Righetti Computing: Should benefit greatly from Novera’s (NASDAQ:RGTI) partnership program.

john d

Founded in 2013, Rigetti Computing Company (Nasdaq: RGTI) is a company that develops integrated supercomputer services available through its cloud platform, Forest.

After going public via a SPAC deal in 2021, the stock’s performance has been disappointing thus far. Trading at around $9 At its level at the time, the stock has lost -89% of its value since then. Currently, RGTI is trading at a price level of $1. However, RGTI has gained some momentum since the beginning of the year, with the stock up about 16% year to date.

I rate the stock a buy. The one-year price target is $1.4 per share upside by approximately 35%. At this level, RGTI represents a good buying opportunity. In my opinion, the launch of the recent QPU Partnership Program will greatly benefit RGTI, allowing it to open up and seize greater opportunities in the quantum computing industry in many ways. The risk reward looks attractive.

Financial reviews

YCharts

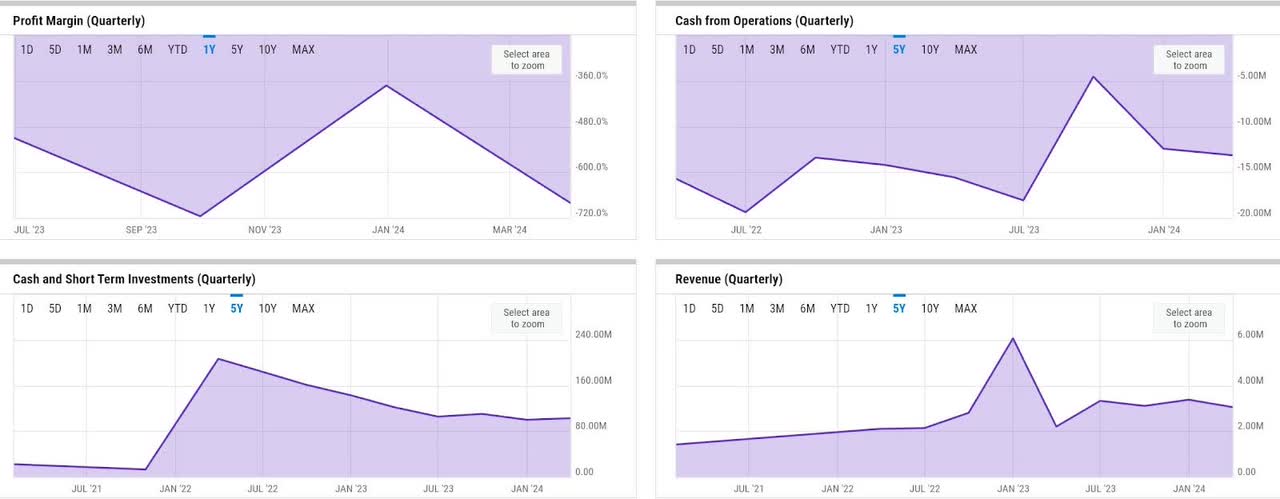

As is the case with any company developing a new and highly innovative technology, I consider RGTI to be at the investment stage today. In the first quarter, RGTI generated revenues of more than $3 million, a 39% year-over-year growth. Its revenues are primarily based on technology development contracts and QPU sales. As an investment stage company, RGTI spends a lot on R&D. In fact, R&D spending was more than three times its revenue as of the first quarter, leading to an operating loss of $16.5 million in the quarter. However, the operating loss and net loss narrowed by -25% and -10% in the first quarter, indicating a significant improvement there. Continuing losses have led to increased negative operating cash flows (OCF). Although OCF’s losses have also narrowed in the past five years, RGTI still looks some way away from turning cash flow positive. This has put pressure on liquidity since going public, although the level of liquidity has remained relatively stable recently. In the first quarter, RGTI saw a slight increase in liquidity, having ended the quarter with more than $102 million of cash and short-term investments. Primarily, a $20.7 million cash infusion from the issuance of common stock helped RGTI boost liquidity in the first quarter.

Catalyst

In my opinion, the recently launched Novera QPU Partnership Program should stand RGTI in good stead to not only develop the quantum computing industry further but also drive more QPU sales in the future.

Presentation to the company

Since the quantum computing industry is still at a very early stage, I believe that the approach of developing the ecosystem through partnerships to promote technology development across different parts of the stack is a strategic move. Firstly, it must establish RGTI as a leading name in this space, which will also allow it to be in a position to secure a dominant market share in the future.

Second, as management commented in the first quarter earnings call, partnerships will allow the industry to advance further and faster. This may be due to the fact that quantum computing is a complex technology that requires deep focus on a specific part of the stack to achieve continuous improvements more quickly:

We fundamentally believe that an open standard approach is the right way to allow innovation to come in faster. Therefore, we allow other partner companies to develop what they are good at. For example, we partnered with Riverlane in Cambridge, UK, which is a very good company at debugging. We have partnered with Quantum Machines in Israel and Zurich Instruments in Switzerland, who are very good at control systems. So, we allow our QPU to interact with other parts of the stack from other companies. We believe this is the right approach to develop a quantum computing system in a faster and more efficient way.

Source: Q1 earnings call.

Last but not least, I believe the success of the partnership program should indicate future revenue growth, since the obvious early adopters of a quantum computing solution within the company will be one of the partners in the program. In Q1, we saw this happen when RGTI sold Novera QPU to Horizon.

risk

Given the relatively early stage of today’s technology, RGTI remains a high-risk investment opportunity, in my opinion. For example, as management commented in Q1, in addition to the industry still being in the development stage as of today, additional education about the current and potential state of the technology for potential customers remains important for managing expectations:

Overall, if you look at the number of clients, we have active discussions going on right now, and it’s in the range of 10 to 15 clients. We also make sure they have funding, are serious and understand the importance of their quantum computing. Clearly, we have not reached a point where quantum computers can demonstrate superiority over today’s classical computers. Therefore, these are primarily for research purposes. Therefore, we make sure that the client understands exactly what they are getting, and that they will get value from it before we follow up on every lead we get.

Source: Q1 earnings call.

As such, it is important to note that RGTI’s potential TAM will be very limited in the near term. Furthermore, since RGTI may continue to see relatively high R&D spending as a percentage of revenue, investors interested in the stock should also expect further stock dilution in the future. In my opinion, RGTI will continue to rely on cash flow financing rather than OCF generation in the near to medium term.

Evaluation/Pricing

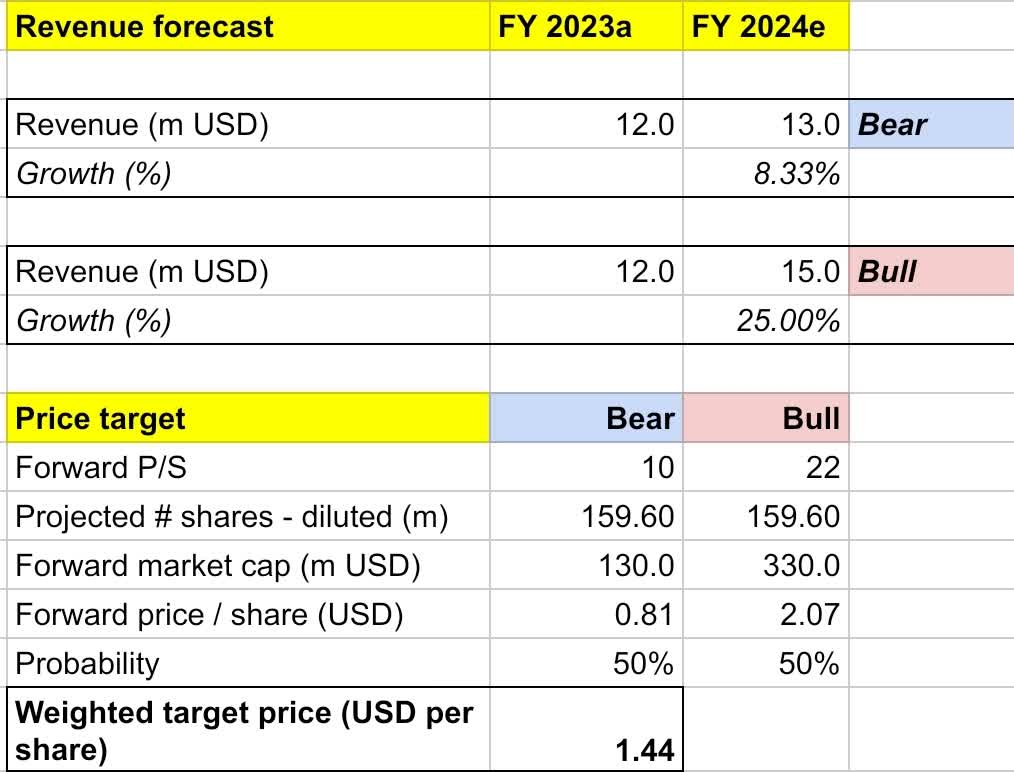

RGTI’s target price is driven by the following assumptions for bull versus bear scenarios for the FY2024 outlook:

-

Upside Scenario Assumptions (50% probability) – I expect revenues to grow 25% year over year to $15 million, in line with market estimates. I assume that the forward P/E will expand to 22 times, which means the stock price will rise to the $2 price level, and return to its highest levels since the beginning of the year. I assume that RGTI’s P/S will reach its highest level since the beginning of the year once it can achieve 25% year-over-year revenue growth, which is a significant rebound from 2023.

-

Downside Scenario Assumptions (50% probability) – RGTI will achieve FY2024 revenues of $13 million, 8.3% year-over-year growth, which is $1 million below the agreed-upon downside target. This will lead to a potential correction to $0.8 per share.

Private analysis

By incorporating all of the above information into my model, I arrive at a FY2024 weighted target price of $1.44 per share, an expected one-year upside of approximately 35%. I would rate the stock as a buy

Putting the downside probability at 50-50 is based on my belief that despite the promising development so far, the revenue growth outlook remains minimal to moderate. However, I think RGTI appears undervalued. After seeing a slowdown in 2023, the company appears to be on track for higher revenue growth and improved net income performance in 2024. Although the company still burned about $13 million of OCF in the first quarter, $102 million $ of liquidity should provide more than enough cushion to continue execution at the current level through the fiscal year.

Conclusion

RGTI is a company developing quantum supercomputing services. It should continue to benefit from the recently launched partnership program, which attempts to bring together all the leading names in quantum computing across the technology stack under one ecosystem. This should not only benefit RGTI by opening up more QPU sales opportunities, but also by developing technology to speed up the commercialization process. The risks are still very high, given the new and evolving nature of this industry. However, the risk reward can be attractive in my view. The price target is $1.4 per share for a ~35% yield. I rate the stock a buy.