RyanJLane/E+ via Getty Images

Investment thesis

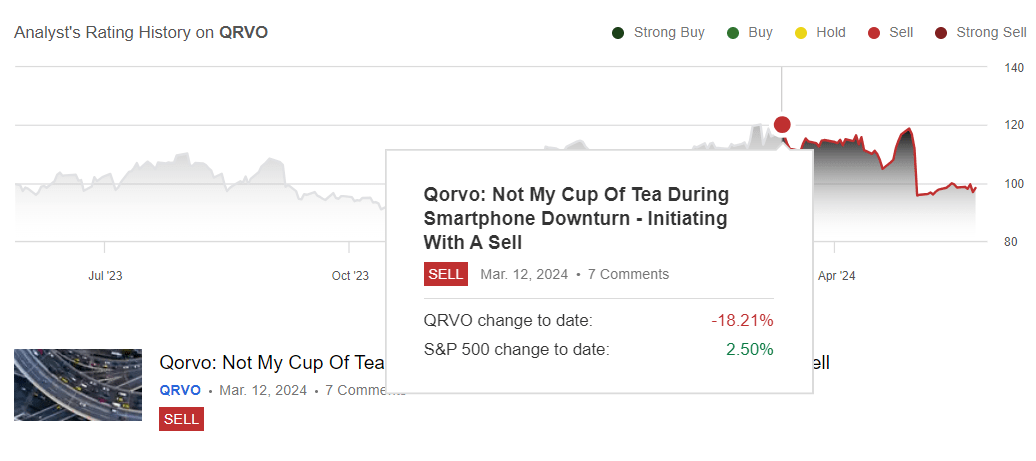

It’s been about a month since Corfu (Nasdaq: QRVO) announced its results and expectations for the fourth quarter of fiscal year 2024; Since my sell rating on Qorvo in mid-March, the stock has underperformed the S&P 500 by about 20%, as shown below. I’m updating My investment thesis Post-profit results to repeat my selling process. I think a lot of the bad news has already been factored into the stock price performance and management’s outlook for the June quarter, but I see more downside risks over the next quarter.

TheTechie – SeekingAlpha

The company reported March sales of $914 million compared to consensus expectations, which were slightly higher at $925 million. I view Qorvo’s Advanced Cellular Group sales as a measure of the company’s risk-reward scenario, and due to the lack of demand for smartphones this year I am less optimistic about Qorvo for 2024.

Total sales fell 12% quarter-on-quarter to $941 million compared to consensus expectations of $925 million. The company’s largest segment, Advanced Cellular Group, fell 23% QoQ to $654 million due to weak demand from the star of the smartphone market, Apple (AAPL) (AAPL:CA). Even Apple’s results this quarter failed to impress me. I think that although the market has reacted well, with Apple trading higher on the buyback results and news, the results have indicated no real recovery in final demand, which makes me considerably less optimistic about Qorvo’s near-term performance. To illustrate Qorvo’s exposure to the smartphone market, it is worth noting that for FY2024, Apple accounted for 46% of total sales and 37% in FY2023 and Samsung accounted for 12% of total sales in both years, respectively. Not to mention the additional risks Qorvo faces from competing in the 5G market against Qualcomm (QCOM), Huawei and others, which management addressed in the quarter.

Keep in mind that sales of Qorvo’s other segments grew; High-performance analog sales were up 38% q-o-q, and connectivity and sensor suite sales were up 13% q-o-q. However, I don’t think other segment growth (although double digits) is relevant to Qorvo’s performance as long as advanced cellular group sales remain weak. I think the administration would agree with me, given their point of view.

The company is guiding sales to decline another 10% quarter-over-quarter in the next quarter, which will be the first quarter of fiscal 2025, to $850 million, well below the consensus of $925 million. In particular, management expects sales of advanced mobile phones to decline by 8-9% QoQ due to weak demand from Apple and flat demand from China’s Android market. So, this reaffirms my pessimism when it comes to Qorvo’s near-term performance, specifically the company’s performance over the next Q1 and Q2. Management still expects the total addressable smartphone market, or TAM, to grow by 1% year over year and the 5G market by about 10% year over year for 2024.

What could go wrong?

There’s an argument that the stock is attractive at current levels because management has been so negative for the upcoming quarter. Aside from the expected decline in its advanced cellular sales, management also expects a decline in high-performance analog sales (by 11-12% QoQ) and flat sequential growth for connectivity and sensor sales. Bad news is recognized by management and the market. Why are you still pessimistic? I think there is limited upside this year as I cannot see any near-term catalyst that could reverse the situation for 2024 to revive eventual demand for smartphones. I think other players with similar exposure, such as Skyworks (SWKS), are pointing to the same thing. I also think that part of the disappointment in this quarter was based on the fact that the market has been positive about the 2024 smartphone recovery since the second half of last year, and therefore, was already priced in with some of that optimism. So I think the results will continue to be disappointing in the near term.

evaluation

Qorvo shares are undervalued, based on the relative stock valuation methodology within the company’s peer group. The stock is trading at a price/earnings ratio of 16.3, while the average peer group ratio is much higher at 31. The same is true for 2024 EV/sales. The stock is trading at a ratio of 2.7 compared to an average ratio of 7.1, as shown in The table below, which was created using data from Refinitiv. The valuation is attractive compared to companies within the peer group with similar exposure to the smartphone market and Apple, especially Qualcomm and Skyworks, but I don’t think the valuation is enough of a reason to buy the stock on weakness if there’s no catalyst on the horizon to boost growth in the near term. My predictions of a lack of growth during the first half of 2024 came true, and now I expect to see the same for the rest of 2024.

Image created by Techie using data from Refinitiv

What then?

I believe Qorvo will continue to struggle to grow its earnings in the near term, specifically over the next Q1 and Q2. I expect to see further physical recovery in 2025 as smartphone TAM is expected to grow further year-over-year, and management pegs 2025 final demand growth with Apple’s expected sales growth over FY 2025 and FY 2026. I advise investors to keep an eye on Apple’s results In the coming quarter and advanced Qorvo cellular range sales to better determine the moment of recovery and leap forward. I don’t expect that turning point moment to happen in 2024, although I think the stock would be more attractive if it fell near its 52-week low of ~$80.62. The reason I don’t see this moment repeated this year is not only due to weak orders from Apple but also due to the inventory cycle impacting Qorvo’s margins. The company’s non-GAAP gross margins declined to 42.5% this quarter and are expected to decline again next quarter to the 40-41% range due to a higher mix of high-cost inventory. I expect Qorvo to underperform among its peer group compared to a live performance at best for the year.