pcess609

This monthly article series presents sector metrics in the S&P 500. It is also a top-down analysis of ETFs based on the S&P 500, such as the Invesco S&P 500 Equal Weight ETF (NYSEARCA:RSP).

RSP strategy and historical performance

Invesco Standard & Poor’s The Equal-Weighted 500 Foundation holds all S&P 500 stocks in an equal-weighted portfolio, which is rebalanced quarterly. The RSP is expected to outperform the S&P 500 over the long term by betting on Size factor (smaller companies have a higher weighting than the capitalization-weighted index) and the rebalancing mechanism (a systematic “buy high, buy low” strategy). In fact, the equal-weighted S&P 500 has outperformed the capitalization-weighted index by 1.9% in annual return since 1/1/2000, but by only 23 basis points since the inception of the RSP system (04/24/2003). The RSP has lagged in the past three years, especially in 2024. Its expense ratio is slightly higher than the SPDR S&P 500 ETF Trust (spy): 0.20% vs. 0.09%.

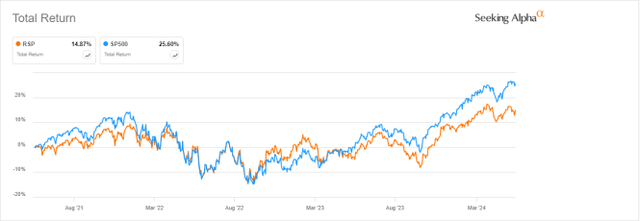

RSP vs. SPY, 3-year return (Searching for Alpha)

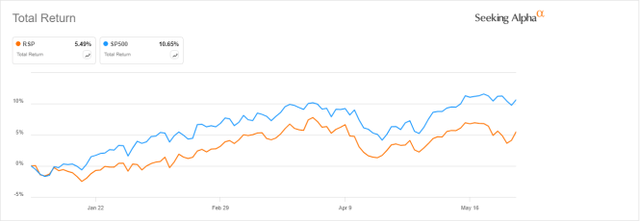

RSP vs SPY, 2024-present (Searching for Alpha)

RSP has a bias to value: it is cheaper than SPY based on valuation ratios and has a lower overall earnings growth rate, as shown in the following table.

|

RSP |

spy |

||

|

P/E TTM |

20.02 |

24.39 |

|

|

Price/book |

2.68 |

4.26 |

|

|

Price/Sales |

1.67 |

2.79 |

|

|

Price/cash flow |

12.13 |

16.79 |

|

|

Earnings growth |

16.18% |

21.92% |

|

source: devotion

Now, let’s get into the details of the sector metrics within RSP (which are also relevant to other S&P 500 ETFs).

abbreviation

The next two paragraphs in italics describe the dashboard methodology. They are essential for new readers to understand metrics. If you are familiar with this series or if you are short on time, you can skip it and move on to the charts.

Basic metrics

I calculate the average value of five key ratios in each sector: earnings yield (“EY”), sales yield (“SY”), free cash flow yield (“FY”), return on equity (“ROE”), gross margin (“G m”). They are all calculated over a 12-month period. For all of these ratios, higher is better and lower is bad. EY, SY, and FY are averages of the inverses of price/earnings, price/sales, and price/free cash flow. They are better for statistical studies than P/E ratios, which are unusable when “something” is close to zero or negative (for example, companies with negative earnings). I also calculate two momentum measures for each group: average monthly return (RetM) and average annual return (RetY).

I prefer averages rather than averages because the median divides the group into a good half and a bad half. Capital-weighted averages are skewed by outliers and large firms. As a result, these metrics are designed for stock picking rather than index investing.

Value and quality points

Historical baselines are calculated as averages over an 11-year lookback period for all metrics. They are respectively denoted EYh, SYh, FYh, ROEh, GMh. For example, the EYh value for technology in the table below is the 11-year average of the average dividend yield for technology companies included in the S&P 500 Index.

The “VS” value score is the average percentage difference between the three evaluation ratios (EY, SY, FY) and their baselines (EYh, SYh, FYh). In the same way, the QS score is the average difference between two quality ratios (ROE, GM) and their baselines (ROEh, GMh).

VS can be interpreted as the percentage of undervaluation or overvaluation compared to the baseline (positive is good, negative is bad). This interpretation must be taken with caution: the baseline is an arbitrary reference, not an assumed fair value. The formula assumes that the three valuation metrics are equally important, with the exception of energy and utilities, where free cash flow yield is ignored to avoid some inconsistencies. VS and QS The maximum is between -100 and +100 When the account is gone behind ythis values.

Current data

The following table shows metrics and results as of the last daily close. The columns represent all the data specified above.

|

against |

QS |

any |

bad |

fiscal year |

Return on shareholders’ equity |

GM |

Yes |

Seeh |

FYh |

Return on shareholders’ equity |

G.M.H |

Rhett M |

Riti |

|

|

everyone |

-11.41 |

6.02 |

0.0388 |

0.3563 |

0.0243 |

16.36 |

48.38 |

0.0428 |

0.4122 |

0.0274 |

15.19 |

46.39 |

2.71% |

18.97% |

|

Customer services. Available |

1.50 |

22.78 |

0.0465 |

0.5258 |

0.0355 |

30.29 |

38.42 |

0.0448 |

0.6384 |

0.0300 |

21.68 |

36.31 |

1.55% |

16.66% |

|

Customer services. paper clip |

2.00 |

-6.30 |

0.0451 |

0.5123 |

0.0187 |

20.33 |

40.84 |

0.0418 |

0.4698 |

0.0210 |

23.45 |

40.55 |

-0.81% |

-3.17% |

|

energy |

100 |

92.65 |

0.0682 |

0.4746 |

0.0363 |

20.67 |

45.87 |

0.0244 |

0.5469 |

-0.0041 |

7.40 |

43.30 |

2.02% |

26.20% |

|

Finance |

4.97 |

6.71 |

0.0637 |

0.5329 |

0.0658 |

11.78 |

80.77 |

0.0685 |

0.4323 |

0.0667 |

11.17 |

74.81 |

1.98% |

37.64% |

|

health care |

-14.03 |

-8.06 |

0.0266 |

0.2770 |

0.0255 |

13.24 |

63.56 |

0.0341 |

0.2731 |

0.0325 |

15.81 |

63.48 |

0.59% |

7.36% |

|

Industries |

-28.53 |

3.24 |

0.0342 |

0.2910 |

0.0210 |

21.30 |

39.78 |

0.0433 |

0.5098 |

0.0268 |

21.35 |

37.27 |

2.37% |

23.66% |

|

technology |

-30.11 |

12.16 |

0.0268 |

0.1584 |

0.0247 |

28.08 |

62.18 |

0.0367 |

0.2526 |

0.0334 |

22.31 |

63.13 |

4.15% |

21.31% |

|

communication |

19.25 |

3.34 |

0.0439 |

0.7115 |

0.0450 |

17.20 |

55.99 |

0.0459 |

0.5285 |

0.0353 |

16.51 |

54.62 |

4.88% |

6.72% |

|

Material |

-14.44 |

-3.10 |

0.0301 |

0.5832 |

0.0213 |

16.02 |

37.07 |

0.0435 |

0.5951 |

0.0238 |

17.50 |

36.24 |

3.34% |

29.44% |

|

Services |

-4.79 |

9.54 |

0.0525 |

0.4123 |

-0.0845 |

10.40 |

44.24 |

0.0493 |

0.4912 |

-0.0567 |

9.61 |

39.90 |

4.84% |

12.26% |

|

Real estate |

18.56 |

10.14 |

0.0303 |

0.1246 |

0.0087 |

8.29 |

64.74 |

0.0234 |

0.1147 |

0.0074 |

6.82 |

65.64 |

4.02% |

9.75% |

Result charts

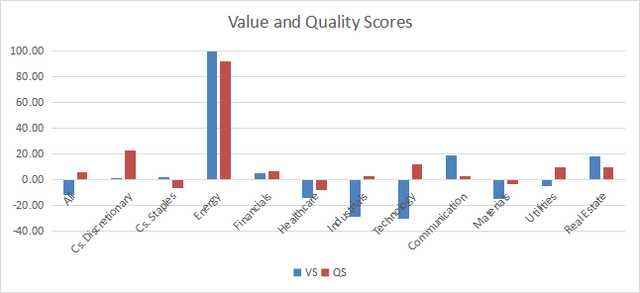

The following chart shows value and quality scores by sector (higher is better).

Value and quality in the S&P 500 (Chart: Author; Data: Portfolio123)

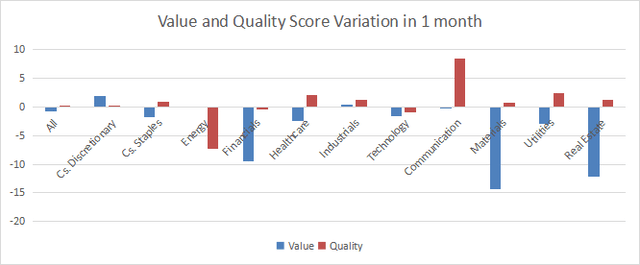

Score variation since last month:

Differences in value and quality (Chart: Author; Data: Portfolio123)

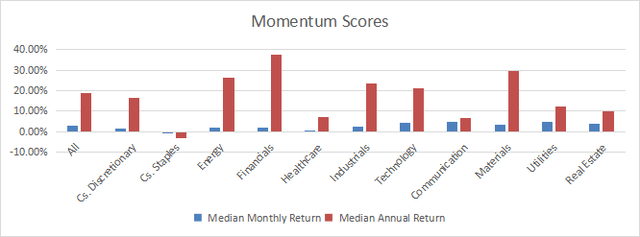

The following chart plots momentum scores based on average returns by sector.

Momentum in the S&P 500 (Chart: Author; Data: Portfolio123)

Explanation

The hypothetical “average” S&P 500 company is 11.4% overvalued compared to the average valuation metrics since 2013. The Quality Score is slightly higher than the historical baseline. We can translate the average returns by their inverse ratios:

Price/earnings: 25.77 – Price/Sales: 2.81 Price/Free Cash Flow: 41.15

Energy has shown the highest value and quality scores among GEX sectors since February 2022. Real Estate and Telecommunications are also undervalued by approximately 19% compared to 11-year averages. Financials, consumer estimates, consumer staples and utilities are close to the historical baseline in valuation. Materials and health care are overvalued by about 14% compared to the baseline, while technology and industrials are overvalued by about 30%.

The SPY has gained 25% in 12 months (total return), while the average return for the S&P 500 is 19% (reported in the table above) and the equal-weighted return (measured on the RSP) is 17.3%. This means that the capitalization-weighted index has been skewed to the upside by large-cap companies over the past 12 months.

Cheap stocks among peers

We use the table above to calculate our Value and Quality Score. It can also be used in the stock picking process to check where companies stand among their peers. For example, an EY column tells that a large consumer staples company with an earnings yield above 0.0451 (or a P/E below 22.17) is in the better half of the sector with respect to this metric. The dashboard list is sent every month to Participants with the most profitable businesses stand in the better half among their peers on all three valuation metrics at the same time. The nine stocks mentioned below are an excerpt from the list of 75 companies sent to subscribers for the June 2024 update.

|

CHTR |

Charter Communications Company |

communication |

|

Global Positioning System |

GAP Company |

Available |

|

Abba |

ABA company |

energy |

|

SYF |

Financial synchronization |

Financial |

|

Ministry of Health |

Molina Healthcare Company |

health care |

|

D |

Deere & Co |

industrial |

|

BJ |

Pong International SA |

paper clip |

|

GDDY |

Godaddy, Inc. |

Technique |

|

EXC |

Exelon Company |

Uses |

It is a rotational model with a statistical bias toward long-term excess returns, not the result of analyzing each stock.