COLIN ANDERSON PRODUCTIONS PTY LIMITED

We’ve previously covered RTX (New York Stock Exchange: RTX) in March 2024, to discuss its excellent FY2023 results and growing backlog, which was attributed to the unstable geopolitical landscape and the recovery of passenger flights.

It was clear that the negative Press related to the quality of crushed metal manufacturing problem It has been far behind us, with the stock also recovering much of its earlier losses thanks to massive upside support.

Since our Buy rating, RTX is already up +17.9% well outperforming the broader market by +3.3%.

However, the stock continues to present a potentially strong dividend investment thesis, thanks to promising market trends and recently raised payouts, respectively.

Combined with its growing business backlog, excellent Q1 2024 earnings results, and reasonably priced stock valuations compared to its aerospace engine peers, we reiterate our buy Rating here.

RTX’s investment thesis remains strong, with growth in commercial/defense spending driving growth catalysts

Currently, RTX reports double-digit earnings for Q1 2024, with total revenue of $19.3 billion (-3.1% QoQ/+12.1% YoY) and adjusted EPS of $1.34 (+3.8% QoQ). QoQ/+9.8% YoY).

Much of the tailwind was naturally attributable to strong commercial sales of $8.72 billion (-5.2% QoQ/+17.9% YoY) and sales to the US government of $8.12 billion (-3.6% QoQ/+7.5 % on an annual basis) among others.

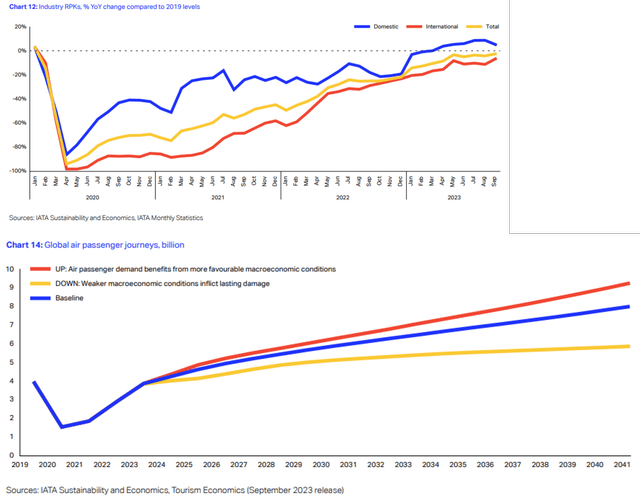

Global air travel trends and forecasts

International Air Transport Association

Meanwhile, RTX continues to report an increase in backlog of $202 billion (+3% QoQ/+12.2% YoY) by Q1 2024, including commercial aviation contracts worth $125 billion ( +5.9% QoQ/+14.6% YoY) and defense contracts worth $77 billion (-1.2% QoQ/+8.4% YoY).

Strong growth in business backlog is not a surprising development indeed, with global air travel recovering close to pre-pandemic averages by the end of 2023.

Things are expected to grow even further over the next few years as “the global commercial aviation fleet also expands by +33% to reach more than 36,000 aircraft by 2033, according to analysis by Oliver Wyman.”

Readers should also note that defense spending is expected to remain high in the future, as the US government recently signed an $886 billion policy bill into law, to support future RTX investments in R&D and manufacturing capabilities.

As a result of the excellent visibility in its top lines, we believe it remains well positioned to maintain future growth prospects.

Much of RTX’s positive results are also attributable to management’s numerous cost-cutting initiatives, as discussed in our previous article, allowing the company to report a sustained expansion in operating margins to 11.4% in fiscal Q1 2024 (+0.7 y/y / +3.7 y/y). FY21 levels of 7.7%, partially offsetting rising inflationary pressures to date.

Importantly, metal powder processing is already underway, with management reporting peak aircraft on ground (AOG) by FQ1’24 and things will moderate through 2026, naturally reducing upcoming penalty charges.

Risks remain as RTX’s debt leverage grows – the potential impact on the bottom line in the future

On the other hand, readers may also want to keep an eye on the health of the balance sheet going forward, with RTX’s net debt-to-EBITDA ratio increasingly high at 3.2x by Q1 2024, compared to 2.8x in Q4 of 2023, 2.3x in Q4 2023. FQ1’23, and 2.33x in FQ4’21.

When compared to aerospace engine peers, such as Rolls-Royce Holdings (OTCPK:RYCEY) (OTCPK:RYCEF) at 0.76x, GE Aerospace (GE) at 0.24x, and aerospace and defense industry averages of 1.69x, it’s undeniable that leverage RTX debt is somewhat risky.

This is particularly because $300 million of its long-term debt will be due in 2024, $3.5 billion in 2025, and $4.46 billion in 2026, which could lead to more refinancing during a higher interest rate environment. and, therefore, higher annual interest expenses than reported. In the first fiscal quarter of 2024 at $1.62 billion (+8% QoQ/+28.5% YoY).

This could impact its bottom line growth while raising headwinds to its profitable growth prospects. As a result, this may be a major risk that interested readers may want to consider.

So, is RTX stock a buy?Sell, or hold?

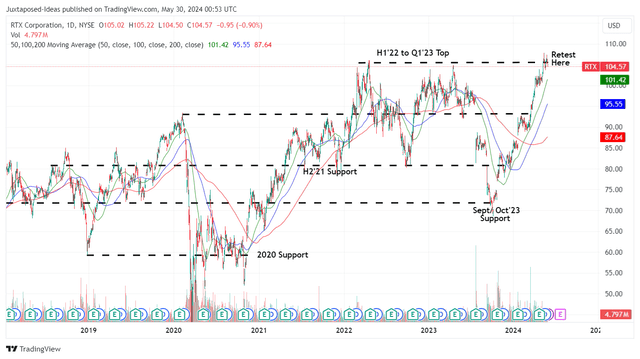

RTX 5Y stock price

Trading offer

Right now, RTX is actually bullishly higher after the latest earnings call, while staying away from its 50/100/200 day moving averages.

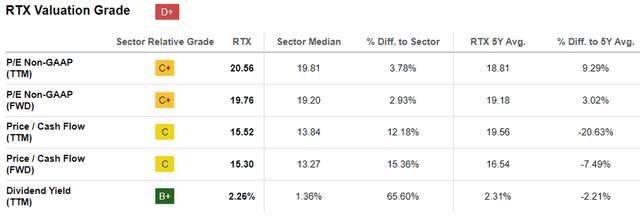

RTX Ratings

Seeking alpha

However, we think RTX is not expensive at its FWD P/E valuations of 19.76x. While this number is higher than the previous article at 16.81x (reduced due to the metal powder issue) and the pre-pandemic 3Y average of 17.33x, it is still relatively reasonable compared to its peers, such as RYCEY at 28.21x and GE at 28.21x. 39.80x.

This is especially due to RTX’s stable up/net forecast comparison of +9%/+10.1% CAGR through FY2026, compared to RYCEY at +8.3%/+13.6% and GE at -13.1%/+28.3%, on straight. , implying that the former’s relatively reasonable FWD valuations are 19.76x at current levels given its promising profitable growth outlook.

As a result of its reasonable valuations, we believe RTX continues to trade close to our fair value estimate of $102.10, based on LTM EPS of $5.17 (+2.1% from FY2023 levels of $5.06 and +6.3%, respectively) and recovery FWD P/E ratings are 19.76x.

Based on FY2026 consensus EPS estimates of $6.76 and the same FWD multiple valuations of 19.76x, there remains excellent upside potential of +25.6% for the long-term price target of $133.50 as well.

Readers should also note that RTX recently raised its quarterly dividend by +6.7% to $0.63, naturally maintaining its dividend investing thesis with a forward yield of 2.37%, compared to a 5-year dividend growth rate of +5.59% and an average The sector increased by 1.41%. , respectively.

This comes in addition to ongoing share repurchases where 136.9 million or 9.2% of outstanding shares were withdrawn during the LTV period, demonstrating management’s excellent use of strong free cash flow.

As a result of the continued two-pronged potential returns through capital appreciation and dividends, we maintain our Buy rating on RTX, although there is no specific entry point given it is currently retesting its all-time highs at $106.

Interested investors may consider monitoring the stock’s movement for a little longer, before adding the price according to dollar cost averaging and their risk appetite.

However, we think RTX is likely to continue to perform well, largely supported by long-term catalysts from rising multi-year accumulation and strong business/defense spending, well, while offsetting the risks from increased reliance on debt.