We/DigitalVision via Getty Images

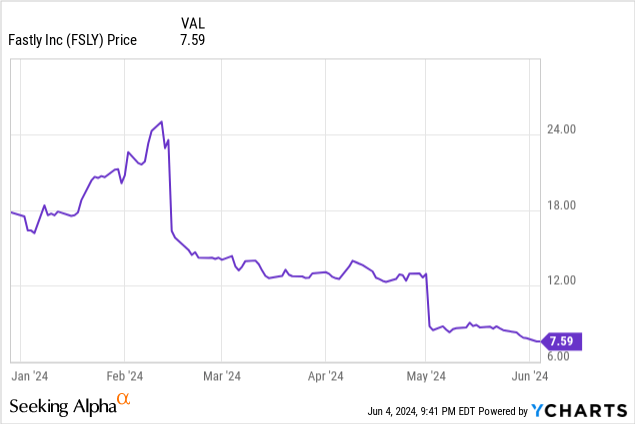

In an extremely challenging operating environment for small and midcap stocks, Fastly (New York Stock Exchange: FSLY) He has witnessed a world of hurt. The content delivery network (CDN) platform, which was once one of the hottest deals on Wall Street during the pandemic when it commanded a double-digit revenue valuation Multiples, has seen its stock price fall nearly 60% year to date. Compared to its pandemic-era highs that briefly topped $100 per share, Fastly has wiped billions off market value over the past few years.

The company recently released first-quarter earnings combined with a significant reduction in revenue guidance for the current year, causing the stock to decline even further.

Fastly is lowering expectations now to leave room to outperform in the near future

I wrote the last bullish article on Fastly in April, before the company’s Q1 earnings failure. While I admit now That my buy call was premature, and after observing the company’s first quarter print wreck, I think there is a lot of salvage value for investors to recognize in this stock.

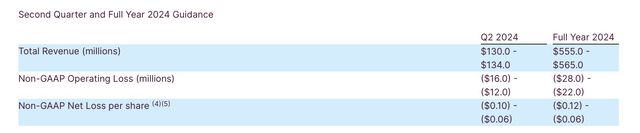

Let’s cover the issue first: The company lowered its full-year guidance forecast from a previous view of $580-590 million (15-17% YoY growth) to just $555-565 million (10-12% YoY growth). ).

Update forecasts quickly (First quarter earnings announcement soon)

It goes without saying that cutting growth forecasts by five points would be a big swing. But we note that it’s not uncommon for companies to take one “big” quarter to reset expectations at very low levels, and then chart a course to outperform going forward. We also note that Fastly’s stock price is down roughly 40% since earnings forecasts (or a loss of more than $600 million in market cap) versus a roughly $30 million drop in revenue forecasts for the current year – which appears to be an overreaction.

Fastly attributes the slowdown to declining traffic trends at the company’s largest enterprise clients. Meanwhile, traffic is an input that is largely outside of Fastly’s control — it relies on users like you and me clicking through to sites and submitting content requests to be processed through Fastly’s network. From my perspective, this weaker traffic appears to be seasonal and macro-driven in nature, rather than a failure of execution on Fastly’s part.

But that doesn’t mean Fastly isn’t taking steps to right the ship. Fastly is undergoing a leadership shake-up, including the search for a new CEO. We also note that the company has just hired a new Chief Revenue Officer, a long-time software industry executive with thirty years of experience primarily in cybersecurity, to demonstrate its commitment to getting its sales processes right.

Short-term volatility aside, here’s a reminder about my long-term bullish outlook for Fastly:

- Usage-based pricing may take a hit quickly now amid weak traffic, but it also allows for expansion when traffic recovers. Since Fastly’s pricing is based on the volume of content delivered, as core customers continue to grow their websites and traffic, Fastly’s revenues will also grow proportionately. Amid the deteriorating NRR of many of its tech peers, and even amid the company’s reports of traffic slowdowns, we’d like Fastly’s trailing NRR to remain above 110%.

- Customer growth and diversification The company now has a base of approximately 3,000 clients, including approximately 500 enterprise clients. It no longer relies on single large clients (before 2020, TikTok was a major driver of the company’s revenue).

- Economies of scale and now achieves positive adjusted EBITDA. As Fastly grows, it achieves economies of scale on its CDN. It has already begun cutting back on hardware spending in an effort to improve gross margins. Capital spending as a percentage of revenue is also expected to continue the downward trend. As Fastly’s existing customer base continues to drive usage, profit margins will continue to expand.

Stay Long Here: In my view, a lot of risk has already arisen from Fastly’s stock price, and it has a greater chance of downside.

Download Q1

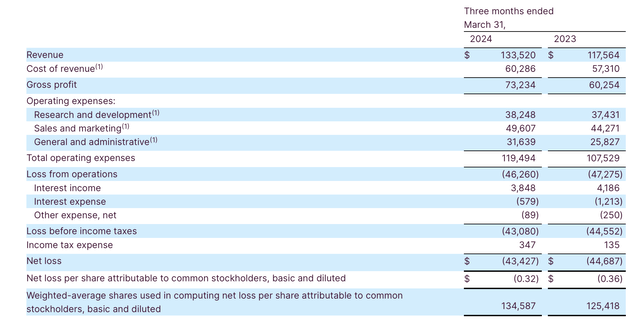

Let’s now review Fastly’s latest quarterly results in more detail. The first quarter earnings summary is shown below:

Q1 results quickly (Q1 earnings announcement soon)

Revenue in the first quarter grew 14% year over year to $133.5 million, slightly below Wall Street expectations of $133.8 million but barely slowing from the fourth quarter’s pace of growth of 15% year over year.

As previously mentioned, top line weakness in the quarter was dominated by weaker traffic trends at the company’s largest enterprise customers. According to CEO Todd Nightingale on the first quarter earnings call:

There are some factors that have contributed to a challenging environment in the short term. The biggest factor is declining revenue from a small number of our larger customers. Q1 revenue from our top 10 clients decreased from 40% to 38%.

Many of the top 10 accounts run a multi-vendor strategy. We have seen huge fluctuations here. There are several reasons for this. First, historically, Fastly has gradually captured a greater share of traffic in our largest accounts. But with the timing of price and volume changes, we saw increased volatility during the quarter. To be clear, we have not been excluded from any of our largest clients, and we will remain in a strong strategic position, for each of them, over the long term.

Second, by some accounts, we’ve seen the addition of CDN vendors or a reversal of the vendor consolidation we saw last year. Third, we are seeing a slight uptick from the typical level of re-pricing with our largest customers, but we have not yet seen the commensurate expansion in traffic typically associated with that traffic.

Very positively, we’re seeing continued success in our new customer acquisition movements and, in particular, we added two very big new logos in the first quarter, one of which will move into the top 10 throughout the year. We aim to see the long-term results of our new customer acquisition traffic have an increasing impact on our revenue as the year goes on.”

The final points made by Nightingale above are crucial. Despite the decline in traffic in its existing customer base, the company is still seeing better-than-expected new customer acquisition – which, over time as those customers fully come on board, will help offset weaker trends in the existing base. The company noted the addition of 18 new enterprise customers in the quarter (including the “two new very big logos” mentioned above) as well as 47 new customers overall in the quarter, bringing the number of customers to 3,290.

Second, we also note that USD retention rates were 114% in Q1, which suggests that despite all this weakness in traffic, the average customer is still expanding at about 14%. This improved slightly from 113% in the fourth quarter.

We also note that profitability is about to turn around.

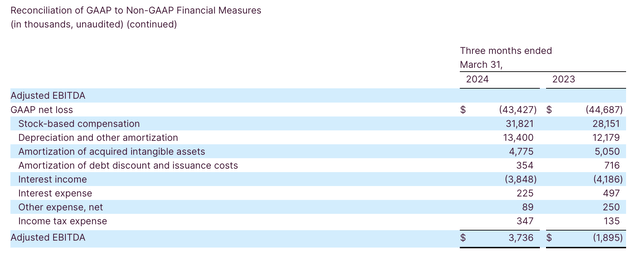

EBITDA adjusted quickly (First quarter earnings announcement soon)

As shown in the chart above, Adjusted EBITDA increased to $3.7 million in the quarter, representing an Adjusted EBITDA margin of 3%, versus an Adjusted EBITDA loss of – 2% in the first quarter of last year.

Risks, assessment and key takeaways

At current post-earnings stock prices of close to $8, Fastly trades with a market cap of just $1.04 billion; After we liquidated $329.5 million in cash and $343.8 million in debt in Fastly’s most recent balance sheet, the company’s results Enterprise value: $1.05 billion.

This puts Fastly’s rating at 1.9x EV revenue/FY24. Even with lower growth expectations, with Fastly just starting to post positive EBITDA as well as coming off a strong win with the new logo, I’d say this is a pretty low multiple.

There are a ton of risks here, of course – which is exactly why the stock is down so hard. Winning operations with a new logo can slow down, and new processes implemented by a new revenue manager may fail. Competition against other CDNs may cause Fastly to lose more share and suffer deeper traffic declines.

But in my view, all of this is already priced into Fastly’s lower post-earnings price. In my view, it’s time to pick up the pieces here.