john m. Chase

Investment thesis

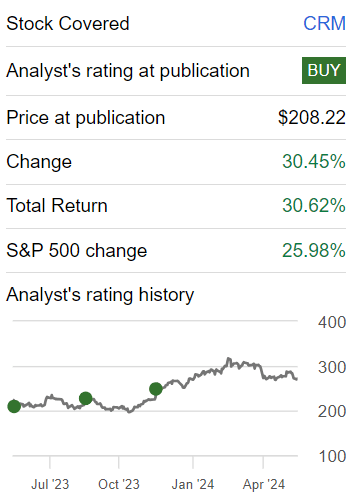

sales force (New York Stock Exchange: Customer Relationship Management) witnessed a decline in its shares on the back of the results of the first quarter of the fiscal year.

At the same time, I see this sale as unjustified. Yes, investors haven’t taken too hard on the fact that Salesforce’s growth rates are moderate. But this is it Old news. Although the fact is that Salesforce was not able to revise its revenue growth forecast for fiscal 2025 upward It clearly surprised investors.

But over time, investors will shake off this shock. They will once again reevaluate Salesforce based on its intrinsic value. On that front, having to pay forward 23 times non-GAAP EPS is a very fair entry point.

Therefore, I remain bullish on CRM.

Quick recap

I said in my previous analysis in November:

(…) What I think will set Salesforce apart from many of its peers is that this business generates insanely strong cash Flows and profits. Yes, clean operating profits after SBC and GAAP.

I stand by this statement.

The author worked on CRM

As you can see above, Salesforce is a stock I’ve been bullish on for some time. In fact, I felt like repeating the title of my article this time last year, “Don’t Throw in the Towel” in this article. After all, it’s the same message again.

Furthermore, including the 16% pre-market sell-off, following the advice from my job last year would have netted investors nice gains. In fact, I reiterate this assertion that investors should not give up on CRM.

Salesforce’s near-term prospects

Salesforce used its earnings call to highlight its use of strategic AI, as you’d expect. For example, Salesforce has asserted its leadership position in the CRM market, managing more than 250 petabytes of customer data, which is critical to its AI transformation.

Salesforce also announced that Data Cloud is emerging as the next billion-dollar product, with the need to seamlessly integrate customer data across platforms. Furthermore, Salesforce reminded investors of its partnerships with megatech companies, such as Amazon (AMZN), Google (GOOGL)(GOOG), and Microsoft (MSFT), which have strengthened its position in the AI landscape.

However, Salesforce faces near-term challenges, most notably a weak remaining performance obligation (“RPO”), a critical forward-looking indicator. First-quarter results fell short of expectations for CRPO growth, raising concerns about future revenue stability. Although full-year revenue guidance was maintained, this discrepancy indicates potential risks.

Case in point, customers exhibit deliberate purchasing behavior, leading to lengthy sales cycles, as well as shorter project lead times.

Given this background, let’s now delve into its financials.

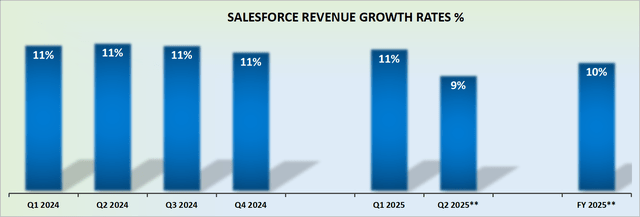

Saleforce guidelines indicate a 10% CAGR

CRM revenue growth rates

Salesforce appears to be growing a little slower than analysts expected, with its RPO rate falling sequentially, which investors have no doubt latched on to, as this is a key leading indicator.

Also, not only did Salesforce marginally miss its revenue estimates for the first quarter of fiscal 2025, but its forecast for fiscal 2025 also came in well below analyst expectations, at $38.00 billion at the high end versus $38.01 billion.

A little went wrong and investors completely lost confidence, with the stock down 16% after hours. Overreaction? Obviously so. Ultimately, the fact that Salesforce’s growth prospects have declined is not news to anyone.

Instead, I think what happened here is that the stock showed some weakness in the last few months, and investors wanted to be reassured that Salesforce still had more power left in the tank.

As a leader in its industry, investors can be very tolerant of many different aspects of a company’s performance and prospects, but what investors don’t want to see is their company’s revenue growth rates slowing. And that’s what happened here.

Given this context, let us now discuss its evaluation.

CRM Stock Valuation – 23x Non-GAAP Forward EPS

Salesforce revised its non-GAAP EPS guidance for fiscal 2025 from $9.76 to $9.94, an increase of 2% since the beginning of this fiscal year.

Thus, it is natural to assume that at some point in the next 12 months, Salesforce EPS will deliver $10 from non-GAAP EPS, leaving the stock price at 23x forward of non-GAAP EPS. , which is a number that is far from expanding.

However, the fact that Salesforce has focused strongly over the past 12 months on improving its profit margins has come at a cost, given that its growth rates have now moderated. Here lies the problem.

Investors realize that without supportive, stable, and strong revenue growth, Salesforce’s EPS prospects can’t shine just yet.

On the other hand, Salesforce notes that both its GAAP and non-GAAP EPS estimates for fiscal 2025 do not include any potential share repurchases. Therefore, it’s very likely that Salesforce’s non-GAAP EPS will reach $10 per share sooner than investors are currently expecting.

Overall, this is not a thesis-breaking quarter.

Bottom line

As an investor who has been bullish on Salesforce for some time, I believe this sell-off is an overreaction.

Despite concerns about slowing growth rates and the inability to revise FY2025 revenue growth upwards, the company’s intrinsic value remains strong. Salesforce’s strategic focus on AI, its leadership in the CRM market, and its strong financial performance, including significant cash flow and earnings generation, reinforce my confidence.

Paying 23 times forward non-GAAP EPS represents a fair entry point for investors. While the weak RPO number and moderate growth rates pose near-term challenges, Salesforce is good for future growth. I stand by my assertion: Don’t give up on CRM.