Samsara Q1: Institutional Mix and International Strength Confirm Outperforming Quarter (IOT)

to imagine

Investment thesis

samsara (New York Stock Exchange: Internet of Things) announced its quarterly earnings and revenue for the first quarter of fiscal year 25. The manufacturer of tools and cloud solutions for connected operations posted strong profits in the first quarter, which led to a slight increase in its profits Guidance ahead of its previous forecast for sales growth, making Samsara one of the few companies to take a hit this earnings season.

International growth and strong momentum in Samsara’s net new annual contract value were among the bright spots in the company’s earnings report, according to my review of its numbers.

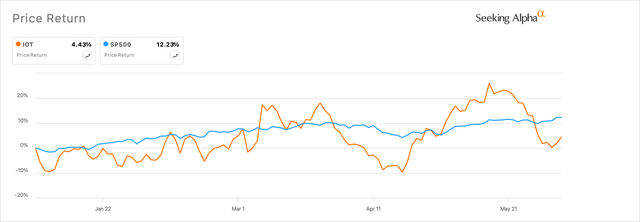

Ignoring any market movements following the earnings report, Samsara has lagged behind the broader performance of the markets, now up just 2% so far in 2024, while the S&P 500 is up nearly 12% for the year, as seen below in Exhibit A.

Exhibit A: Samsara’s performance this year It was also lackluster in comparison to broader markets. (Sa)

After analyzing Samsara’s Q1 2024 results, I’m optimistic about the company’s long-term prospects, but with the numbers I have, I’d lower my target and classify this as a ‘hold’.

Earnings strength led by international and net new additions

In March of this year, I published a research note on Samsara where I said:

“I believe Samsara’s focus on addressing a highly fragmented target market that is still in the early stages of digitization is paying dividends for the company as customers increasingly find more traction in Samsara’s connected vision.”

I believe the appeal of the Samsara product line is increasingly being seen by customers on a global scale, as evidenced by their Q1 report.

In Q1 2025, the San Francisco, California-headquartered company reported revenue of $280.7 million, up 37% year over year, beating consensus estimates by $8.3 million, or ~3.1%, as shown below. In Figure (b). The company’s first quarter revenue numbers were comfortably above the high end of management’s previous first quarter revenue target range of $271 million to $273 million.

Exhibit B: Samsara increased its revenue sequentially and year over year to approximately $281 million, beating expectations. (Q1 FY25 Earnings Report, Samsara)

The year-over-year and sequential strength demonstrated by the company’s top-of-funnel metrics, revenue and ARR (Annual Recurring Revenue) was encouraging in my opinion. In the first quarter, annualized revenue rose 37% for the year to $1,176 million. Management said in the earnings call that the company also benefited from an expansion in ACV (annual contract values), with the mix of net new customers gradually growing again.

According to management, 59% of GVA during the quarter came from customer expansion, while the remaining 41% of GVA came from net new logo addition, the second highest rate in the company’s operating history. At the same time, “18% of net new ACV came from non-U.S. geographies driven by strength in Mexico and Europe, which contributed the highest quarterly mix of net new ACV ever in Q1.” A new record according to the administration.

This strength was also evident in the company’s customer metrics, which pointed to some incremental gains in its key target segment, $100K+ ARR customers, which grew 43% year over year to nearly 2,000 customers in the first quarter. I notice that the pace at which Samsara is adding logos to its $100K+ ARR clients is slowing down if you compare the pace to the same quarter last year, as the company’s $100K+ ARR client pool grew by 53% last year.

This still appears to be very strong, but the pace of growth seems to have returned to normal. Additionally, the company’s $100K+ ARR client pool now represents 53% of the company’s ARR, which is encouraging as it attempts to further penetrate this market.

Exhibit C: Samsara’s $100K+ ARR client pool grew 43% year over year to 1,964 clients. (Q1 FY25 Earnings Report, Samsara)

Operating leverage indicates moderate signs of improvement

Samsara’s management also delivered impressive earnings in the first quarter, with the company reporting adjusted earnings of 3 cents per share, easily topping the consensus mark of 1 cent per share. The company’s bottom line was supported by a massive 12-point expansion in adjusted operating margin compared to the previous year, with the company reporting an adjusted operating margin of 2%. Adjusted operating income reached $6.2 million in Q1 FY25. The company’s gross margins even expanded 4% to 76% in the first quarter.

Exhibit D: Samara’s adjusted margin profile for 1QFY25 (Source: Q1FY25 Earnings Report, Samsara)

The company is still reporting operating losses if you look at its GAAP numbers; However, those numbers narrowed further with the company reporting a GAAP operating loss of approximately $66 million, down from the approximately $76 million reported last year.

Since the company is focusing on selling to larger clients, as we mentioned earlier, I find it necessary to review the company’s expenses. As shown in Exhibit E below, the company’s SG&A expenses increased approximately 26% in Q1 FY25 to $205 million. This indicates that management spends about 73% of its turnover on acquisitions and expansion. To me, this represents some improvement in acquisition efficiency year over year as I see the company spent 79.4% of its revenue in April of last year.

Figure E: Samara’s expenses over the past year (Company sources)

Furthermore, Samsara’s balance sheet appears well-capitalized with no debt, and cash is up 20% year-to-date to $162.5 million.

Long term optimistic but lower price targets

On the earnings call, management updated guidance for Q2 and for FY25. Management’s expectations for Q2 seemed slightly tempered, in my opinion, if you compare that to what the markets were expecting.

For 2QFY25, management expects the company to earn roughly $0.05 per share, barely breaking even on total revenue of roughly $289 million, at the midpoint of the guidance range. By comparison, markets were expecting the company to expect 1 cent of earnings per share on revenue of $288 million. However, management expects the company to maintain similar performance linearity to the trends observed in FY23. Given that the company’s H2s are typically stronger, I expect the company to accelerate and perhaps even beat its own forecast of $1.205-$1.213 billion, gathered from 1 $186 – $1,196 million issued last quarter.

With operating profits tight and company stocks rising, I will continue to resort to revenue forecasting to arrive at my target price for Samsara. My model will assume a discount rate of 8.8% which factors in according to the calculations here.

The thing that surprised me about the earnings report is the significant increase in stock dilution that management is seeing for this year. My previous forecast was based on a 2-3% dilution rate the company outlined at last year’s investor day, but the company expects its outstanding shares to now reach ~580 million this year alone, implying an 8% dilution rate. Which will affect expected returns.

Exhibit F: Samsara stock shows marginal rise (author)

As shown in Figure F above, I now expect the company’s revenue to grow at approximately 28% CAGR, which is higher than the 26% CAGR I estimated in my previous coverage of Samsara. These growth rates suggest a forward sales multiple of approximately 14x if you compare them to the long-term growth rates of the broader market. This means that there will now only be a 5-6% upside, which does not look attractive despite my optimistic long-term outlook for Samsara.

Risks and other factors to look out for

Samsara’s management has repeatedly stated, time and time again, that the company is not sensitive to the slowdown seen in the larger software spending environment since the company is technically the beneficiary of operations budgets and not IT budgets.

According to management, the company’s products attract a completely different set of end users within the organization. But over the past four weeks, the company has been impacted by a decline in enterprise IT spending, as seen by leading cloud software companies like Salesforce (CRM) and MongoDB (MDB). So far, management insists there has been no slowdown in operations budgets.

I expect the company to add more details to its roadmaps to achieve more profitability in addition to the progress it has shown. Additionally, if management can add more detail about why equity dilution is expected to suddenly increase this year and whether investors should expect similar dilution rates over the longer term, that would help investors make more informed decisions based on the implications of future dilution rates. .

NB: The company is expected to add more color to its long-term operating model at its upcoming FY25 Investor Day on June 27, later this month.

Ready meals

I remain very optimistic about the long-term operational vision of the company and the connected technology space in which Samsara operates. Samsara’s management has been able to show outperformance so far, and the first quarter was another feather in the cap for the management.

But factoring in future growth at the moment, I’d recommend staying neutral on Samsara for now.