com.bjdlzx

Ring Energy Company (New York Stock Exchange:Re) Management has been trying for a long time to push this company to a suitable operating model with adequate cash flow and an acceptable market debt ratio, as I discussed in the last article (and more before that). This type The shift can affect investor patience. However, the result should be a higher share price valuation based on lower debt concerns as well as the ability to return capital to shareholders which the market now demands.

This time around, management has reported significant financial and operational improvements through several acquisitions made in the past few years. The hope of the takeover drive was to accelerate the shift to stock market and debt market requirements. It seems that this hope has begun to come true.

There has been progress

Management has managed to keep some percentages from returning to the “high” levels they were at before the commodity Rising prices in fiscal year 2022 allowed many companies to achieve significant financial progress.

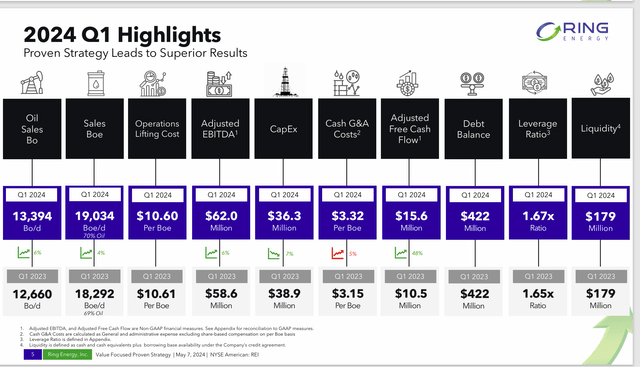

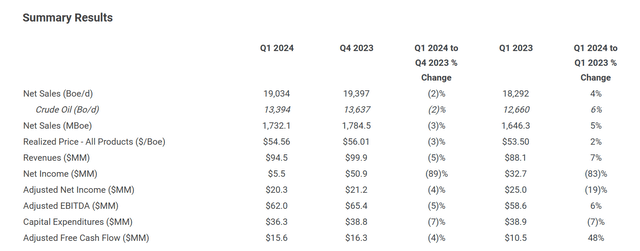

Summary of Ring Energy’s progress compared to the first quarter of the previous fiscal year (Ring Energy Q1 2024 earnings conference call slides)

Perhaps the main improvement highlighted above is the large percentage increase in free cash flow, even though oil prices haven’t changed much. Mr. Market generally uses free cash flow as a measure for oil and gas companies to pay down debt. This harks back to the earlier days when the unconventional group of companies couldn’t grow unless they borrowed money because upfront costs were (relatively) high compared to profits.

This is a traditional opportunity that does not have enough production yet. However, it is clear that management is “getting there” through an acquisition strategy. The debt balance was about the same as a year ago, despite acquisitions and increased production.

Much more importantly, the debt ratio has remained roughly the same despite the sharp decline in natural gas prices. Management’s first goal is to get the debt ratio below 1.5 (and later below 1.0). Companies that advertise better debt ratios can receive an upgrade in credit rating which often helps increase the value of outstanding shares.

The lack of movement in the debt ratio may indicate that this company may be able to show significant progress if commodity prices remain at the same level.

For shareholders

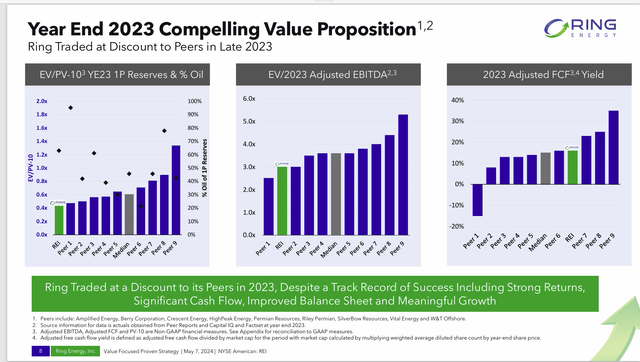

The slide shown below gives an idea of the improvement in the available stock price if the management brings some key ratios to acceptable levels.

Comparing Ring Energy’s value to other publicly traded entities (Ring Energy Q1 2024 earnings conference call slides)

As shown above, a company’s stock can easily double or more once the debt ratio gets below 1.0.

traditional opportunity

One difference between Ring Energy and many competitors is that Ring Energy represents a traditional opportunity. Therefore, the company’s wells show a lower initial decline rate than is the case with unconventional opportunities. A company, often times, has a strong opportunity to make more money on production in the first few years from the greater cash flow provided by a lower decline rate.

Comparing Ring Energy’s value to other publicly traded entities (Ring Energy Q1 2024 earnings conference call slides)

Of all the competitors mentioned on the slide, Riley Exploration Permian, Inc. (REPX) is the only one that has a traditional opportunity and is actually competing in the same type of business. The other companies are all unconventional with very high decline rates in the first year.

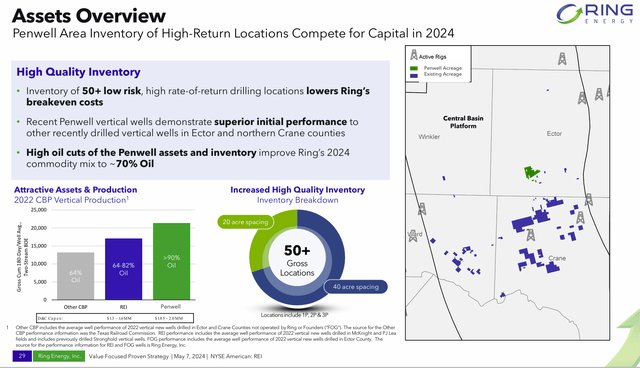

Leverage founder acquisitions

The founders were acquired using debt (not stock). Therefore, some wondered how such an acquisition could help the debt ratio.

Founders Acquisition of Penwell Area Lease Interests (Ring Energy Q1 2024 Earnings Conference Slides)

This space has actually raised the production mix to a greater proportion of oil than production. Over time, the process can be repeated similarly.

More oil as part of the production mix allows a company to make progress on debt without having to increase production. If, for some reason, it is not possible to purchase more assets because they are accretive or if oil prices decline, this area will likely continue to make money for the company and allow progress at a time when a large portion of the industry is likely to be in financial distress. compressed.

Earnings results

Cash flow is perhaps the best measure of how a company’s strategy is working.

Ring Energy Q1 2024 Earnings Press Release (Ring Energy Q1 2024 Earnings Press Release)

Note that the realized price and free cash flow are little changed. This shows that for the most part, weaker commodity prices between 2023 and 2024 had little impact on the company’s free cash flow. This is important because the last thing the administration needs is for the debt ratio to rise again due to falling commodity prices.

The next step, of course, would be to make some additional acquisitions to reduce the debt ratio before commodity prices rise to make acquisitions too expensive.

Adjusted net income is essentially the net income shown above without the effects of unrealized commodity losses. Clearly, the more profitable mix of founder takeover had an impact on the company’s comparison without founder production.

summary

This stock will require some patience (if it doesn’t already). Progress toward the goal of reducing the debt ratio has been slow, but significant. The goal of finding accretive acquisitions appears to be a challenge for management.

Once the debt ratio gets where it needs to be, this stock could be revalued significantly. Whether or not it is worth waiting is up to the individual investor. Hopefully management will make at least one acquisition this year.

As part of a basket of well-selected oil and gas stocks, this aggressive speculative buying should enable that basket to outperform over the long term. If this is your only property, you may have to keep a close eye on it.

The wells still look just as profitable as they did when I started following the company. The main problem is that when transitioning from an exploration stage company to a going concern, the coronavirus pandemic has had all its challenges. What was a conservative position has turned into today’s set of challenges. Management is doing well with the “hand it has been dealt” because debt market requirements and stock market conditions changed “overnight.” Many small businesses get into a financial bind like this through no fault of their own.

Risks

This company needs some cooperation from commodity prices to get its debt ratio down. Commodity prices have low visibility and are highly volatile. However, market demands of “living within your means” and shareholder returns have limited the industry’s growth. This can ensure that commodity prices remain in a range that is beneficial to the company in this case.

Growth through acquisition can be derailed if an acquisition is not executed as desired.

Losing key employees can be devastating to a company in a situation like this.