Evening pictures

thesis

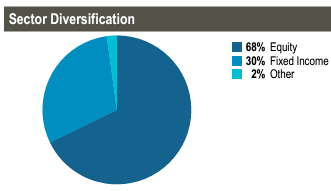

Cohen & Steers Real Estate Opportunities and Income Fund (New York Stock Exchange: RLTY) is a closed-end equity fund. CEF focuses on REIT stocks, but also has a 30% fixed income consisting of preferred stock. box It comes with a high leverage ratio of up to 35% and has a high beta versus its non-leveraged counterparts in the ETF world.

We’ve covered this name before, right when it went public, and correctly predicted its discount would widen on the back of weak performance of the underlying assets. RLTY had very poor timing in terms of getting to market, and has struggled ever since, despite its strong structure.

In this article, we’ll revisit the name and highlight why it represents an attractive high beta fund to use for REIT space.

Fund holdings – 70% of share capital

CEF has a 70/30 split between its equities and fixed income funds:

Taksim Holding (statement of facts)

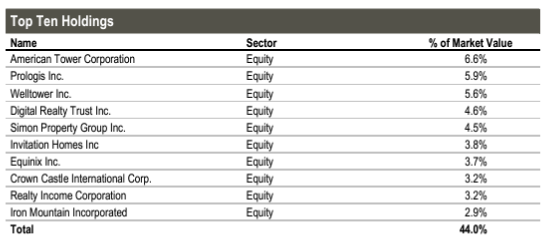

Its most significant holdings consist of well-known REITs, with a clear concentration in the top five names:

Top Holding (statement of facts)

The top five names make up more than 27% of the fund, while the top 10 holdings represent 44% of the collateral. This central fund position is fairly concentrated, and is an active participant in the fund manager’s preferred list of names.

The fixed income wrapper contains a portfolio of preferred financial stocks, details of which can be found by downloading the holdings list here. Most preferred stock holdings come from large, systemically important companies, but credit spread risk still exists, with many securities being perpetual.

While the fixed income wrapper does not have a high probability of default risk, it does have a large duration and sensitivity to the credit spread. Expect fixed income to lose value when rates rise or when credit spreads widen.

Use leverage as an asset, but beware of volatility

Leverage has two elements to pay attention to when using it in CEF. First, leverage leads to volatility, both up and down. Therefore, leveraged ETFs tend to outperform sector ETFs in bull markets, while underperforming in down scenarios.

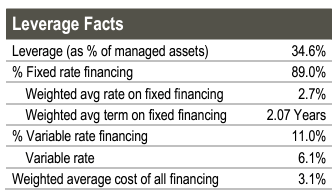

Second, low leverage can lead to NAV accumulation, especially for fixed income funds. RLTY has cleverly structured its influence:

Leverage details (statement of facts)

Approximately 90% of the fund’s leverage is in a fixed-rate format, meaning the fund’s cost of leverage has not increased much as rates rise. The average fixed interest rate is just 2.7%, a level that many funds would consider an asset. Financing with a variable interest rate is in line with the market, and is done through repurchase facilities at a rate of approximately 50 basis points.

Leverage amplifies a fund’s performance, but when done right it can also be considered an asset. The CEF we own and cover on Seeking Alpha is the Flaherty & Crumrine Preferred and Income Securities Fund (FFC), which we recently reviewed here. FFC’s leverage is a variable rate of 100%, making the fund lagging in the current high interest rate environment. On the other hand, RLTY pays only half of what FFC pays on interest expense.

The CEF outlines the same financial engineering dynamics in its annual report:

The use of leverage is a speculative tactic and there are special risks and costs associated with leverage. The net asset value of the Fund’s shares may be reduced by issuance and ongoing costs of leverage. As long as the Fund is able to invest in securities that produce a greater than total investment return Cost of Leverage A leveraged strategy will produce a higher net current investment income for shareholders. On the other hand, to the extent that the total cost of leverage exceeds the additional income earned from using that leverage, shareholders will realize less net investment income. In addition to the impact on net income, the use of leverage will have an impactExaggerate capital appreciation or decrease shareholder value. Specifically, in a bull market, leverage will typically result in greater capital appreciation than if the Fund had not used leverage.

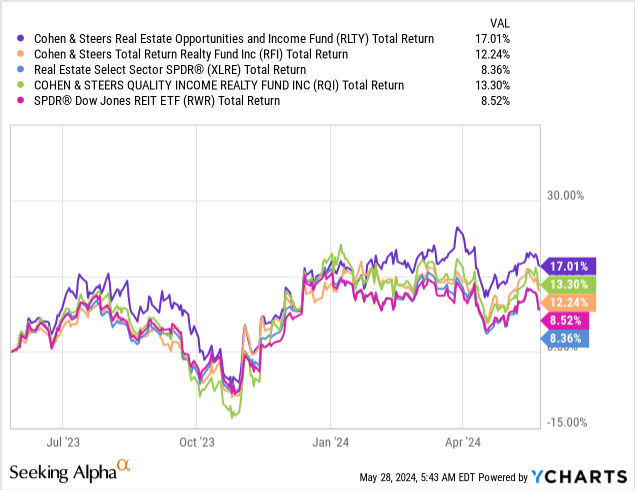

Performance – Outperforming the competition

Given its poor timing regarding the IPO, let’s take a look at RLTY in light of its performance last year:

In the chart above, we compare the fund to leveraged vehicles (other mutual funds) and non-leveraged funds in the form of ETFs. To this end, the selected group is:

- Mutual Funds: Cohen & Steers TR Realty Fund (RFI), Cohen & Steers Quality Income Fund (RQI)

- ETFs: Real Estate Select Sector SPDR (XLRE) and SPDR Dow Jones REIT ETF (RWR)

RLTY outperformed the entire group last year, posting a total return of more than 17%, versus 13.3% for the closest competitor. Unsurprisingly, non-leveraged funds (ETFs) have lower total return numbers, while ETFs outperform. RFI’s performance is also notable given that the fund has minimal leverage, but is actively managed.

The negative thing to note is that RLTY has the highest beta of the entire group (1.1 beta according to Tradingview.com). While analytics also highlight this factor, an investor can clearly see the beta multiple from the chart above, where the CEF’s total return line is very volatile, both on the downside and the upside.

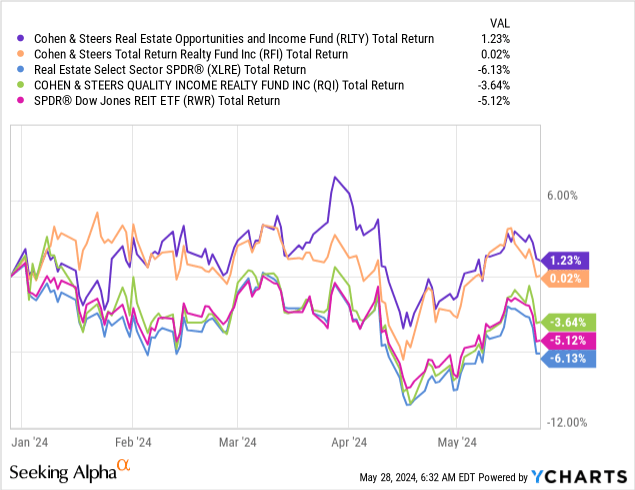

The fund’s portfolio composition has helped it get through 2024 better than most of its competitors:

RLTY and RFI are the only funds that rise during the year on a total return basis.

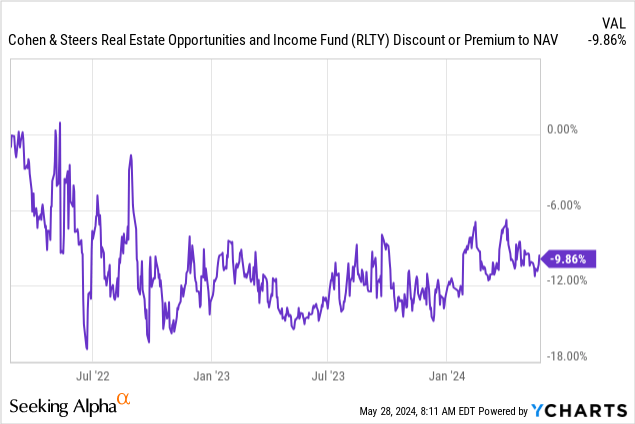

Discount to NAV – stability on the back of strong performance

RLTY went public at a really tough time in the market when the Fed started raising interest rates. Due to the downward movement in the Fund’s core holdings, the IMF experienced a turbulent start to its existence:

We can see from the chart above that CEF moved to a significant discount to NAV in 2022, a discount that briefly reached -18%, which prompted our article “RLTY: The discount has gotten too big”. The fund now sits at a roughly -10% discount, with a cyclical bull market bringing the name closer to stable NAV in our view.

CEF discounts to NAV are always a factor in historical performance and the intelligence of the collateral manager. The greater the positive performance of the CEF, the lower the discount. RLTY is off to a false start due to macro factors, and we fully expect the name to trade flat to NAV once the interest rate environment moves lower and REITs find themselves in a cyclical bull. So expect an additional +10% increase to the fund’s total return once the above factors are met.

The main risk factor – hard landing

The main risk factor for this high beta fund is a “hard landing.” If CEF’s underlying stocks start selling off on the back of weak economic data, the fund will have a high downside move due to its high beta and leverage. RLTY is properly set up for a range-bound market or cyclical bull, but will post large drawdowns in the event of a hard bearish.

2022 was a tough year for holders to recognize the beta factor, as CEF saw a -37% decline, half of which was driven by a widening of its discount to NAV.

Investors need to assume a soft landing or a fairly weak economy in order to buy a fund like RLTY. Choose a non-leveraged ETF that has… REITs otherwise.

Conclusion

RLTY is REIT Stock CEF. The fund has 70% equity and 30% fixed income consisting of preferred stocks. The CEF comes with a very high leverage ratio of 35%, and represents a high beta in the REIT market. In range-bound or rising markets, the fund will outperform, as observed last year. Conversely, in down markets, investors will experience larger drawdowns than they experienced in vanilla REIT ETFs.

RLTY has a very good liability structure, with most of its fund costs being implemented through fixed-rate instruments. The low cost of funds translates into high net income during capped or higher markets due to its fixed income. We love this manager REIT and CEF’s active approach, we feel the fund is an appropriate vehicle to use for investors looking for high beta names in… REIT space.