Evening pictures

summary

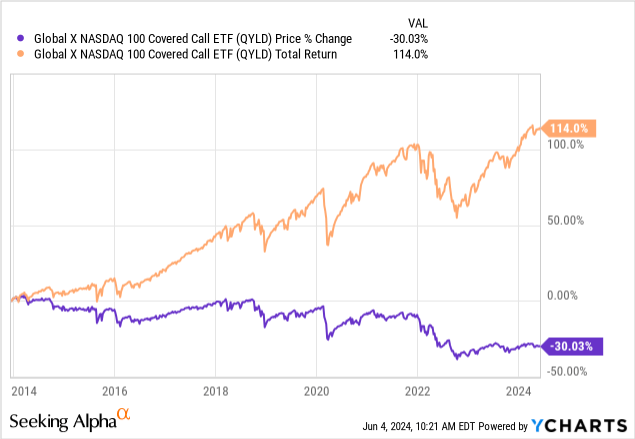

Covered ETFs make it possible to collect very large returns from relatively small investments. This makes them popular asset classes among investors who value income. GlobalNasdaq:KLD) offers a very high dividend yield of over 11% while providing exposure to the best companies in the world. However, the inclusion of an option strategy leaves some weaknesses that investors should be aware of. As a result of these weaknesses, the price has consistently traded in a downward trend over time since its inception in 2013.

QYLD is actively managed by Global X Management Company and has total net assets of $8.15 billion. The fund’s expense ratio is very reasonable at 0.61%. QYLD seeks to provide a total return that is consistent with the price and return performance of the Cboe Nasdaq 100 BuyWrite V2 indicator. QYLD writes call options on the Nasdaq 100 Index and gives investors the opportunity to let professionals handle this strategy, rather than incurring the expense of implementing similar options strategies yourself.

Although the price is down over 30% since inception, the high dividend makes up for it. Including the dividends, we find that the total return from the beginning is 114%. Therefore, I believe a fund like this would be best used by an investor who is in or approaching the retirement phase of his investment journey. This is because these investors likely have a much higher priority on generating income that can be used to fund lifestyle expenses. Before getting into the best way to use QYLD, let’s first take a look at what the fund holds and what the option strategy entails.

Strategy and weaknesses

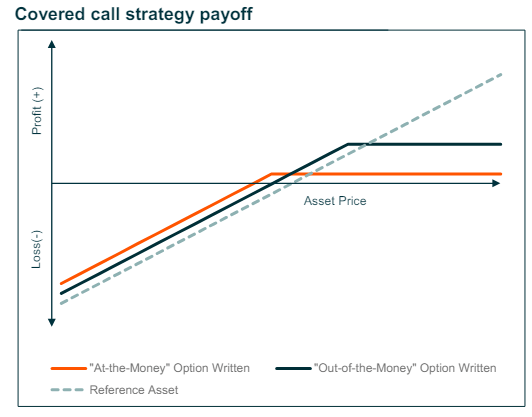

QYLD’s strategy is to generate income by writing covered calls. During periods of extreme volatility, the income generated actually grows. This is usually because higher volatility can produce higher premiums that investors can earn from selling a call option. However, this covered call strategy has some limitations, the most notable of which is that an upward movement is determined if the value of the underlying asset rises above the strike price.

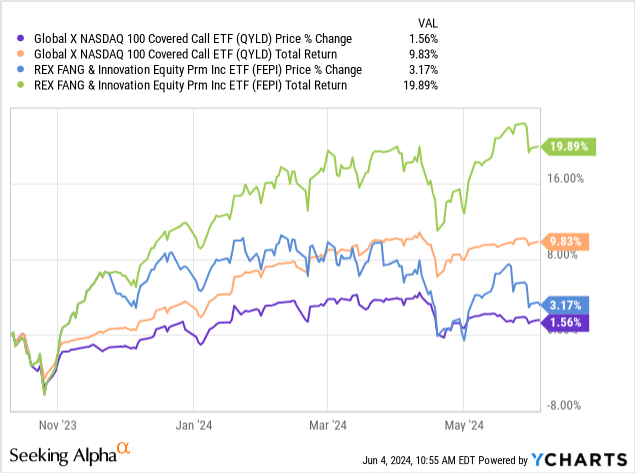

This is because QYLD implements an “at the money” communication strategy rather than an “out of the money” strategy. In money strategies, you leave no barrier until the uptrend of the price is captured. A good example of this is the different strategies between QYLD and the REX FANG & Innovation Equity Premium Income ETF (FEPI), which use out-of-the-money call options. The visual below is a great representation of how different strategies affect returns.

QYLD offer

FEPI has a very short history, with less than a year of price movement. However, the difference in strategy makes a dramatic difference in price performance even though the two funds implement covered call strategies. We can see that FEPI has repeatedly delivered greater returns, which contributes to FEPI’s outperformance in total return. This is the main disadvantage of the in-the-money option strategy. You are essentially losing the upside potential while also remaining exposed to all of the downside risks of the index that QYLD tracks.

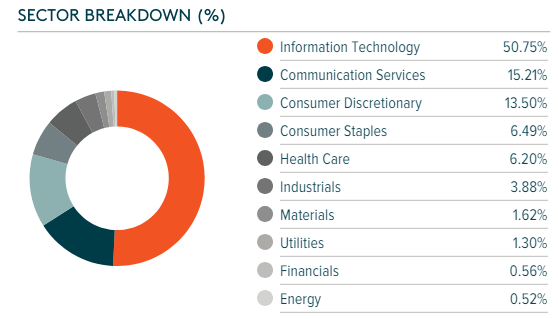

Despite the strategy’s shortcomings, QYLD is diversified in nature but has a fundamental weighting towards the technology sector. The technology sector is usually more volatile than others due to the fastest growing companies within it. As a result, QYLD is able to easily generate income from the option strategy. We can see that technology accounts for about 50% of the weight of the fund. Followed by communications services at 15%, then consumer discretionary services at 13.5%. There are a total of 102 sole proprietorships within QYLD.

QYLD Fact Sheet

Since the top sector consists of technology companies, we can expect the largest holdings to be in some of the most well-known companies in the world right now. The top five holdings include companies such as Microsoft (MSFT), Apple (AAPL), Nvidia (NVDA), Amazon (AMZN), and Meta Platforms (META). While this is great for capturing volatility to generate income, I can’t help but feel that focusing on holdings on the inside is a bit pointless since no upside movement is recorded anyway. However, this diversified group of holdings helps mitigate exposure to any sector-specific risks, especially technology.

Dividend

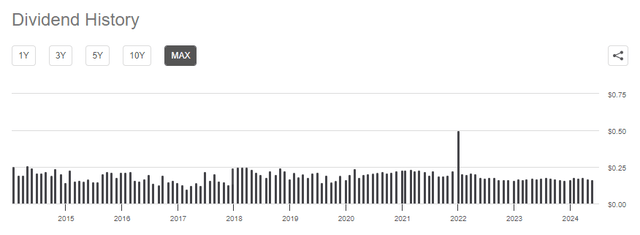

As of the most recently declared monthly dividend of $0.1628 per share, the current dividend yield is approximately 12%. This focus on monthly distributions makes QYLD a very attractive fund for investors who prioritize income. Taking a monthly distribution can help fund lifestyle expenses or can be integrated into other areas of your portfolio that may be better value. However, the distribution is directly linked to the fund’s performance, so the amount received may vary on a monthly basis.

Seeking alpha

We can see that dividends have remained around the same range throughout the fund’s history. After the pandemic collapse in 2020, market volatility increased and payouts rose slightly. However, you are unlikely to see any growth here with the dividend over a long period of time. So, if you’re an investor looking for a more traditional form of dividend growth over time, QYLD is not for you.

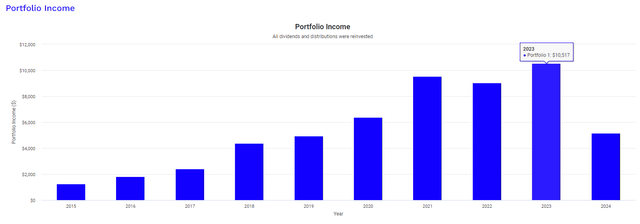

However, this does not mean that there is no way to increase your dividend income. In order to see any meaningful growth in dividend income here, you must essentially create your own income with ongoing contributions and full or partial reinvestment of your distribution. Using the Portfolio Visualizer, we can show exactly how this could have gone down over the past decade. This picture assumes an original investment of $10,000 in 2015. It also assumes that $500 is added to your position on a monthly basis and profits are reinvested over the entire holding period.

Portfolio visualizer

In 2015, your total dividend income was just $1,237. Fast forward to 2023, your dividend income would have grown to over $10,500 per year while your position is now worth around $108,000. This scenario would be ideal for someone preparing to retire in the near future. By starting the trade now, you will have some time to build a significant income stream over time. However, I also want to point out something I noted in QYLD Notice 19A. More than 96% of the distributions issued this year were a return of capital.

QYLD Notice 19a

When it comes to closed-end funds, the return of capital can be detrimental because it means the fund is not earning enough income to defray distribution costs. However, with covered ETFs like QYLD, this return of capital is merely a tax deduction as a result of the income generated from the option strategy and is not detrimental in this case.

Best use case and outlook

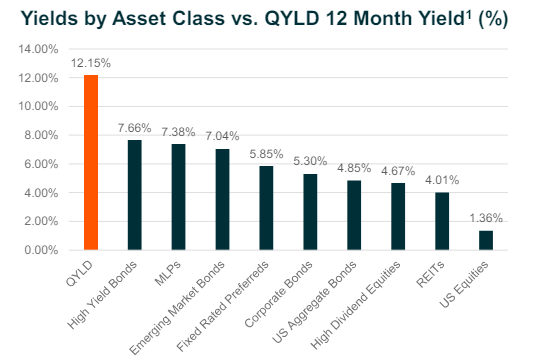

So what type of investor is best for QYLD? In my opinion, QYLD would be better complemented by a range of other asset classes that could offset the price deterioration it has seen. While the returns from covered ETFs like this are generally still higher than other asset classes like high-yield bonds, MSEs, REITs, or traditional stocks, it wouldn’t be wise to have a fund like QYLD It makes up the largest percentage of your portfolio. .

QYLD offer

The unique use case for a fund like QYLD is that dividend-focused investors may be able to increase the return of their portfolio while simultaneously filling any diversification gaps. When I started my dividend investing journey a long time ago, I made the mistake of focusing too much on companies like Dividend Aristocrats and Dividend Kings. These companies are usually within the utilities, consumer, industrial and energy sectors. Although this is a good place to start, these companies usually do not involve any exposure to technology. Technology isn’t exactly known for its strong dividend yields or earnings growth, so I naturally built a portfolio that had high levels of income but lacked proper diversification across industries.

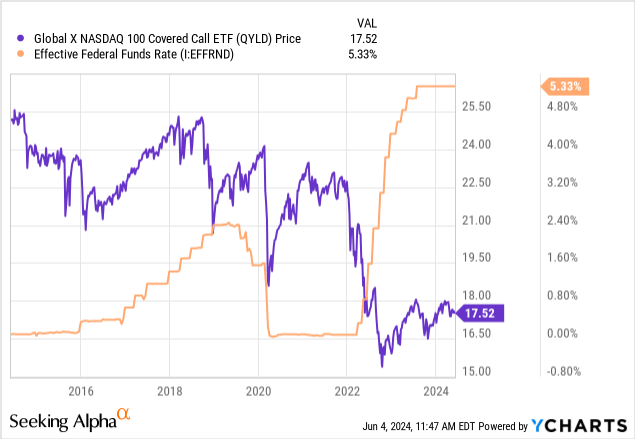

As mentioned earlier, covered ETFs like QYLD benefit from higher levels of volatility. With this in mind, I think there are a few different factors that will continue to provide favorable volatility levels for QYLD to benefit from. To begin with, there are still ongoing talks about interest rate cuts. With every Federal Reserve meeting, the market shows us that it is still very reactive. Interest rates started rising rapidly in mid-2022, and we can actually see QYLD struggling to gain any upward momentum since then.

With the unemployment rate remaining below 4%, inflation remaining high, and interest rates rising, I believe that any talks about lowering interest rates in the future will lead to more volatility. The Fed appears to be slowing down and waiting for more economic data to emerge as the months go by. Therefore, there is a possibility that interest rate cuts will not actually happen until next year. Additionally, we have the US presidential election on the horizon, which historically has always created higher volatility in the markets. This volatility can be attributed to the uncertainty represented by the election. So, I think the higher level of income from QYLD will be able to continue throughout the remainder of 2024.

Away

QYLD’s Covered Call Strategy is a great way to add some extra income to your portfolio with its options strategy. However, using at-the-money calls leaves vulnerabilities as you are putting a limit on the potential upside while also facing the full impact of downside risk. I believe that out-of-the-money covered ETFs like FEPI serve as a better alternative option to ETFs. Despite its weaknesses, QYLD has its own use cases and ultimately provides exactly what it intends to do, which is generate high levels of income. Monthly distributions are still able to provide a high level of total returns that offset price deterioration.

The dividend yield is still at around 12% and I think it can be maintained throughout the rest of the year. Covered ETFs thrive in a highly volatile environment, and that is exactly what we are likely to experience throughout the remainder of the year in my opinion. As talks about lowering interest rates continue and the presidential election approaches, I believe this will create a lot of uncertainty in the markets which will lead to volatility.