Radical Overhaul: Q3 Earnings Still Show Huge Challenges, Rally Unwarranted (NASDAQ:SFIX)

MoMo Productions/DigitalVision via Getty Images

Stitch Fix, Inc (Nasdaq: SFIX) is an online clothing retailer. The company is known for its innovative subscription box system, where customers subscribe to receive a box (called FX) with pieces of their choice. The designer can later decide which ones to buy and which ones to return.

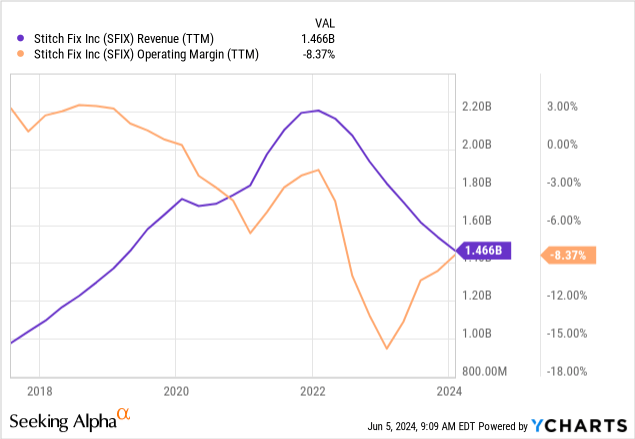

This article discusses the company’s Q3 2024 results and earnings call. The results were not good, with active customers down 20% year over year, revenue down 13% year over year, and an operating loss of $25 million (-7.7% margin). However, results were expected to be worse, and thus, SFIX beat the consensus, leading to a rally with the stock opening 35% higher.

I began covering SFIX in March 2024 with a Hold rating. The reasons for the suspension were the company’s ongoing operating losses (masked by massive amounts of stock-based compensation) and the fact that it was The model appears to face fundamental challenges.

After the results, I don’t think the fundamentals have changed. The stock price is up about 50% from my last article, so the valuation (adjusted for the massive dilution resulting from stock-based compensation, or SBC) is still unattractive. I think SFIX is still pending.

Not great results in the third quarter of 2024

SFIX posted negative results across all income statement lines (year-over-year): revenues fell 13%, customers fell 20%, gross profits fell 11%, and operating losses rose 21%. EPS for the quarter was -$0.18, up 12.5% (negative).

However, the stock rose after the results were announced. The reason is that the results were less bad than expected, as the company beat revenue, earnings per share, and high guidance.

SFIX has posted terrible results for more than two years, with revenues and customers declining post-pandemic. The company was never operationally profitable after the pandemic.

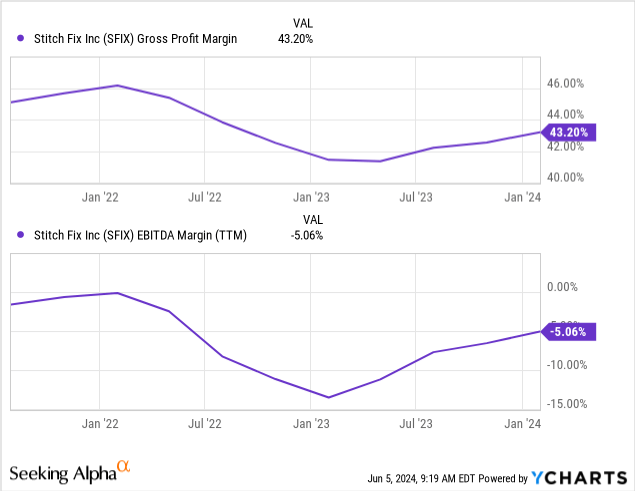

There were some positive data points. First, gross margins rose about 300 basis points year over year, driven by freight costs. Second, average customer revenue increased by about 2% to $525. These numbers may indicate that the customers SFIX is losing are the least profitable customers. In my previous article, I commented that SFIX could be profitable on a smaller scale without a lot of low LTV clients. Third, SG&A declined 7% year over year, reducing the company’s high fixed cost base.

Repair the model

In my original coverage article, I commented on the challenges of the SFIX model. The main challenge is that SFIX’s target customer (the person who cannot afford the clothes themselves) is not interested in the clothes to begin with, which means the customer has a low lifetime value. This results in a lot of hype, which implies a heavy reliance on advertising. This problem was exacerbated by high fixed investments in employees and distribution centers, which required volume justification, resulting in an increased need for advertising.

The current CEO team has been with the company for a year. During that period, the company was restructured. This includes design staff being laid off, design staff moving from full-time to part-time to avoid paying benefits, and leaving the UK market. The goal was to reduce the fixed component of costs to make SFIX profitable on a lower scale. Gross margins and EBITDA margins improved.

The new CEO also commented on reimagining the customer experience. The 1Q24 call mentioned developments in this regard.

For example, the company has reduced the number of customers to whom it offers Quick Fix, which is a smaller batch in addition to the usual batch of five pieces. The quick repair was causing losses for many customers due to the cost of sending some parts back and forth. The company made the product more profitable by reducing the number of customers to whom the product was offered.

Another change mentioned is merchandising, where algorithms help make inventory decisions. Inventories are down 20% year-over-year, and a recovery in gross margins suggests there has been less promotional activity, indicating better marketing decisions.

During the call, the management discussed the possibility of changing the number of pieces sent in the fax to different types of customers and increasing communication between customers and designers. These model changes may increase customer lifetime value, which is key to making SFIX profitable.

The valuation is still unattractive

In my previous article, I adjusted the company’s published market capitalization to take into account the massive dilution resulting from SBC (which amounted to $20 million in the last quarter alone). This dilution is not calculated today because the company is generating losses, so more shares would be anti-dilution. However, if the company becomes profitable, the number of diluted shares will suddenly increase. As of Q4 2024, the company’s shares, including all options and RSUs, are approaching 325 million. The number will likely be higher as of the third quarter of 2024, but the 10-Q number has not yet been published. At a share price of $3.5, SFIX has an (adjusted) market cap of $1.14 billion.

SFIX also has $245 million in cash and no debt. This was made possible by SBC, despite huge operating losses (over US$100 million). Therefore, the value of the company’s (modified) electric vehicle is approximately $892 million.

Against this valuation, SFIX provides FY24 guidance of approximately $1.33 billion (down 19%) and adjusted EBITDA of $25 million to $30 million. Considering a TTM D&A of $40 million and a TTM SBC of $90 million, this would still represent an operating loss of $105-110 million.

So, adjusted for future dilution, the SFIX valuation is an EV/adj-EBITDA multiple of 32x at the midpoint of guidance. There is no EV/EBIT or P/E multiple because the company is still largely unprofitable. Losses are decreasing (operating losses last year were $170 million), but that’s mainly because the company has cut costs, not because it’s increased its bottom line or gross profits. I think challenges to the corporate model still exist.

Conclusion

SFIX is restructuring its operations to reduce fixed costs and improving its model to increase customer lifetime value. These moves address my three main concerns about the company’s model: customer lifetime value is low, churn is high, and the company has a high fixed cost base that requires scale.

Q3 2024 results showed some signs of improvement on these fronts: lower SG&A, higher gross margins, and higher average customer revenue. Unfortunately, Stitch Fix, Inc. is still… They quickly attract customers, lose revenue, and generate huge operating losses.

I think all this does not justify the company’s recent rise. When adjusted for potential dilution, the company’s EV/adj-EBITDA of 32x appears exceptionally high for a company that is losing revenue at a rate of 13% year over year and has not demonstrated that it can operate profitably.

So, I think Stitch Fix, Inc. stock is… Not an opportunity at these prices and maintains my Hold rating.