hapabapa

In the volatile stock market of 2024, winners made big gains while losers moved deeper and deeper into the penalty box. However, more often than not, the stock price performance has been completely uncorrelated with the underlying fundamental performance, which I believe is the case with… rocco (Nasdaq: Roku).

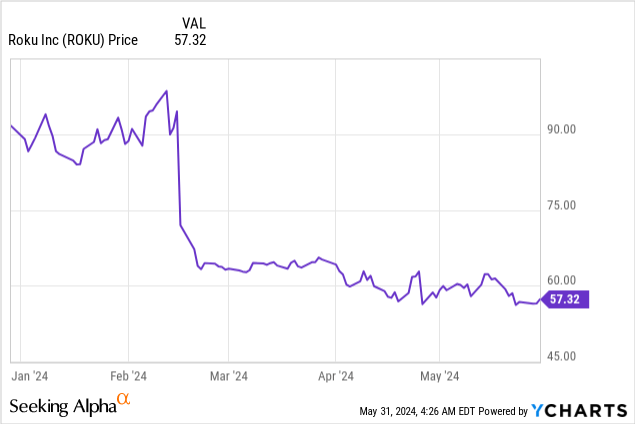

Roku, the leading streaming company for both devices and platforms, is now down nearly 40% year-to-date. The company’s first-quarter earnings announcement, revealed in April, did little to calm investors despite the crisis Acceleration In revenue growth and sharp gains in profitability. It’s a great time, in my view, for investors to reevaluate the bull case for Roku.

after With prices falling, the bull case for Roku has never looked more favorable

I last wrote a bullish article on Roku in March, when the stock was still trading The mid-sixties and before the company’s first quarter earnings announcement. With stock prices having fallen since then, as well as positive updates from the first quarter (which we’ll discuss in the next section), I’m still… rising on Roku for the rest of the year.

There are a few product updates worth mentioning: First, the company noted the successful sales of its new Roku Pro TV product. This is Roku’s high-end smart TV that starts at $699 (for the 55-inch model; there are additional options for 65-inch and 75-inch screen sizes), and includes AI-powered brightness and color adjustment features and a new side-speaker system. We remind investors that although the devices are not profitable Rocco (Indeed, strong hardware sales here are the driver behind the company’s year-over-year gross margin decline), but they are the gateway to streaming and platform revenues.

Speaking of which: The company notes that its streaming service distribution activities are accelerating. During the Super Bowl, the company generated revenue from directing viewers toward Paramount+. Roku also handles payment processing for sign-ups through the Roku platform, creating a captive growth market for its Roku Pay segment. The company is also continuing to innovate in the viewing experience to try to increase engagement and more subscriptions, with sports in particular. The company’s new NBA region, which complements the existing NFL region, creates a one-stop-shop for sports fans to access their content through the Roku platform.

Here’s a refresher on my complete long-term bull case for Roku:

-

Roku’s shift toward a platform-first model has dramatically improved its margins and stabilized its revenue. At one point, Roku’s revenue split between lower-margin hardware players and its platform revenue was closer to 50/50; Now, hardware represents less than 20% of Roku’s total revenue. Not only has this improved profitability, but it also means that Roku’s revenue is more stable quarter-to-quarter and not as highly dependent on the seasonality of hardware sales.

- Secular tailwinds toward streaming and away from traditional television The company notes that in the US in the first quarter, streaming hours increased 23% year-over-year in the US while traditional TV viewing time fell 13% year-over-year in the same time period.

-

The company continues to drive growth across The Roku Channel and is also a leader in original programming. The company’s platform is now one of the leading streaming offerings in the United States. This channel is now also producing original content, including a new documentary in partnership with the NFL that has become one of the most popular shows on Roku. Sports-oriented hubs, such as the company’s NFL and NBA territories, continue to drive engagement and subscriptions to other companies’ streaming services.

-

Streaming Distribution and Roku Pay- The company has also increased the pace of facilitating subscriptions to streaming services from its platform, where it also generates revenue through processing via Roku Pay.

-

International expansion opportunity- Rocco It has recently set its sights on aggressively expanding overseas, with recent initiatives in the UK, Canada and Mexico – representing the next phase of growth for the company. Although this has resulted in a lower average revenue per user (ARPU) for the company (international markets generate less advertising money than the US), we should focus on getting attention first and worry about revenue contribution later.

- Rich cash balances- The company has more than $2 billion of net cash on its books and no debt, which represents about a quarter of its current market capitalization of $8 billion.

Stick around for the long haul and buy Roku while it’s down.

Download Q1

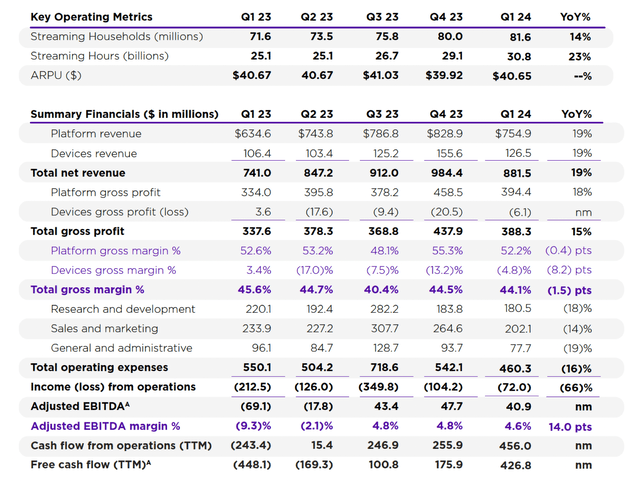

Let’s now review Roku’s latest quarterly results in more detail. Q1 earnings highlights are shown in the snapshot below:

Roku Q1 results (Roku Q1 Shareholder Letter)

Roku’s revenue rose 19% year over year to $881.5 million, with 19% growth in both its platform (software and advertising) and hardware sales. It beat Wall Street’s more modest forecast of $850.4 million (+15% y/y) by a margin of four points, while also accelerating against the Q4 growth rate of 14% y/y — making the stock’s post-earnings decline even more puzzling.

This is the beginning of the year in which Roku expects overall growth to accelerate. CEO Anthony Wood’s remarks on the first quarter earnings call:

We will accelerate platform revenue, adjusted EBITDA, and free cash flow growth in 2025 by focusing on three key opportunities, maximizing Roku Home Screen as the TV leader, growing Roku bill subscriptions, and driving ad demand. For Roku.

Every day, Roku Home Screen reaches US households of about 120 million people. This greater reach creates a lot of opportunities. I see many ways to improve the user experience while increasing monetization for Roku (…)

We also see a huge opportunity to grow the subscriptions that Roku bills with. Roku Pay, our payment and billing service, simplifies the sign-up process for users so they can get up and running quickly and ensures content partners don’t lose subscribers due to unnecessary friction at the point of purchase. Additionally, we are making it easier for advertisers to execute campaigns programmatically on the Roku platform by expanding and deepening our relationships with third-party platforms.”

We note that Roku’s guidance for Q2 indicates a 10% deceleration in revenue growth year over year, along with hardware gross margin expected to be in the negative teens. While Roku is certainly barred from having a perfect story, investors should keep in mind that Roku’s strategy is to produce competitively priced devices and generate long-term revenue through advertising and subscriptions.

The presence of leading hardware products did not at all prevent Roku from improving its profitability, as adjusted EBITDA in the first quarter rose to a profit of $40.9 million with a margin of 4.6%, representing a profit of $40.9 million. An improvement of 14 points year-on-year Compared to -9.3% adjusted EBITDA margin in the first quarter of last year.

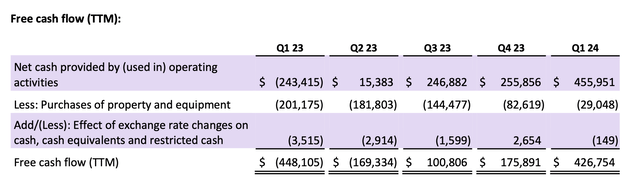

We also note that Roku generated a whopping $427 million in trailing-twelve-month FCF, versus FCF Burn A similar size in the same period last year.

Roku TTM FCF (Roku Q1 Shareholder Letter)

Evaluation and key takeaways

At current stock prices near $57, Roku is trading with a market cap of $8.26 billion. After we liquidated $2.06 billion in cash in the company’s most recent balance sheet, the Enterprise value: $6.20 billion – Which represents just 14.5x TTM FCF multi. Taking into account the multiple levers for continued double-digit growth (and the fact that over the long term, higher margin platform revenue will continue to represent a higher mix of revenue versus hardware, which will boost adjusted EBITDA) And (FCF margins), I would say Roku stock is on sale now.

Don’t miss the opportunity to build a position in Roku while it’s still cheap.