Evening pictures

Investment thesis

Box Inc. (New York Stock Exchange: FundYesterday, it announced earnings results for the first quarter of fiscal year 25, which exceeded estimates. The maker of workforce synchronization, content management, and productivity cloud software is currently in the midst of a transformation as it tries to get a core process going Transforming its business in the face of artificial intelligence.

Although Box beat estimates, my opinion of the Redwood City, Calif.-headquartered company remains the same: The overall outlook remains clouded by the wide range of offerings it has posted in the last 12 to 15 months. The company moved to sell its cloud-based content management and productivity software to take advantage of the massive amounts of unstructured data its customers were storing on Box’s cloud storage products. In addition, the company also launched BoxAI last year targeting larger enterprise customers as part of its strategy to re-accelerate growth.

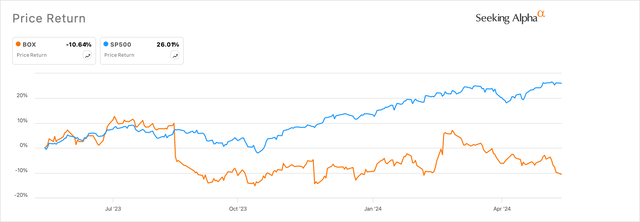

But I have not yet seen any trace of growth beyond 10%. This has also impacted the share price, which is severely lagging all indices so far, as shown in Figure A below.

Exhibit A: Box Inc lags the broader markets on a trailing twelve-month basis (Searching for Alpha)

The results are not exciting enough, and I expect the stock to stay within a range and move away. For now, I recommend Hold.

Nothing out of the ordinary for growth

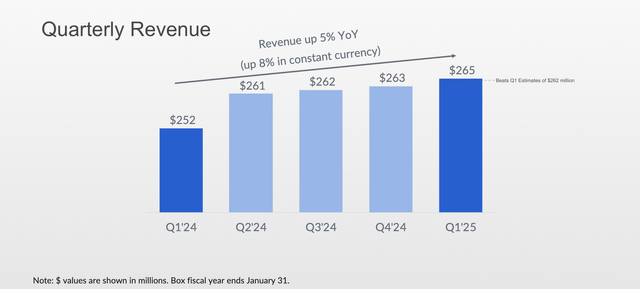

In Box’s fiscal 1Q25, the company reported total sales of $264.7 million, up 5% year over year and topping the consensus mark of roughly $262 million, as shown in Exhibit B below.

Exhibit B: Q1FY25 revenues up 5% year over year (Q1FY25 earnings results, Box Inc.)

Box’s management attributed the growth in its revenues to sustained single-digit demand among its institutional clients. Box has launched Enterprise Plus pricing for enterprise customers, tracking conversions to its suites, and multi-product offerings. In a recent earnings call, management stated:

Suites account for 81% of deals worth more than $100,000, compared to 72% a year ago. We have seen a continuation of strong wings attaching prices to large deals across all geographies.”

Suite customers now represent 55% of our revenue, which is a significant improvement from 46% in the fourth quarter of last year and from 51% in the third quarter.”

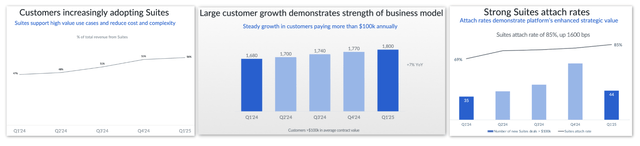

In 1QFY25, Suites customers represented 56% of Box’s total quarterly sales, as shown in Figure C below. At the same time, the company has made further progress in penetrating the larger customer segment, as evidenced by growth in customer volume > $100K in average contract value.

Exhibit C: Enterprise customers add momentum to Box as witnessed by Box and Suites customer growth rates (Q1FY25 earnings results, Box Inc.)

Wing attach rates, which is the rate at which winning deals also transact by selling target customers wings on their annual contracts, showed some improvement, compared to the same quarter last year when the wing attach rate metric showed signs of decline (page 19).

The company’s net retention rate has shown some signs of stabilizing at 101% after eight straight quarters of decline. I think net retention rate will be a key metric to watch, as it will indicate the spending appetite existing Box customers have for the company’s suite of content storage and management products. Any decline below the 100% mark would indicate revenue contracting, assuming its customer base does not increase.

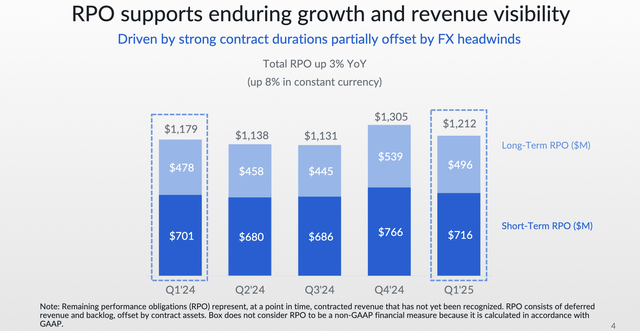

An alternative method the company prefers to track growth in an enterprise customer base is to measure the company’s ability to contract customers for longer leases. For management, this means locking in customers for longer annual contract periods. This can be seen in Figure D below, which shows that while total RPO rose 3% YoY, long-term total RPO rose 3.8% YoY outpacing total RPO growth.

Exhibit D: Trends in Fund’s remaining performance obligations (FY2025 Q1 earnings results, Box Inc.)

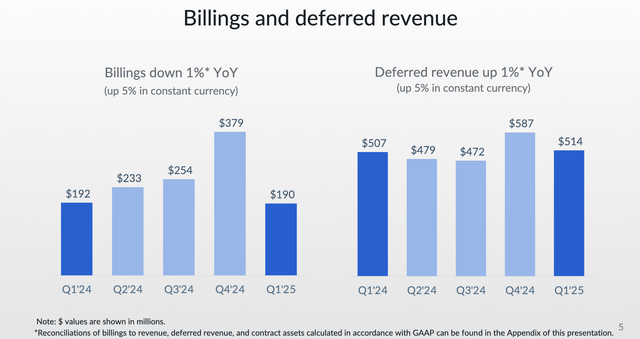

But I would take that with a grain of salt because it doesn’t necessarily paint the right picture when looking at billings and deferred revenue metrics that are barely growing, as shown in Figure E. Knowing that Q1 quarters are the weakest for SaaS companies, Box’s management will need to do more to convince its investors of strong, sustainable long-term growth, in my opinion.

Exhibit E: Revenue Growth and Deferred Billings at Box (Q1FY25 Earnings Results, Box Inc.)

Profitability is showing stronger signs of growth

On the other hand, Box’s profitability metrics looked much more promising. At 78%, our Q1 GAAP gross margin was one of the strongest I’ve seen in the longest time, probably since October 2014.

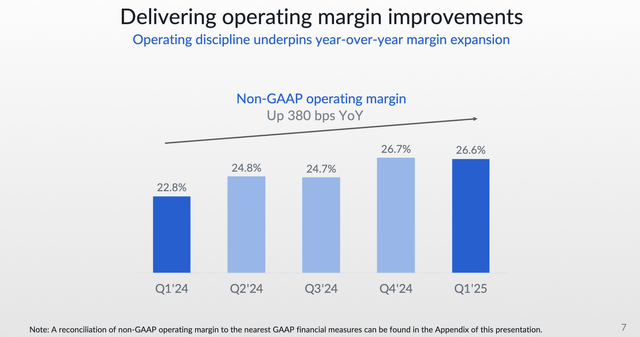

In the first quarter, Box reported Q1FY25 non-GAAP earnings of 39 cents per share, or 8 cents on a GAAP basis, beating consensus estimates by 8.3% and up 21.9% on Annual basis. In the quarter, Box also reported record operating income of $70.4 million, up 22.6% year over year on an adjusted basis. This resulted in adjusted operating margin expanding by 380 basis points to 26.6%, as shown in Figure F below.

Exhibit F: Box delivers strong margin expansion in operating income on an adjusted basis (Q1FY25 earnings results, Box Inc.)

In prepared statements to analysts during the call to discuss first-quarter earnings, management said:

We are pleased to have achieved first-quarter revenue growth of 5% year over year, or 8% in constant currency. A continued focus on operational discipline resulted in first-quarter operating margin and EPS significantly exceeding our guidance, recording a non-GAAP gross margin of 80%, and free cash flow growth of 14% year-over-year. We remain focused on delivering revenue growth while maintaining our commitment to continued cost savings and further expanding operating margin.”

Meanwhile, the company’s balance sheet remains stable, with debt and operating leases at approximately $552 million. The company should be able to service the principal portion of its $345 million 2026 senior notes, as it currently has approximately $450 million in cash.

As growth has yet to show signs of re-accelerating, management signals encourage me to achieve profitable growth and maintain a stable balance sheet, which should be able to support the company well during this transition period.

The fund’s valuation is not attractive enough

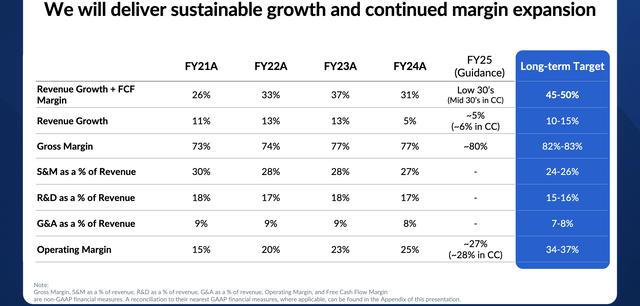

Unfortunately, Box’s tepid growth rates aren’t exciting enough for me to get excited about the company’s prospects. The company’s first quarter results have been average so far and haven’t stood out to me. In formulating my forecast for Box, I took into account the company’s long-term goals that were laid out in the company’s Financial Analyst Day presentation in March. Below is a screenshot of the guidance summary from this presentation.

Exhibit G: Management’s Long-Term Growth Goals (FY2025 Financial Analyst Day, Box Inc.)

Here are my assumptions that were factored into my outlook:

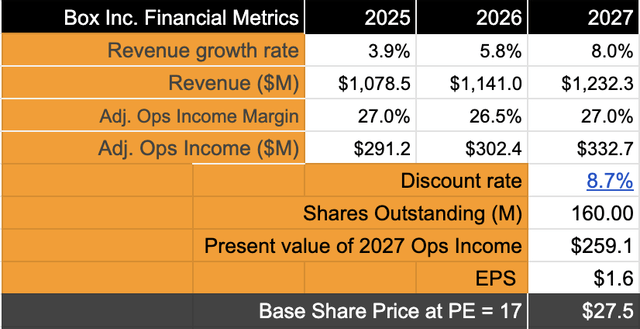

- Based on historical trends and the future growth rates that management expects, I would assume that Box will increase its sales in the mid-single digit range. This implies a CAGR of 6-7% between FY24 and FY27, as shown in Figure (h).

- According to the Q1 report, management indicates that it raised revenue guidance for FY25. But in deeper analysis, I see that it is only on a constant currency basis. The reality is that revenue guidance for FY25 has been pulled down quite a bit, from the previous targets of $1.08-1.085 billion issued last quarter to the updated targets of $1.075-1.08 billion issued this quarter.

- I expect Box to continue to deliver strong margin expansion in its operating income on an adjusted basis, as stated in previous management’s intentions and goals. I expect some leveling off over the next year because I think management may increase SG&A to better target institutional clients, but I expect that to return to normal. Over time, Box should achieve faster growth in adjusted operating income, growing in the 9-10% range.

- I have assumed a discount rate of 8.7% based on the estimates mentioned here.

Figure H: Box evaluation model indicates minimum height (author)

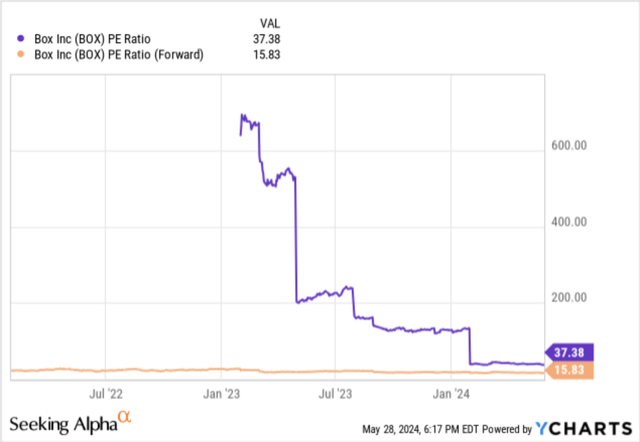

If I compare the growth rates from my assumptions to the long-term growth rates of the S&P 500, I believe the company warrants a forward P/E of between 16 and 17, in line with the multiple expectations for overall forward earnings as shown in the first figure below. My model implies a 9% upside, but this is not dramatic enough given the lack of growth catalysts for Box in the face of fundamental risks.

Figure 1: Future PE Trends for Box (YCharts)

Risks and other factors to look out for

Most cloud software solutions for content storage and management, such as Box, Dropbox (DBX), and DocuSign (DOCU) have faced uncertain environments since macroeconomic and geopolitical risks have shifted forces in the markets in which most of these companies operate, especially in the SMB markets.

I appreciate Box management’s efforts to revitalize its overall business and product development strategy, but it faces headwinds from larger technology shifts, as seen in AI, as well as vendor consolidation with larger platform providers, which has continued to pressure Box. Box made some acquisitions to enter new markets, such as electronic signature, but those markets quickly became saturated, leaving Box to pivot again.

Additionally, the pressure that Box’s original target market, SMBs, continues to experience from Box, in my opinion, forcing Box to spend more on sales and marketing to target larger enterprises. So far the company has shown some improvement, albeit with low single-digit growth.

He stays away

The Box Quarter didn’t excite me, leaving me looking for traces of further catalysts as I scanned the earnings report. Unfortunately, it appears that these growth catalysts are still out of reach for Box, leaving management to become more disciplined about maintaining strong profitability. Fortunately, Box’s profitability story looks more promising to me.

For now, I recommend being neutral on Box, despite the ~9% upside.