Sebastian Gorczowski/iStock via Getty Images

Investment thesis

FlexShares Defensive Dividend Index Fund (NYSEARCA:QDEF) has been one of the best-performing large-cap ETFs in recent years. However, this is only because it is not as defensive as its name suggests. My basic analysis It reveals that it’s one of the most growth-oriented programs in its category, and since there are already many low-cost alternatives offering the same thing, I see no good reason to pay its 0.37% annual fee. As a result, I have assigned a Neutral ‘Hold’ rating to QDEF, and I look forward to explaining why in more detail below.

QDEF Overview

Strategy discussion

Launched on December 14, 2012, QDEF has an expense ratio of 0.37% and assets under management of $363 million. It tracks the Northern Trust Quality Dividends Defensive Index, which the index provider describes as follows:

Quality Dividend from Northern Trust The defensive index is designed to provide exposure to a high-quality, income-oriented universe of long-term US equity securities only, with an emphasis on long-term capital growth and a target aggregate beta that generally ranges north of 0.5 to 1.0 times. Trust 1250 Index (original index). Companies included in the index are selected based on expected dividends and basic factors such as profitability, management experience and cash flow.

The index provider uses a proprietary scoring model to evaluate company quality and aims to achieve a higher dividend yield than the benchmark index. In addition, the index provider manages systematic (market) risk with the following limitations:

- Security weight (+/- 5% vs. standard)

- Industry Weight (+/- 10% vs. standard)

- Segment weight (+/- 6% vs. standard)

- Turnover rate: 25% maximum on each rebalancing date

The indices are reconstituted four times a year on the last business day in February, May, August, and November, so the turnover constraint is very large. However, sector constraints mean QDEF will still have a good allocation to technology stocks. As of May 30, 2024, it was 30%. Let’s take a closer look at the fund’s composition next, as I believe these constraints limit QDEF’s “defensive” ability.

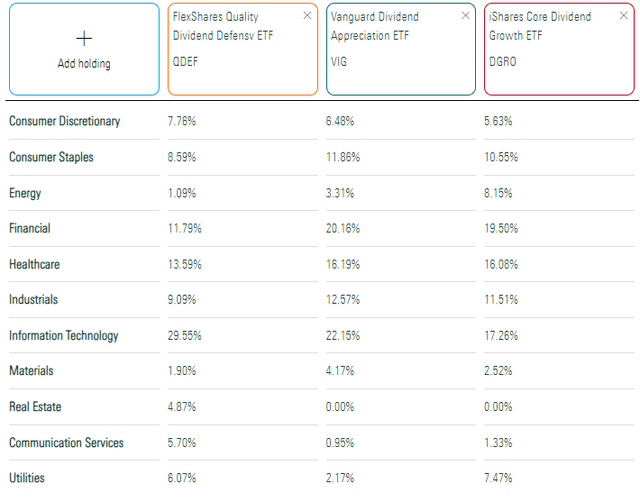

Sector exposures and top ten holdings

The following table highlights QDEF’s sector exposures along with the Vanguard Dividend Appreciation ETF (VIG) and the iShares Core Dividend Growth ETF (DGRO). Despite their focus on earnings growth, VIG and DGRO share many similarities with QDEF, namely their higher position on the value scale.

Morning star

QDEF is arguably the least defended of the three. In addition to increasing exposure to technology stocks by 7-12%, QDEF also reduced the weight of consumer staples by 2-3%, a sector known for its defensive capabilities.

The ten largest holdings in QDEF include Apple (Camel), Microsoft (MSFT), nVidia (NVDA), and identification platforms (dead), and they all bear fruit. Their higher weights are likely related, in part, to the 5% security restriction mentioned earlier.

FlexShares

I have no doubt that if Amazon (Amzn) and Tesla (TSLA) dividends paid, they will also be in the index. As for the alphabet (Google), the company will He paid his first dividend For registered shareholders on June 10, 2024, so I expect it will be added in the reconstitution in August. The bottom line here is that the constraints imposed by the index have huge implications, and because the country’s largest companies are mostly growth-oriented, the index’s defensive capabilities are limited.

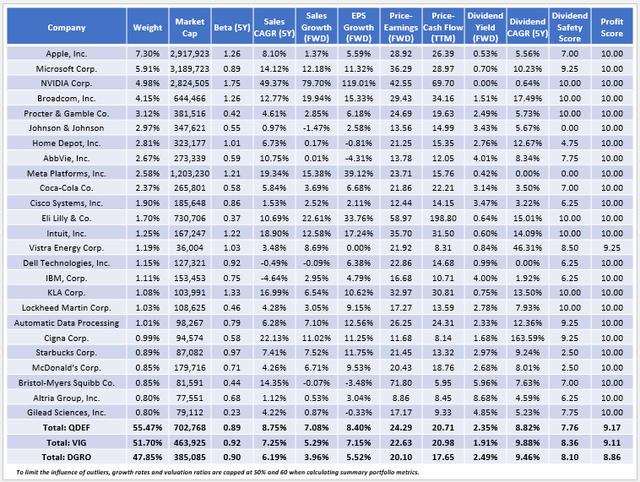

QDEF analysis

The following table highlights selected key metrics for QDEF’s 25 largest holdings, totaling 55.47% of the portfolio (cash-adjusted). I’ve also included summary metrics for VIG and DGRO in the bottom rows.

Investor Sunday

I have four notes:

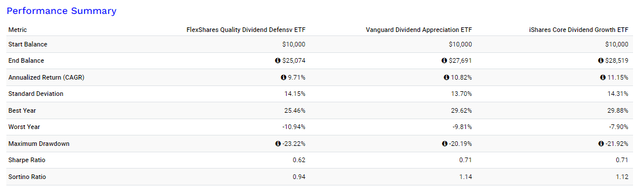

1. The five-year average beta for large-cap ETFs and large-cap ETFs is 0.97 and 0.93, respectively, which shows how it’s not unusual for dividend stocks to be slightly less volatile. At 0.89, QDEF’s beta is lower than most of its peers, but not by much, and the reason is its high allocations to Apple, Nvidia, and Broadcom (Afgo). Even considering its track record since July 2014, QDEF’s ‘standard deviation’, ‘worst year’ and ‘maximum drawdown’ numbers don’t stand out as impressive.

Portfolio visualizer

2. Nvidia’s 4.98% QDEF allocation is the source of its relatively high EPS growth rate of 8.40%. If the stock were not included, QDEF’s earnings growth rate would be 6.15%, 1% less than VIG, which excludes the stock. While QDEF’s forward P/E will fall to 23.93 times, it is still more expensive than VIG, so I don’t think it offers good value.

3. The QDEF index yield, calculated on the basis of the weighted average dividend yield of all its members, is 2.35%. After subtracting the fund’s expense ratio of 0.37%, net shareholders should be 1.98% compared to 1.85% and 2.41% for VIG and DGRO, respectively. Additionally, the current components of all three ETFs have similar five-year dividend growth rates of between 9 and 10%, so there is not much separation between them and a DGI perspective.

4. QDEF has impressive profitability metrics compared to VIG and DGRO, including:

- Return on assets: 13.04% vs. 10.44% vs. 8.63%

- Return on equity: 29.29% vs. 28.25% vs. 24.74%

- Return on total capital: 19.01% vs. 15.66% vs. 13.67%

However, these metrics are related to the QDEF configuration. Remember, QDEF overweights technology, an asset-light sector, by 7-12%. Asset-light companies typically have high margins, so comparing the quality of ETF picks to their sector peers is essential. This is where looking up alpha factor scores can help, and after converting each score into a number on a ten-point scale, the QDEF score is 9.16/10 compared to 9.11/10 for VIG. Again, the difference is slight.

Investment recommendation

QDEF’s expense ratio of 0.37% is very high, and its growth combination and valuation are no better than those of VIG, a similar yield fund with an expense ratio of 0.06%. While QDEF has a ten-year track record, that is mostly because it is a “light value” fund with a forward P/E that is third highest in the large-cap value category. Finally, its security restrictions mean Alphabet is a potential addition in August, which could result in a lower dividend yield and less downside protection. The QDEF may track the Defensive Earnings Index, but there are cheaper and better alternatives, so I wouldn’t recommend buying. Thank you for reading, and I look forward to your comments below.