owngarden

Kevo Technology Company (Nasdaq: Enough) announced its first-quarter results, highlighted by strong growth and stable profitability. The China-based fintech company is managing mixed economic indicators in the region and persistent headwinds for consumer credit by tightening lending standards and streamlining business. Last The results indicate that the strategy is working.

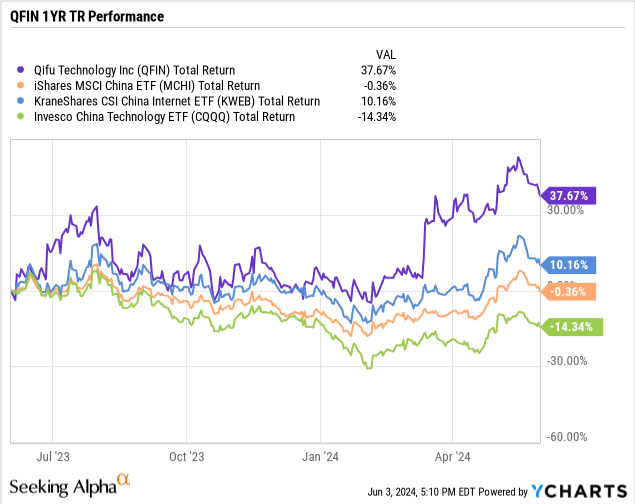

We last covered the stock in late 2022 when the company was still known as “360 DigiTech” before changing the company name in March of last year. While the stock has been volatile going into 2023, the stock has been gaining momentum recently and is outperforming Chinese stock indexes.

In many respects, operational and financial trends have developed better than we expected, and we can reiterate our bullish outlook. The attraction here is the company’s strong fundamentals, which include a generous stock buyback program and dividend policy. We see room for more upside in the future.

QFIN Q1 Earnings Summary

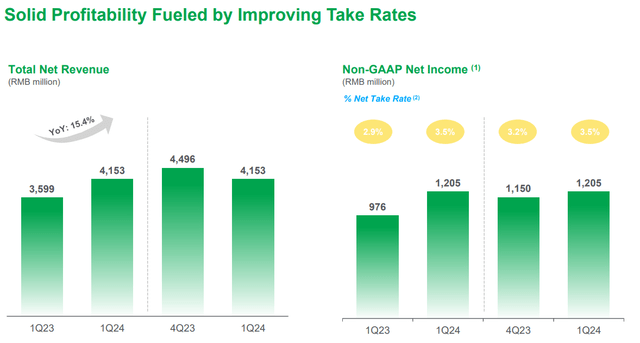

QFIN’s first-quarter earnings per American depositary shares (EPADS) of $1.05 rose 28% year-over-year from $0.86 in the first quarter of 2023. The result in this quarter represents adjusted net income of CNY 1.2 billion, or about 167 million USD, also rising sequentially from the fourth quarter. Revenue of $575 million increased 15% year over year.

Although the overall volume of loan originations decreased by -9.3% compared to the same period last year, the borrowing rate as a measure of profit per transaction increased by 54 basis points to 3.5%.

Management explains that amid the changing macro backdrop over the past year, lending standards have become more stringent, but borrowers are willing to pay higher spreads.

Source: IR Company

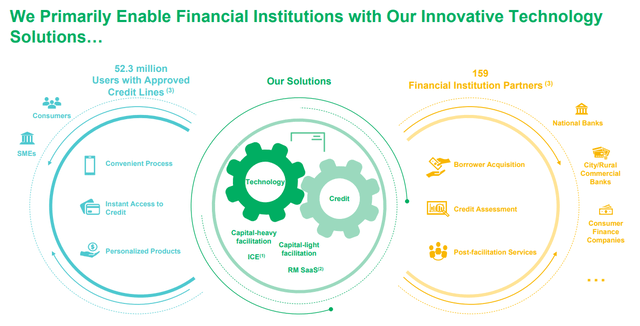

The cumulative number of users with approved lines of credit reached 52.3 million, an increase of 13.8% year-over-year. Within this amount, the actual number of borrowers of 31.2 million increased by 12.6% year-on-year.

The company found that repeat customers contributed about 92% of total loan volume in the first quarter. This metric indicates a certain level of brand loyalty and customer satisfaction, while also indicating winds of growth as a new group of new borrowers enter the platform.

The delinquency rate at 4.9% this quarter was up 4.1% from a year ago, but for context is still well below levels of more than 6% in 2019 as the pre-pandemic norm. The risk measure decreased from 5.0% in the previous fourth quarter. Management sees the current scope as expected, and is otherwise a normal part of the business.

In terms of guidance, the company is targeting adjusted net income for the second quarter between CNY1.22 billion and CNY1.28 billion, representing year-over-year growth of between 6.4% and 11.6%.

Efforts are to continue prioritizing risk performance and operational efficiency. This was a point addressed in translated comments during the earnings conference call from Qifu Technology CEO Haisheng Wu:

Since the second half of last year, we have made adjustments to our business strategies, focusing more on the overall profitability of our business and achieved good results…

Next, we expect Q2 buy rate to improve further with the main driving factors being: The first factor is improved risk. By reducing business with low or negative margins, we enhance the profitability of the overall loan portfolio. In addition, we will continue to improve the efficiency of the collection process, and we expect further improvement of risk indicators in the second quarter.

What’s next for Kivu?

The Chinese economy and related stocks have been a closely watched story in the first half of 2024. Despite some deep pessimism at the start of the year, recent economic indicators have provided some sense of stability in the region. Reports indicate that the authorities are moving forward with a comprehensive approach towards stimulus efforts to avoid a recession and also support the capital markets.

In our view, Qifu Technologies is well positioned to capitalize on this potential macro shift. The company proved capable of navigating a challenging operating backdrop last year, while tailwinds of new credit demand could be a catalyst for better-than-expected results.

In essence, an expanding credit platform with more borrowers and partner financial institutions has plenty of room to grow in the world’s largest economy. In many ways, there’s an argument that Qifu’s growth story has only just begun.

Source: IR Company

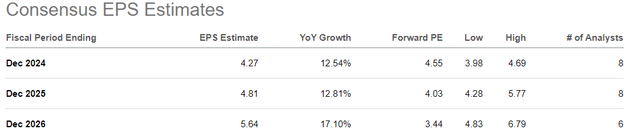

According to consensus, Qifu’s 2024 EPS is expected to be $4.27, up 12.5% from 2023, as a continuation of Q1 trends and Q2 guidance. The market is seeing an average earnings growth of about 15% between 2025 and 2026.

Of course, this path will depend on how economic conditions in China evolve over this period, but we argue that there is a path for growth to even beat expectations in a scenario where consumer credit rises.

The stock’s valuation, which trades at just 5 times forward earnings, appears low given the same China-related uncertainties and risks to the region. On the upside, the ability to continue executing on the strategy should allow the earnings multiple to expand as an additional catalyst for the stock.

Source: IR Company

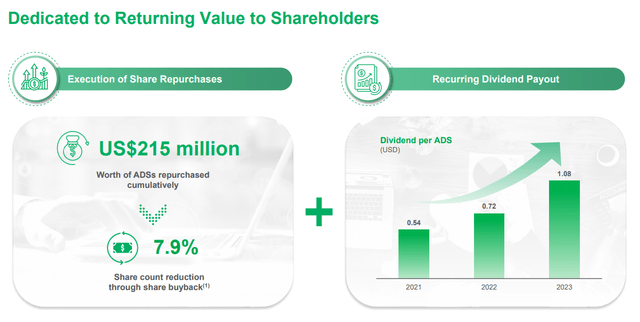

We mentioned the buyback of company shares and the distribution of dividends. According to the 2023 annual report, Qifu intends to announce a semi-annual dividend representing between 20% and 30% of net income as a payout ratio.

For context, the $1.08 distributed to ADS QIFU holders over the past 12 months corresponds to 28% of EPADS for 2023. With the final payment in May, investors can expect the next payment by November, following the trend of the year The past, although nothing has been confirmed. Based on the earnings trend, we can estimate the forward dividend yield at around 5.5%.

Separately, the company has been active in buybacks. In March, the board approved a new $350 million repurchase authorization. As of May 17, the company has already purchased $65 million worth of shares under the program. Given the stock’s current market cap of $3 billion, the implied forward repurchase yield on the remaining warrant is about 1%.

Source: IR Company

Final thoughts

Qifu Technologies ticks several boxes for what we consider to be a compelling investment opportunity. Steady growth, recurring profitability, a strong balance sheet and regular dividend payments make the stock one of the high-quality names outside China in our opinion.

Meanwhile, the risk to consider here is the potential scenario where economic conditions deteriorate, forcing a reassessment of earnings expectations. In China, there are shades of regulatory issues that cannot be overlooked in light of events in recent years.

However, a small position in stocks can make sense in the context of a diversified portfolio as a good option for exposure to Chinese consumer credit trends. We think the stock is attractive on a risk-adjusted basis.