A similar result at Tommy Hilfiger Europe would be a positive positive for the company.

Digging deeper into each brand’s results, we’ll first look at Tommy Hilfiger. Its sales fell 10% to $1.01 billion, with North American sales up 2% and international sales down 14%. Tommy Hilfiger gets 71% of its revenue from abroad. Tommy’s sales have been particularly affected by planned cuts in Europe, and I expect this quarter to represent the worst of the declines year-on-year. Tommy Hilfiger’s U.S. profits rose from $2 million to $24 million, as sales grew and inventory rationalization efforts helped improve margins. Due to lower sales, overseas profits fell from $126 million to $76 million. Overall, profits fell by about a quarter to $101 million.

Calvin Klein sales were steady at $887 million, with a decrease overseas of 2% and an increase in North America of 4%. 68% of its sales are international. The significant discrepancy in brand performance, and the particular need to revamp Tommy Hilfiger’s European strategy, explains why PVH should make a change in management. Although its revenue is about 13% lower than Tommy Hilfiger’s, Calvin Klein is more profitable. Profits rose 30% to $133 million thanks to improvement in North America.

Overall, I see this as an encouraging quarter. PVH demonstrated very resilient margin performance as it rethinks its European sales strategy. The strong results in North America and strong Calvin Klein speak to the benefits of a diluted wholesale strategy, which, if applied successfully at Tommy Hilfiger, could be of significant benefit to earnings over the next 18 months. It also continues to have a strong balance sheet of $376 million in cash and $2.1 billion in debt, and interest expense fell by $4 million to $18 million, helped by higher rates earned on its cash. During the quarter, PVH took advantage of declining shares to make $200 million in buybacks. As a result, its share count is down 8% from last year, and management plans to buy back $400 million over the full year, which will reduce its share count by another 3%.

In terms of future outlook, in the second quarter, it expects revenues to fall by 6-7% or a 3% decline excluding divestments, a significant improvement from the first quarter, supported by easier comps and the transition from the reset in Europe. For the full year, PVH confirmed that it expects full-year revenue to decline by 6-7%. However, it raised its EPS guidance from $10.75 to $11.00 to $11.00 to $11.25. Back in April, I argued that we might see a revenue decline of about 5% this year and that we would likely see EPS in the $11.00-$11.25 range. Our PVH now matches my EPS expectations, although revenue is still a bit lower. More aggressive buybacks pushed the share dilution forward, and margin expansion was stronger than I expected, which is why I was able to raise my EPS forecast, in my view. Now, I still think there’s room for upside in sales, which leads me to believe EPS should be between $11.20 and $11.40 this year, based on Q1 margin results.

In terms of North America, I’m comfortable with the overall apparel retail background. Employment rates remain strong, and disposable income is rising. Importantly, major retailers like Macy’s (M) have reduced inventory significantly, so headwinds from wholesale channels should be complete. Furthermore, after spending an unsustainable amount on clothing in 2022, spending has stalled in 2023 and is now within 3% of trend. With spending close to long-term trends, I believe the backdrop is favorable for modest growth in apparel consumption of 0-2%. This will enable continued sales growth for PVH’s North American operations.

St. Louis Federal Reserve

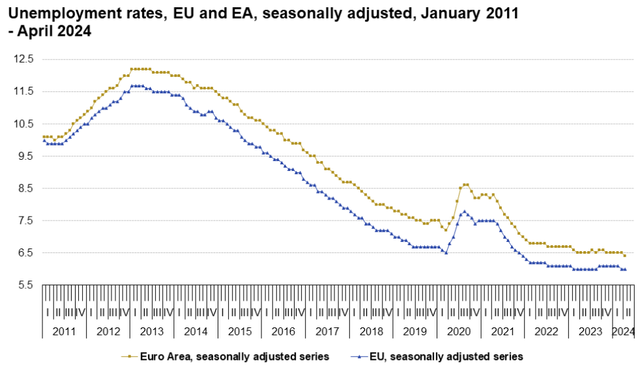

Now, as mentioned, about 70% of PVH is overseas, so the US can only drive so much growth. Most importantly, I feel comfortable with its European exposure. After Covid-19, Europe lagged behind the US by 6 to 12 months, and just as US retailers were reducing inventory last year, their retailers are doing so now, which is why wholesale is weak. As this process is completed this year, these headwinds should fade. It is also important to note that the European economy is fairly strong, with unemployment falling to pre-coronavirus levels.

Eurostat

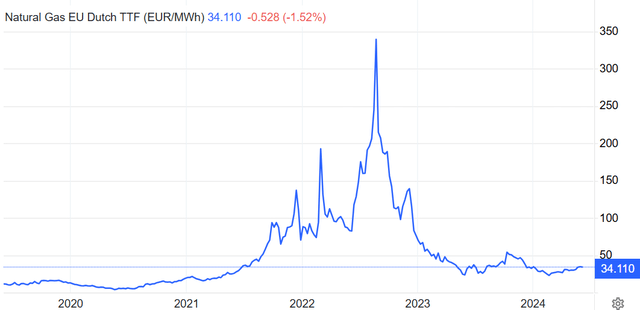

The biggest challenge facing Europe has been the sharp rise in energy price inflation as it seeks to limit its exposure to Russian natural gas. This put significant pressure on consumers’ incomes. More importantly, as LNG exports have increased, we have seen natural gas prices decline significantly over the past 18 months, freeing up consumer income for more discretionary items such as clothing. Lower inflation pressure also means that the ECB is more likely to cut interest rates before the Fed, in my view. Although Europe may not be as fast growing, we should see some tailwinds here against the current backdrop, allowing for some increased sales activity and allowing PVH to beat revenue guidance in my view.

Trading economics

Last quarter, I thought PVH set itself a very conservative target for 2024, and that appears to be the case after the quarter, with the guidance lifted. However, I still see more upside risks to the guidance given the modestly positive macro conditions, meaning that European transition efforts are likely to be well-timed. At my estimate of $11.30, it’s only 10.6x earnings. I see roughly 12 times earnings, or about 8% earnings yield, as an appropriate multiple for the company.

Fashion tastes can be fickle, limiting multiple expansion in my view, and PVH’s European exposure will likely be viewed with caution. To compensate for this, it has prominent brands and an excellent balance sheet. Assuming long-term growth of 2% to 4%, or slightly less than global nominal GDP growth of 4% to 5% (since Europe is growing somewhat slower), with a dividend payout of 60%, PVH could To generate about 10% long-term returns (a) 5% annual repurchase, growing at about 5% annually) at a multiple of 12x. This could push shares to lows of $130. As investors become more confident in its European transition, and we see more guidance, I expect stocks to continue their recovery. I will remain a buyer.