zoranm

Consumer goods maker Reckitt Benckiser ( OTCPK:RBGLY ) has had a bumpy few months.

I last covered the name in November, with my article Reckitt Benckiser: Not a Bargain Despite Its Potential. Since then, London stocks have fallen 17%. This is even after a 10% rebound over the past two months.

At this point, I changed my rating from “Hold” to “Buy” and have actually purchased some shares for my portfolio over the past couple of months.

Main investor concern

The main reason for the stock’s decline this year is, surprise surprise, concerns stemming from Lernaean Hydra in the feed business. As many plots in recent years attest, this has been a source of significant problems and huge losses for the company since its 2017 acquisition from Mead Johnson.

In March, there was news of a negative ruling in an Illinois state court, with many other cases pending. A March notice to an Illinois court awarding $60 million to a plaintiff in connection with necrotizing enterocolitis. Reckitt’s statement stressed that this was an individual ruling, and the company said it would “pursue all options to overturn it.”

Compare that with the statement in its final results published two weeks ago (emphasis mine):

Product liability claims involving NEC have been brought against the Group, or against the Group and Abbott Laboratories, in state and federal courts in the United States. The proceedings allege NEC-related infections in premature infants. Plaintiffs assert that human milk fortifiers (HMF) and preterm infant formulas containing bovine-derived ingredients cause NEC, and that preterm infants should receive a diet consisting exclusively of breast milk. The company denied the material allegations contained in the claims. It emphasizes that its products provide important tools for expert neonatologists for the nutritional management of premature infants for whom human milk, by itself, is not considered nutritionally adequate. The products are used under the supervision of doctors. Any potential costs related to these procedures are not considered probable It cannot be estimated reliably at this time.

The stock price decline we saw in reaction to the Illinois ruling reflects the potential cost of such broader litigation and, I suggest, investor concerns that management may not have fully appreciated the risks.

Shares are down significantly, but for now we have yet to see the final cost of the issues, and investors have been trading rough numbers that vary widely. Barclays analysts believe that £2 billion would be the “very worst-case scenario” and that between £100 million and £400 million is more likely.

While Reckitt has pledged to fight these cases, it is difficult to imagine a scenario in which the company would not bear some eventual cost, even if only to settle the lawsuit without admitting liability.

But in the long term, I think even a £2bn loss (essentially the company’s free cash flow for a year) is manageable and not worth the kind of share price reduction we saw after the ruling.

Business performance is good, not excellent

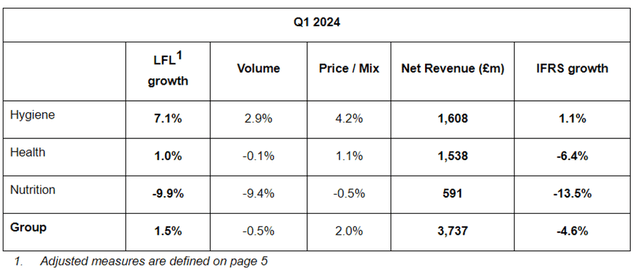

In April, the company issued a first-quarter business update. The headline “Good Q1 performance, on track for full year delivery” doesn’t seem accurate to me, or at least if the decline in both volume and net revenue is viewed as “good”, I don’t want to see what management might consider As a bad performance. Part of the blame was placed on foreign exchange rate movements.

In my opinion, the health department is not working very well, unlike the hygiene department, but the big challenge remains the long and problematic feeding arm of the company. I’ve addressed in my previous analyses why this is a problem, and it remains the case.

Overall, this quarter’s results looked disappointing to me, with both the health and nutrition businesses showing declines in volumes, although in the case of the health division at least, this was offset by price and mix changes.

Company’s first quarter trading update

The company based its nutrition performance on strong comparisons to the previous year, due to competing supply problems at that stage.

The company is entering into the third tranche of a £1bn share buyback programme, which it expects to complete in July.

Reckitt reiterated its full-year outlook, which ranges from 2-4% as net revenue growth and adjusted operating profit growth before net revenue growth, with the year’s performance weighted for the second half.

Overall, I think the update confirms what we’ve seen at Reckitt in the past couple of years: the former growth machine has transformed into a company that needs to work hard to stay afloat. Overall, I was able to do it. It still has a strong stable of brands and is more strategically focused than it has been in nearly a decade, in my opinion, so the fundamentals remain in place for future success.

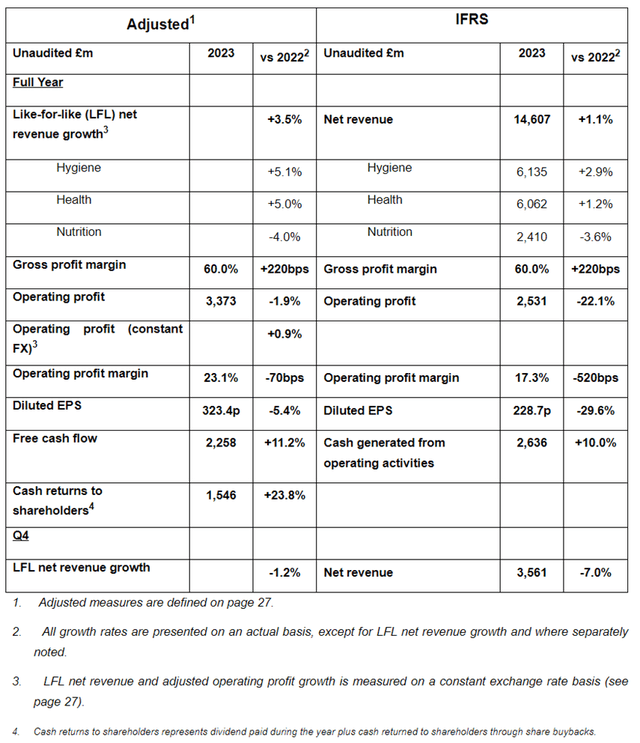

This was in addition to last year’s full-year performance which could be described as workable rather than strong given the ongoing inflationary environment (although free cash flow performance was strong).

Announcement of final results

But it’s important to remember that Reckitt’s hygiene brands have thrived during the pandemic, and they continue to show growth in two of their three divisions despite that higher base. Revenues last year were 14% higher than in 2019, for example.

So, while the business doesn’t have a very exciting feel about it at the moment, I think the stage is set for a strong performance in the coming years. I think Reckitt’s forecast of 2% to 4% net revenue growth for the current year is nothing to scoff at, especially in light of its ongoing nutrition issues (where it expects a moderate to high net revenue decline this year). Weak economies in many markets are putting pressure on demand for high-priced consumer products with premium brands.

Scuttlebutt negative

I’m not a regular user of Reckitt’s product but I recently bought a tub of their Vanish detergent from a Spanish store. I was disappointed to discover that the large container was barely half full. Some compromise can occur in transportation and there is usually a limited range of container sizes used to reduce complexity, but the low level of packaging really spoiled my view of Vanish and Reckitt as a consumer.

I don’t know whether this is an unusual case or a symptom of the broader approach to dealing with the shelf effect by the company. However, I dare say it has negatively impacted my view of the company, and in the long run, letting shoppers feel short change is rarely a way to thrive.

I purchased at what I consider to be an attractive valuation

But while recent business performance has been mixed and the prospect of food liabilities is indeed a risk, I feel the share price has been overly punished. I have been buying shares in the company over the past few months and am upgrading my rating to Buy.

Currently, the P/E ratio is 14. Compare that with 20 for UK peer Unilever (UL) and 25 for US Procter & Gamble (PG). I think there is still some reduction in the uncertainty surrounding Reckitt in the wake of the US ruling (although this has decreased in recent months) as well as the company’s overall lackluster performance of late.

But let’s not overdo it. The company owns a portfolio of very popular brands with significant pricing power, such as Lysol and Durex. Last year’s revenues were the highest ever. The company made profits of £1.6 billion after deducting tax. Adjusted free cash flow last year was £2.3 billion. Net debt is still higher than I would have liked, but last year it fell to £7.3bn. This means that Reckitt has an enterprise value of less than £40bn. I think this looks like good value for a company with its brand assets and proven long-term profitability, even taking into account the legal uncertainties.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these stocks.